Valuation After Recent Multi Year Shareholder Returns")

With no single headline event driving attention to Marvell Technology (MRVL) today, investors may instead focus on how the stock has traded recently and how that lines up with the company’s current fundamentals.

Over the past week, Marvell’s share price has moved by about 16%, with a smaller gain over the past month and a modest positive return over the past 3 months. Those moves sit against a last close of US$90.44 and a value score of 4. Some investors may use that score as a starting point when comparing Marvell to other semiconductor names.

See our latest analysis for Marvell Technology.

That recent 16% 7 day share price return sits alongside a 1 year total shareholder return of about 30% and a 3 year total shareholder return above 140%, which hints at momentum that has built over a multi year period.

If Marvell’s move has you looking at the wider chip space, this could be a good moment to scan our list of 34 AI infrastructure stocks as potential next ideas to research.

So with Marvell posting solid multi year returns, reporting annual revenue of about US$8.2b and net income of roughly US$2.7b, and trading around US$90, is the stock still undervalued or are markets already pricing in future growth?

Most Popular Narrative: 41.8% Undervalued

According to a widely followed narrative on Simply Wall St, Marvell’s fair value sits at about $155.37 per share versus the recent $90.44 close. This frames a very different picture to the current market price.

Marvell Technology has executed a masterclass in capital allocation. In Q3 Fiscal 2026, they did two things that fundamentally alter the investment thesis: they sold their lower-growth Automotive Ethernet business for $2.5 Billion cash, and announced the acquisition of Celestial AI. This is a clear signal that Marvell is going “All-In” on AI Data Center Infrastructure. With record quarterly revenue of $2.075 Billion (+37% YoY) and guidance accelerating, Marvell is solidifying its position as the critical “plumber” of the AI era, controlling how data moves between Nvidia’s GPUs.

If you want to see what sits behind that valuation, the narrative leans heavily on rapid data center growth, richer margins from AI hardware and a future earnings multiple usually reserved for market leaders. Curious how those moving parts connect into one number and how sensitive the fair value is to just a few key assumptions? The full breakdown lays out the exact growth, margin and valuation inputs behind that $155.37 figure.

Result: Fair Value of $155.37 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on AI data center spending and successful Celestial AI integration; slower orders or execution missteps could quickly erode that undervaluation thesis.

Find out about the key risks to this Marvell Technology narrative.

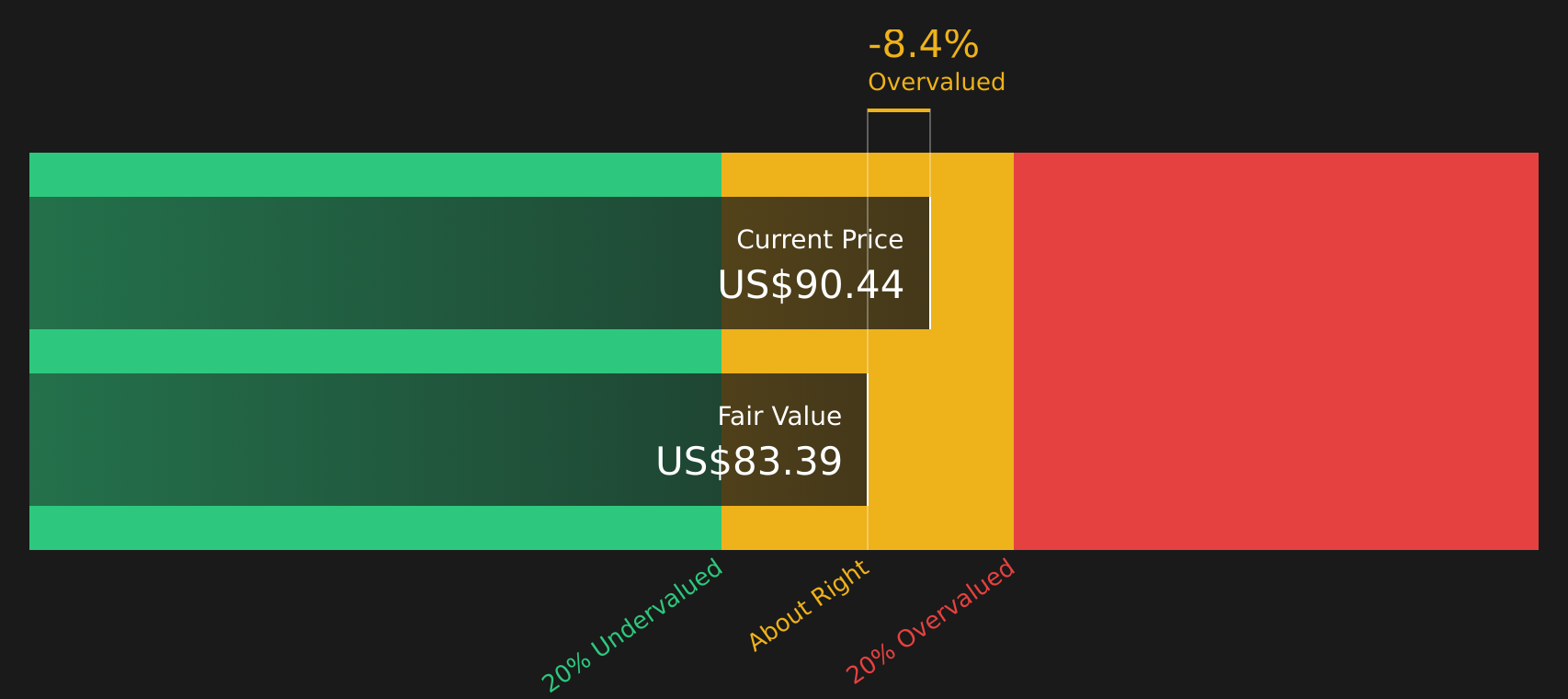

Another View: Our DCF Model Is More Cautious

That 41.8% undervalued fair value of $155.37 rests on a narrative model, but our DCF model paints a different picture. On those cash flow assumptions, Marvell at $90.44 sits above an estimated value of $83.39, which points to the shares looking overvalued instead. Which story appears more robust?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Marvell Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If this mix of bullish and cautious signals feels mixed to you, do not wait on headlines to decide for you. Instead, weigh the 5 key rewards and 1 important warning sign to shape your own view.

Looking for more investment ideas?

Before you move on, use this moment of focus to line up your next ideas with the Simply Wall St screener so you are not reacting after the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com