Valuation As Energy Cost Concerns Meet Solid Recent Results")

Cheesecake Factory (CAKE) has been caught between rising crude oil and gasoline prices, which can pressure restaurant margins and consumer spending, and its recent revenue beat and ongoing restaurant expansion.

That tension is what many investors are reacting to, as they weigh higher input and transportation costs against the company’s report of 4.4% year on year revenue growth to US$961.6 million and record annual revenue supported by 25 new openings.

See our latest analysis for Cheesecake Factory.

Cheesecake Factory’s share price has pulled back over the past week, with a 7 day share price return of 6.71% and a 30 day share price return of 1.87%. However, the 90 day share price return of 14.56% and 1 year total shareholder return of 27.14% suggest momentum has generally been positive as investors balance solid recent results against renewed concerns about higher fuel related costs.

If this energy driven volatility has you rethinking where growth could come from next, it might be worth casting a wider net with our screener of 19 top founder-led companies.

With record annual revenue, 18% net income growth and the share price sitting at a discount to the average analyst target, investors are left with a familiar question: is this a buying opportunity or is future growth already priced in?

Most Popular Narrative: 5% Undervalued

Cheesecake Factory’s most followed valuation narrative pegs fair value at about $60.61, a little above the last close at $57.57, which puts the focus squarely on what has to go right operationally.

Strategic unit expansion including aggressive growth of concepts like Flower Child (with AUVs approaching $5 million and mature unit margins over 20%) and North Italia broadens the total addressable market while leveraging rising demand for premium fast casual and polished casual dining; this diversifies revenue streams, accelerates system sales growth, and improves blended profit margins.

Curious what kind of revenue pace, margin lift, and future P/E all need to line up for that fair value math to work? The full narrative spells out the growth mix, unit economics, and valuation multiple that underpin the $60.61 figure without assuming everything goes perfectly.

Result: Fair Value of $60.61 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there is still the risk that rising labor and operating costs, along with weaker traffic at key concepts, could pressure margins and challenge the positive valuation narrative.

Find out about the key risks to this Cheesecake Factory narrative.

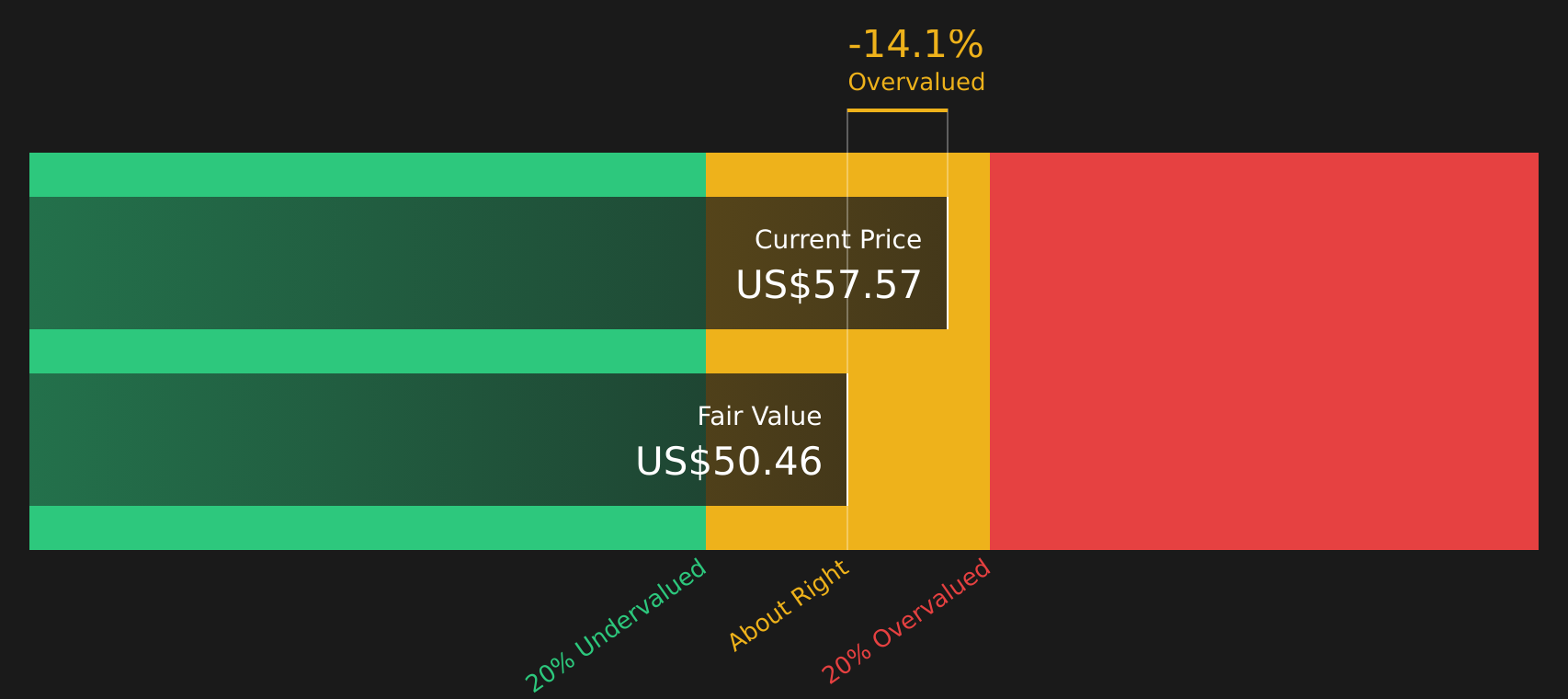

Another View: Cash Flows Point to a Richer Price

While the popular narrative suggests Cheesecake Factory is about 5% undervalued at a fair value of $60.61, our DCF model presents a different view. Based on those cash flow assumptions, fair value comes out closer to $50.46, which would leave today’s $57.57 share price looking overvalued instead. Which story seems more realistic for how cash flows might develop?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cheesecake Factory for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern feels familiar, it is a good moment to look at the numbers yourself and move quickly to frame your own view. You can start with 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you are weighing Cheesecake Factory and still feel uncertain, do not stop here. Broaden your watchlist with a few focused sets of ideas built from our screeners.

- Target income first by reviewing companies we group as 14 dividend fortresses that may appeal if reliable cash returns are near the top of your wish list.

- Hunt for pricing gaps by scanning our collection of 48 high quality undervalued stocks that could suit investors who want quality businesses at what looks like a discount.

- Protect your downside by checking stocks in our 68 resilient stocks with low risk scores that might fit if you care most about steadier fundamentals and smaller swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com