Has Changed Its Investment Story")

- The Walt Disney Company has recently overhauled its leadership, with Josh D’Amaro succeeding Bob Iger as CEO and Dana Walden taking charge of a newly unified Disney Entertainment structure that brings together streaming, film, television, games, and digital operations.

- This consolidation of creative and distribution oversight, alongside fresh leadership across parks, experiences, and communications, could materially influence how Disney coordinates content, monetizes its intellectual property, and allocates capital across its most profitable and fastest-evolving businesses.

- We’ll now examine how Josh D’Amaro’s appointment and the unified Disney Entertainment structure may reshape Disney’s existing investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

Walt Disney Investment Narrative Recap

To own Disney today, you need to believe it can balance its Experiences engine with a now profitable streaming business, while keeping its franchises relevant across formats. The leadership reshuffle around Josh D’Amaro and Dana Walden directly touches both the key near term catalyst of better streaming economics and the major risk that rising content and park investments fail to earn adequate returns. At this stage, the news mainly clarifies accountability rather than changing those fundamentals.

For me, the most relevant development is Dana Walden’s new role leading a unified Disney Entertainment group that now includes streaming, film, television, games and digital operations. This matters for the Disney+ Hulu ESPN bundle and the broader direct to consumer push, because execution on a single, coherent content and distribution plan sits at the heart of both the streaming profitability catalyst and the risk of over spending on content that audiences eventually tire of.

Yet investors should also understand how rising sports rights and park expansion spending could pressure Disney’s margins if…

Read the full narrative on Walt Disney (it’s free!)

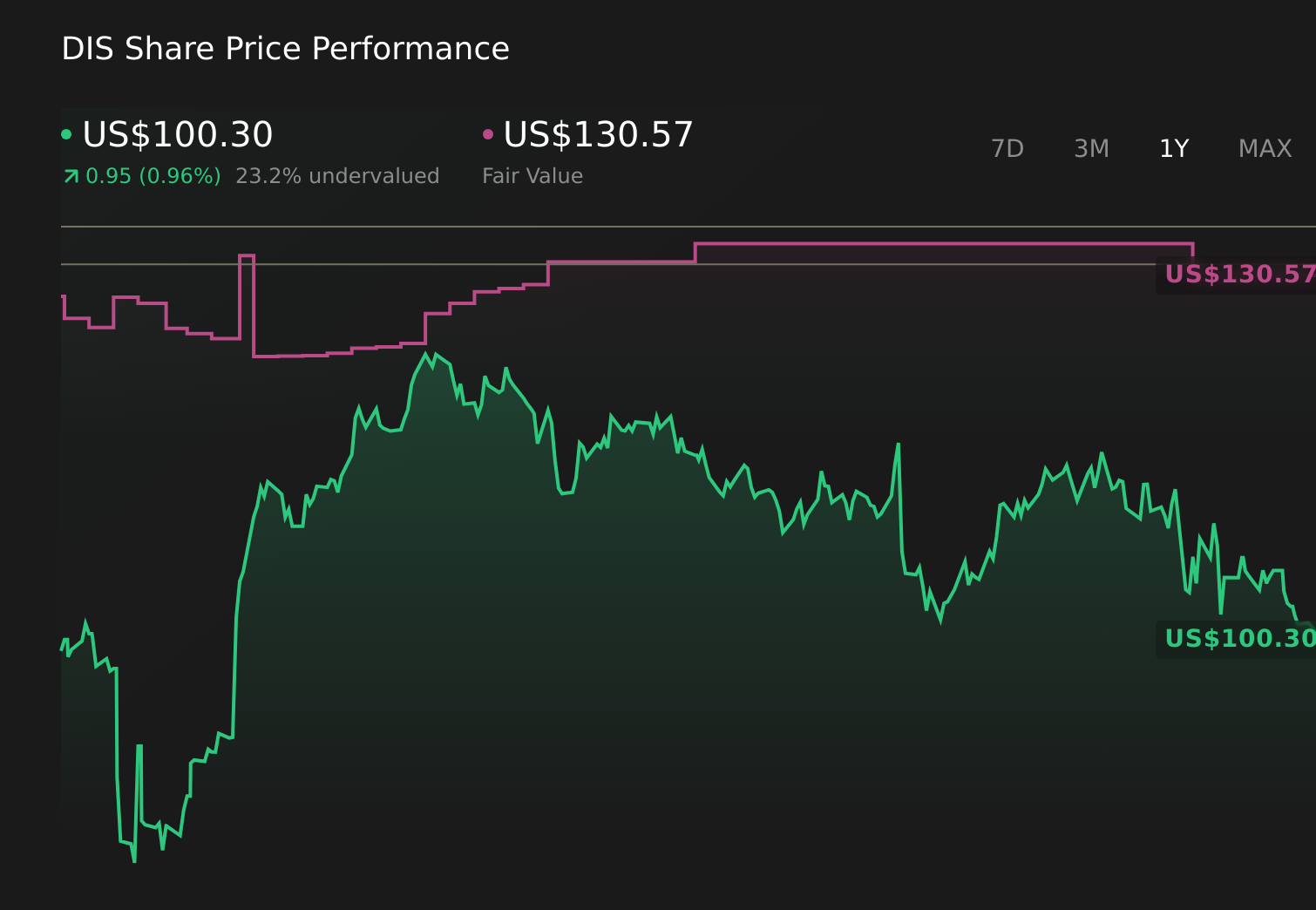

Walt Disney’s narrative projects $106.4 billion revenue and $11.9 billion earnings by 2028. This requires 4.0% yearly revenue growth and about a $0.3 billion earnings increase from $11.6 billion today.

Uncover how Walt Disney’s forecasts yield a $130.30 fair value, a 30% upside to its current price.

Exploring Other Perspectives DIS 1-Year Stock Price Chart

DIS 1-Year Stock Price Chart

Ten Simply Wall St Community valuations for Disney range from about US$99.79 to US$131.56, showing how far apart individual fair value views can be. Against that backdrop, the push to unify Disney’s entertainment and direct to consumer operations under new leadership highlights how differently people may weigh the upside of a stronger bundle against the risk of higher content and capital spending, so it is worth exploring several viewpoints before deciding what you think the company is really worth.

Explore 10 other fair value estimates on Walt Disney – why the stock might be worth as much as 31% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Walt Disney might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com