Although the overall financial markets remain relatively calm at present, Nicolai Tangen, who oversees Norway’s 2.2 trillion US dollar sovereign wealth fund, has been issuing warnings about the potential consequences of the current Middle East situation. Citing economist Hyman Minsky’s theory, he stated that prolonged stability fosters overconfidence and risky behavior, which could eventually lead to panic.

According to Zhitong Finance, although the overall financial market remains relatively calm at present, Nicolai Tangen, who oversees Norway’s $2.2 trillion sovereign wealth fund, has been warning about the potential consequences of the current situation in the Middle East. He cited economist Hyman Minsky’s theory that prolonged stability breeds complacency and risk-taking behavior, which eventually triggers panic.

The head of Norges Bank Investment Management (NBIM) pointed out that there are currently two main bearish scenarios. The first is the return of inflation: a de facto blockade of the Strait of Hormuz would push oil prices above $100 per barrel, exacerbating risks of supply chain disruptions. The second is geopolitical fragmentation—Trump’s tariff policies have already eroded trade ties, and this conflict has further driven a deep wedge between the U.S. and many of its allies, who feel they have been dragged into an unwanted conflict.

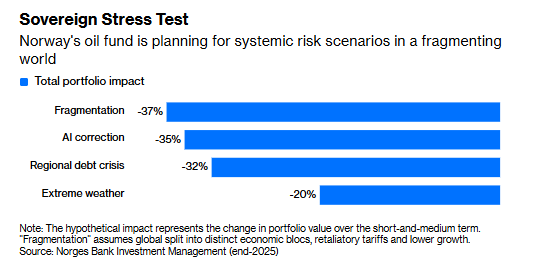

These risks will not only directly impact the Norwegian fund but also ripple through the entire stock market. Stress tests conducted for the end of 2025 show that the disintegration of trade links, slower economic growth, and declining corporate profits could lead to a 49% contraction in the fund’s equity portfolio and a 37% loss in total asset value. Norway may gain short-term benefits from rising oil and gas prices, but broader economic difficulties will severely hit the fund, whose transfers have long accounted for 20% to 25% of Norway’s annual budget.

These risks will not only directly impact the Norwegian fund but also ripple through the entire stock market. Stress tests conducted for the end of 2025 show that the disintegration of trade links, slower economic growth, and declining corporate profits could lead to a 49% contraction in the fund’s equity portfolio and a 37% loss in total asset value. Norway may gain short-term benefits from rising oil and gas prices, but broader economic difficulties will severely hit the fund, whose transfers have long accounted for 20% to 25% of Norway’s annual budget.

The technology sector represents another dangerous area of complacency. While Tangen is “convinced” of the potential of artificial intelligence (AI), believing AI tools can boost corporate productivity by about 20%, he is deeply concerned about overvalued tech stocks and unclear AI profitability prospects. Internal stress tests indicate that a correction in the tech market could wipe out more than half of the fund’s stock portfolio value.

While warning of the economic costs of war, the fund manager refrained from offering opinions on how policymakers should respond. The Norwegian fund is fundamentally an index-tracking investor but is being forced to heighten its geopolitical sensitivity. During a trip to Paris, he did encourage bankers, investors, and officials to strengthen the European single market following advice from former ECB President Mario Draghi: deepen economic integration, unify capital markets, and reduce bureaucratic barriers. “We love Europe… but we must acknowledge that (compared to the U.S.) its growth and innovation are indeed lower.”

Policymakers should heed this message, which echoes the global order restructuring that was underway before Trump’s reckless escalation. Europe, with net energy imports reaching 60%, appears vulnerable. Relevant economic research estimates that the Eurozone’s inflation rate in March could reach 2.6%, lower than the estimated 3.3% in the U.S., but under the worst-case scenario, rising oil prices could deal a blow to growth, potentially pushing France into recession.

This will place greater pressure on central bank officials as they prepare for interest rate decisions. Similarly, it will influence government decision-making—still haunted by memories of the inflation shock following the pandemic in 2022. Belgium’s leader even proposed repairing relations with Russia to lower energy costs, a move that drew criticism but reflects the harsh political reality of protecting voter interests.

There is hope that reason will prevail—especially when European leaders begin saying “no” to Trump and find their own stance. If the revised management guidelines for Norway’s sovereign wealth fund ultimately drive increased investment in Europe (as part of the de-dollarization process that gained momentum prior to the U.S.-led bombing of Iran), it would be beneficial.

The fund faced criticism last year in the U.S. for what was seen as “moral posturing”—divesting from Caterpillar (CAT.US) shares over concerns that bulldozers were being used in Gaza. Some Norwegian politicians have called for reducing exposure to the unpredictable U.S. Billionaire Musk also attacked Tangen after the fund opposed the re-approval of his Tesla compensation plan.

Ultimately, this is about preparing for the worst rather than maintaining the optimistic expectations harbored by many investors today. If geopolitical complacency and tech-sector overconfidence simultaneously collapse, investors will no longer be able to claim they were unprepared.