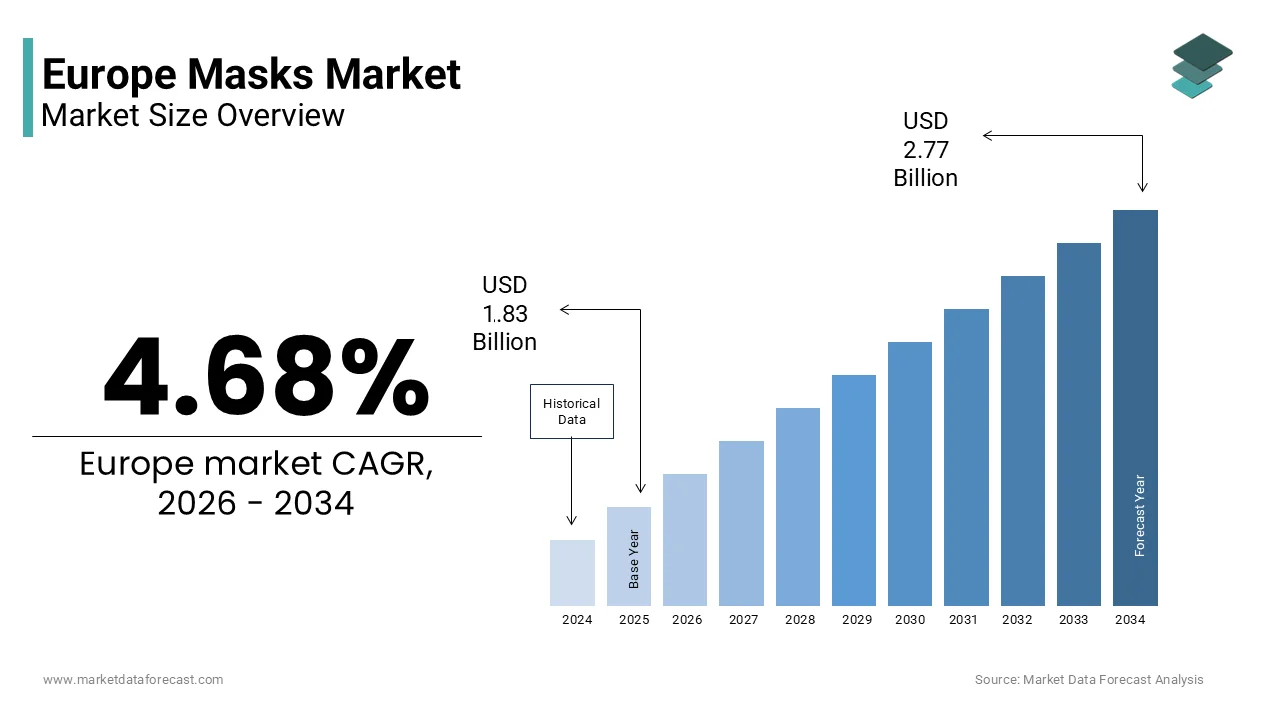

The Europe masks market was valued at USD 1.83 billion in 2025, is estimated to reach USD 1.92 billion in 2026, and is projected to reach USD 2.77 billion by 2034, growing at a CAGR of 4.68% during the forecast period. Market growth is driven by increasing awareness of personal health and safety, rising demand for protective equipment across healthcare and industrial sectors, and recurring usage during seasonal illnesses and pollution exposure. The expansion of workplace safety regulations and healthcare infrastructure is further supporting market demand. In addition, growing consumer preference for convenient and disposable protective products is contributing to steady market growth across Europe.

Key Market Trends

- Rising awareness of health, hygiene, and respiratory protection is driving demand for masks.

- Increasing adoption of disposable masks is supporting convenience and hygiene needs.

- Growth in healthcare and industrial safety standards is boosting market expansion.

- Expansion of retail and pharmacy networks is improving product accessibility.

- Technological advancements in filtration efficiency and comfort are enhancing product performance.

Segmental Insights

- Based on distribution channel, the offline segment was the largest and held 60.8% of the Europe masks market share in 2025. This dominance is attributed to strong presence of pharmacies, supermarkets, and medical supply stores offering easy access to consumers.

- Based on usage, the disposable segment accounted for 66.5% of the Europe masks market share in 2025. The segment’s growth is driven by convenience, hygiene, and widespread use in healthcare and daily protection.

- Based on end use, the women’s segment held 51.8% of the Europe masks market share in 2025, supported by higher adoption of personal care and protective products among female consumers.

Regional Insights

- The Europe masks market is experiencing steady growth across key countries, supported by increasing health awareness and safety regulations.

- Germany was the largest contributor, accounting for 23.2% of the Europe masks market share in 2025, driven by strong healthcare infrastructure, high safety standards, and widespread use of protective equipment.

Competitive Landscape

The Europe masks market is highly competitive, with key players focusing on product innovation, quality standards, and expansion of distribution networks to strengthen their market position. Companies are investing in advanced filtration technologies, ergonomic designs, and sustainable materials to meet evolving consumer and industrial requirements. Prominent players in the Europe masks market include 3M Company, Honeywell International Inc, DuPont de Nemours Inc, Kimberly Clark Worldwide Inc, Uvex Group, Ansell Limited, Delta Plus Group, Drägerwerk AG, Avon Protection plc, Moldex Metric Inc, Alpha Pro Tech Ltd, and Cardinal Health Inc.

Europe Masks Market Size

The Europe masks market size was valued at USD 1.83 billion in 2025 and is projected to reach USD 2.77 billion by 2034 from USD 1.92 billion in 2026, growing at a CAGR of 4.68%.

Masks are a diverse array of respiratory protective equipment ranging from disposable surgical masks and filtering facepiece respirators to reusable cloth barriers and specialized industrial gear. This sector has undergone a paradigm shift from being a niche medical supply to a fundamental component of public health infrastructure and personal safety protocols across the continent. The definition now extends beyond simple filtration to include comfort, sustainability, and regulatory compliance with stringent European standards such as EN 14683 for medical masks and EN 149 for FFP respirators. According to the European Commission, the European Union maintained notified bodies responsible for certifying personal protective equipment, ensuring that every mask entering the market meets rigorous safety benchmarks. The market is characterized by a dual demand structure driven by healthcare institutions requiring clinical-grade protection and the general public seeking reliable barriers against airborne pathogens and pollution. As per the European Centre for Disease Prevention and Control, the region experienced elevated respiratory virus surveillance, prompting health authorities to recommend mask usage in high-risk settings during peak seasons. This normalization of mask-wearing has embedded the product into daily life, transforming it from an emergency item to a staple accessory. Furthermore, the industry is increasingly focused on environmental impact, with innovations targeting biodegradability and recyclability to address the waste generated by single-use products.

MARKET DRIVERS Stringent Occupational Safety Regulations and Industrial Mandates

The rigorous enforcement of occupational safety legislation across European industries is propelling the expansion of the European masks market. The European Union’s Framework Directive on Safety and Health at Work mandates that employers provide adequate personal protective equipment, including respirators, to workers exposed to hazardous dusts, fumes, and biological agents. According to the European Agency for Safety and Health at Work, a significant portion of the European workforce is exposed to carcinogenic substances, necessitating the use of FFP2 or FFP3 rated masks to ensure compliance with exposure limits. This legal obligation creates a non-discretionary demand stream that remains stable regardless of economic fluctuations or public health crises. Industries such as construction rely heavily on these mandates to mitigate liability and protect worker health. As per national labor inspectorates, fines for non-compliance with PPE regulations have increased, driving companies to procure higher volumes of certified masks. Furthermore, the expansion of safety protocols into emerging sectors like battery manufacturing and renewable energy installation has broadened the user base. The continuous updating of occupational exposure limits for substances like silica and wood dust ensures that the specification for mask filtration efficiency remains high, compelling industries to regularly upgrade their inventory. This regulatory backbone provides a predictable and substantial revenue stream for manufacturers specializing in industrial-grade respiratory protection.

Heightened Public Health Awareness and Respiratory Hygiene Culture

A profound and lasting shift in public behavior regarding respiratory hygiene has emerged as a significant driver for the Europe masks market, with citizens voluntarily adopting mask-wearing as a standard preventive measure. The collective experience of recent global health crises has ingrained a culture of responsibility where individuals wear masks when symptomatic or in crowded indoor spaces to protect others. According to the European Consumer Organisation, many respondents in Western Europe stated they would continue to wear masks in healthcare settings or public transport during flu season, indicating a permanent change in social norms. This behavioral adaptation has created a robust consumer market for retail masks, distinct from institutional procurement. As per the World Health Organization Regional Office for Europe, the prevalence of influenza and other respiratory viruses remains high, reinforcing the perceived utility of masks. Data from pharmacy sales records shows that over-the-counter mask purchases have increased during winter months compared to pre-2020 levels, reflecting this new baseline demand. Furthermore, the destigmatization of mask-wearing has encouraged broader acceptance across different age groups and social demographics. The integration of mask usage into daily routines for commuting and shopping ensures a steady flow of retail sales, diversifying the market beyond reliance on emergency stockpiling.

MARKET RESTRAINTS Environmental Concerns Regarding Single-Use Waste

The massive accumulation of single-use mask waste poses a significant environmental restraint on the Europe masks market, which is triggering regulatory backlash and consumer hesitation. During peak usage periods, billions of disposable masks enter the waste stream, many of which are made from polypropylene, a plastic that takes hundreds of years to degrade. According to the European Environment Agency, improper disposal of personal protective equipment has led to a noticeable increase in marine litter, with masks ranking among the top items found on European beaches. This environmental burden has prompted strict waste management regulations and bans on certain single-use plastics in various member states, complicating the distribution and disposal of traditional masks. As per municipal waste management authorities, the cost of collecting and processing mask waste has surged in major cities, straining public budgets. The visual pollution and ecological threat associated with discarded masks have also fueled negative public sentiment, leading some consumers to avoid purchasing disposable options despite their convenience. Furthermore, the lack of specialized recycling infrastructure for contaminated masks means that most end up in landfills or incinerators, contradicting the EU’s circular economy goals. According to waste tracking organizations, only a small fraction of used masks are currently recycled, highlighting a critical inefficiency. This environmental dilemma forces manufacturers to reconsider material choices and design strategies, potentially increasing production costs and limiting the availability of low-cost disposable options.

Supply Chain Volatility and Raw Material Fluctuations

The Europe masks market faces significant constraints due to its heavy dependence on imported polymer resins, particularly polypropylene, which is the primary raw material for melt-blown fabric used in filtration layers. A substantial portion of these raw materials is sourced from outside the EU, making the market vulnerable to global supply chain disruptions, geopolitical tensions, and freight cost volatility. According to the European Chemical Industry Council, the price of polypropylene fluctuated due to energy crises and feedstock shortages, directly impacting the production costs of masks. This volatility makes it difficult for manufacturers to maintain stable pricing, leading to margin compression or reduced competitiveness against lower-cost imports. The limited domestic capacity for producing high-grade melt-blown fabric exacerbates this dependency, creating bottlenecks during periods of surge demand. As per logistics providers, shipping times for raw materials from Asia to Europe have varied unpredictably, disrupting just-in-time manufacturing schedules. Furthermore, the concentration of suppliers in specific regions increases the risk of supply shocks, as seen during previous global crises. According to trade associations, many European mask manufacturers reported raw material shortages as a major operational challenge in the past year. This structural vulnerability restrains the market’s ability to scale rapidly and maintain consistent supply levels, forcing companies to hold larger inventories and tie up capital.

MARKET OPPORTUNITIES Innovation in Biodegradable and Sustainable Materials

The development of plant-based and biodegradable filtration media offers a promising opportunity for the Europe masks market to align with stringent environmental goals while maintaining high performance. Innovations using polylactic acid derived from corn starch, cellulose nanofibers, and other bio-polymers offer viable alternatives to petroleum-based polypropylene, addressing the waste crisis. According to research institutes focused on green chemistry, recent advancements have enabled bio-based filters to achieve filtration efficiencies comparable to traditional FFP2 standards, opening doors for certification and commercialization. This technological breakthrough allows manufacturers to tap into the growing segment of eco-conscious consumers and corporate buyers committed to sustainability targets. As per pilot projects in Germany and France, biodegradable masks have shown potential to decompose in industrial composting facilities, contrasting with conventional masks. The European Union’s funding programs for green innovation provide financial incentives for companies developing these materials, lowering the barrier to entry. According to market analysis firms, the demand for sustainable PPE is expected to grow significantly as regulations tighten. By pioneering these materials, companies can differentiate their brands, command premium prices, and secure long-term contracts with environmentally mandated public sector entities. This shift not only mitigates environmental risks but also future-proofs the business model against impending plastic bans.

Integration of Smart Technologies and Functional Features

The integration of smart technologies, such as embedded sensors and IoT connectivity, offers a groundbreaking opportunity to elevate masks from passive barriers to active health monitoring devices. Innovations including breath analyzers, temperature sensors, and humidity detectors can provide real-time data on the wearer’s respiratory health and mask fit, appealing to both industrial and medical sectors. According to technology trend reports, the global market for smart wearable health devices is expanding rapidly, and masks represent a logical extension of this trend. Pilot programs in European hospitals have demonstrated the efficacy of smart masks in detecting early signs of respiratory distress or fatigue in healthcare workers, enabling timely interventions. As per tech incubators, prototypes capable of detecting specific viral particles or air quality levels are nearing commercial viability. The industrial sector stands to benefit significantly, with smart masks alerting workers to dangerous gas leaks or filter saturation instantly. According to occupational safety studies, real-time monitoring has the potential to reduce workplace accidents related to respiratory hazards. By incorporating these features, manufacturers can unlock high-value market segments willing to pay a premium for enhanced safety and data insights. This technological leap transforms the mask into a critical node in the broader digital health and safety ecosystem.

MARKET CHALLENGES Proliferation of Counterfeit and Non-Compliant Products

The pervasive presence of counterfeit and non-compliant masks in the European market is a significant challenge to the regional market growth, which is also undermining public safety and eroding trust in legitimate brands. Substandard products often fail to meet the required filtration efficiency and breathability standards, putting users at risk of infection or respiratory harm. According to the European Anti-Fraud Office, seizures of fake personal protective equipment at EU borders have increased, highlighting the scale of the illicit trade. These counterfeit items frequently bear forged CE markings, deceiving consumers and procurement officers into believing they are purchasing certified goods. The influx of cheap, non-compliant masks distorts market prices, forcing reputable manufacturers to compete on cost rather than quality, which can compromise their margins and sustainability efforts. As per consumer protection agencies, thousands of complaints regarding ineffective masks are filed annually, damaging the reputation of the entire industry. The complexity of global supply chains makes it difficult to trace the origin of these fakes, allowing them to penetrate deep into the distribution network. According to industry watchdogs, a notable portion of masks sold through unofficial online channels may be non-compliant. Combating this challenge requires constant vigilance, advanced authentication technologies, and coordinated enforcement actions, diverting resources from innovation and growth.

Balancing Comfort with High Filtration Efficiency

Achieving an optimal balance between high filtration efficiency and user comfort remains a persistent technical challenge for the regional market expansion, which is directly impacting compliance and effectiveness. Masks with superior filtration often exhibit higher breathing resistance, leading to discomfort, heat buildup, and moisture accumulation, which discourages prolonged use. According to ergonomic studies conducted by European occupational health institutes, many workers report discomfort as the primary reason for removing their masks prematurely in hazardous environments. This non-compliance negates the protective benefits of the equipment, rendering high-performance masks ineffective in practice. The physiological strain is particularly pronounced for vulnerable groups such as the elderly or those with pre-existing respiratory conditions, limiting the universality of certain mask types. As per user feedback surveys, breathability is a top priority for consumers, often outweighing filtration ratings in purchasing decisions. Manufacturers face the difficult task of engineering materials that capture microscopic particles without impeding airflow, a trade-off that requires advanced and costly material science solutions. According to clinical trials, discomfort-related non-compliance has been shown to reduce overall protection efficacy. Overcoming this challenge requires continuous innovation in fiber geometry and mask design, which demands significant R&D investment and time.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

4.68%

Segments Covered

By Type, Distribution Channel, Usage, End Use, and Region

Various Analyses Covered

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

3M Company, Honeywell International Inc., DuPont de Nemours Inc., Kimberly Clark Worldwide Inc., Uvex Group, Ansell Limited, Delta Plus Group, Drägerwerk AG, Avon Protection plc, Moldex Metric Inc., Alpha Pro Tech Ltd., and Cardinal Health Inc.

SEGMENTAL ANALYSIS By Distribution Channel Insights

The offline segment led the market by accounting for 60.8% of the European market share in 2025 due to the immediate need for physical verification of product quality, fit, and certification, which is crucial for medical and safety equipment. The trust consumers place in established brick-and-mortar retailers, particularly pharmacies, where professional advice is available to ensure the selection of appropriate mask types for specific needs is also aiding the dominance of the offline segment in the European masks market. According to the Pharmaceutical Group of the European Union, many Europeans still prefer purchasing health-related products from physical pharmacies where they can consult with pharmacists about efficacy and standards. This preference is especially pronounced among the elderly population, who are the most frequent users of masks and often lack confidence in navigating online health stores. The second critical driver is the impulse purchase behavior associated with essential goods, where masks are bought alongside groceries or other daily necessities during routine shopping trips. As per retail analytics firms, a significant portion of mask purchases in Europe occur as add-on items in supermarkets, driven by visibility and convenience. Furthermore, the ability to physically inspect the packaging for CE marks, expiration dates, and batch numbers provides a layer of security against counterfeit products that online channels struggle to replicate. According to consumer protection agencies, complaints about fake masks are higher for online purchases compared to offline ones, reinforcing the preference for physical stores. The tactile experience of trying on different sizes to ensure a proper seal also remains a decisive factor, solidifying the offline channel’s market leadership.

However, the online segment is estimated to showcase the fastest CAGR of 10.4% over the forecast period owing to the digital transformation of healthcare retail and the changing shopping habits of younger demographics who prioritize convenience and variety. The foremost driver is the proliferation of e-commerce platforms offering a vast array of mask types, brands, and specialized features that are often unavailable in local physical stores. According to Eurostat, online sales of health and personal care products in the EU have grown, with masks being a top contributor due to the ease of bulk purchasing and home delivery. The second major factor is the rise of subscription models and automated replenishment services offered by online retailers, which ensure a continuous supply of masks for households and businesses without the need for repeated manual ordering. As per e-commerce giants, subscription-based purchases of hygiene products have increased, as consumers seek to automate the management of essential supplies. Additionally, the availability of detailed product reviews, comparison tools, and transparent pricing online empowers consumers to make informed decisions based on performance data and user feedback. According to digital marketing studies, many consumers research mask specifications online before buying, and many complete the purchase on the same platform for convenience. The integration of telehealth services with online pharmacies further accelerates this growth, allowing patients to receive prescriptions and order corresponding protective gear in a seamless digital workflow. These factors collectively make the online channel the most dynamic and fast-scaling segment in the market.

By Usage Insights

The disposable segment held the dominating position by holding 66.5% of the regional market share in 2025 due to the unparalleled convenience, hygiene assurance, and regulatory mandates in healthcare settings. The strict infection control protocols enforced in hospitals, clinics, and long-term care facilities across Europe that mandate the use of fresh, sterile masks for every patient interaction is also supporting the dominance of disposable segment in the European masks market. According to the European Centre for Disease Prevention and Control, disposable surgical masks and FFP respirators are the standard of care for preventing nosocomial infections, creating a massive and non-negotiable institutional demand. The second significant driver is the consumer perception of disposables as the safest option due to the elimination of cleaning errors and the guarantee of pristine filtration media for each use. As per hospital procurement data, respiratory protection purchased by public health systems is predominantly disposable, reflecting the entrenched reliance on this format. Furthermore, the low unit cost and widespread availability of disposable masks make them accessible for mass distribution during health crises or flu seasons. According to retail sales volumes, disposable masks account for the majority of units sold in pharmacies, driven by their ease of use and discard. The logistical simplicity of storing and distributing lightweight disposable packs also favors this segment, allowing for rapid scaling of supply chains. Despite environmental concerns, the immediate priority of health safety and regulatory compliance ensures that disposable masks remain the backbone of the European market.

However, the reusable segment is emerging as the fastest-growing category and is anticipated to expand at a CAGR of 11.5% over the forecast period owing to the intensifying environmental awareness and advancements in fabric technology. This robust growth is also likely to be driven by a paradigm shift among consumers and corporations towards sustainability and the reduction of single-use plastic waste. The primary catalyst is the increasing legislative pressure and public sentiment against disposable plastics, prompting individuals and organizations to seek eco-friendly alternatives that can be washed and used multiple times. According to the European Environment Agency, the push for a circular economy has led to rising consumer interest in washable textile masks, with many cities implementing initiatives to promote their use. The second driving factor is the technological innovation in antimicrobial fabrics and nanofiber filters that allow reusable masks to offer protection levels comparable to disposables while maintaining comfort and durability. As per textile research institutes, new copper-infused and silver-ion treated fabrics have demonstrated the ability to retain filtration efficiency after multiple wash cycles, addressing previous efficacy concerns. Furthermore, the cost-effectiveness of reusable masks over the long term appeals to budget-conscious consumers and large institutions looking to reduce operational expenditures. According to corporate sustainability reports, many large European companies have switched to providing reusable masks for employees as part of their green initiatives. The customization potential of cloth masks for branding and fashion also drives adoption in the corporate and retail sectors. These converging factors of environmental responsibility, technological viability, and economic sense position the reusable segment for exceptional growth trajectories.

By End Use Insights

The women’s segment dominated the Europe masks market by holding 51.8% of the European market share in 2025. The dominance of women’s segment in the European market is driven by the higher propensity of female consumers to adopt protective measures for themselves and their families, alongside a greater engagement with health and wellness trends. The role women often play as primary caregivers in European households, which is leading them to make the majority of purchasing decisions regarding health supplies including masks for children and elderly relatives is also driving the dominance of the women’s segment in the European market. According to the European Institute for Gender Equality, women spend more time on unpaid care work than men, which directly correlates with their increased procurement of hygiene products. This demographic is also more likely to adhere to public health guidelines and wear masks in social settings, creating consistent retail demand. The second critical driver is the fashion integration of masks, where women have embraced masks as accessories that complement their outfits, spurring demand for varied designs, colors, and patterns. As per fashion retail analysts, designer and patterned mask sales are largely attributed to female consumers who view these items as part of their daily attire rather than just medical equipment. Furthermore, the beauty industry has influenced this segment by launching skincare-friendly masks that prevent makeup smudging and reduce skin irritation, addressing specific concerns prevalent among female users. According to cosmetic dermatology surveys, many women consider skin breathability and material softness as key factors when selecting masks, prompting manufacturers to develop specialized products for this audience. These behavioural and aesthetic factors combine to sustain the dominance of the women’s segment in the market.

On the other side, the men’s segment is projected to be the fastest-growing end-user category and is estimated to witness a CAGR of 7.4% over the forecast period owing to the shifting societal norms regarding male grooming and health consciousness, as well as increasing participation in workforce sectors that mandate respiratory protection. The rising awareness among men about personal health and preventive care, which is moving away from traditional stoicism towards proactive health management is also propelling the expansion of the men’s segment in the European market. According to the European Men’s Health Forum, there has been an increase in men seeking health information and purchasing over-the-counter health products, including high-quality respirators for urban commuting and exercise. The second significant driving factor is the strong representation of men in industrial, construction, and logistics sectors across Europe, where strict occupational safety regulations require the use of certified FFP2 and FFP3 masks. As per the European Agency for Safety and Health at Work, men constitute the majority of the workforce in high-risk industries such as construction and manufacturing, driving a steady and growing demand for industrial-grade masks. Additionally, the trend of “maskne” or acne caused by mask-wearing has led to increased innovation in men-specific skincare masks, with brands launching oil-control and anti-bacterial variants tailored to male skin types. According to dermatological studies, men are more likely to suffer from severe mask-related acne due to shaving and skin texture, creating a niche but rapidly expanding market for specialized solutions. This convergence of occupational necessity and evolving personal care habits positions the men’s segment for robust expansion.

REGIONAL ANALYSIS Germany Masks Market Analysis

Germany was the largest market for masks in Europe and accounted for 23.2% of the regional market share in 2025. The leading position of Germany in the European market is majorly driven by its robust industrial base, stringent occupational safety culture, a high level of compliance with regulatory standards and a strong domestic manufacturing sector that produces high-quality respiratory protection. A key driving factor is the country’s extensive manufacturing and engineering industries, which employ millions of workers requiring certified FFP masks under strict workplace safety laws. According to the German Federal Institute for Occupational Safety and Health, many workers in sectors like automotive, chemical, and construction are mandated to use respiratory protection daily, creating a consistent and high-volume demand. The second critical driver is the German population’s high health consciousness and adherence to scientific guidelines, leading to widespread voluntary mask usage during respiratory virus seasons. As per the Robert Koch Institute, Germany maintains one of the highest per capita consumption rates of medical masks in the EU, supported by a well-funded public health system that stockpiles essentials. Furthermore, the presence of leading global mask manufacturers within Germany fosters innovation and ensures a steady supply of advanced products. The combination of industrial necessity, regulatory rigor, and a proactive health culture cements Germany’s position as the dominant force in the European masks landscape.

France Masks Market Analysis

France also occupied for a significant share of the European masks market in 2025 due to its centralized healthcare system and strong government intervention in public health matters. The French market is defined by the state’s active role in procuring and distributing masks, particularly for the public sector and vulnerable populations. The comprehensive national health strategy that mandates mask usage in healthcare settings and encourages it in public spaces during epidemics, backed by substantial government funding is also driving the French market expansion. According to the French Ministry of Health, the state distributes masks annually to schools, hospitals, and nursing homes, creating a massive institutional market. The second significant driver is the vibrant fashion and luxury sector in France, which has elevated the mask to a style accessory, driving demand for designer and aesthetically pleasing options among the general public. As per the French Fashion Federation, there is a unique synergy between health requirements and fashion trends, with Parisian brands launching high-end mask collections that appeal to both locals and tourists. Additionally, the dense urban population in cities like Paris and Lyon increases the perceived risk of airborne transmission, prompting higher individual adoption rates. According to urban health studies, mask usage in French metropolitan areas is higher than in rural regions, reflecting the impact of population density on consumption. This blend of state support, cultural flair, and urban dynamics ensures France remains a pivotal market.

Italy Masks Market Analysis

Italy is anticipated to be a promising regional segment for masks in Europe during the forecast period owing to its aging demographic profile and the severe impact of past respiratory pandemics which have ingrained a culture of caution. The Italian market is distinct due to the high sensitivity of the population to respiratory health risks, leading to sustained demand even in inter-pandemic periods. The primary driving factor is the country’s status as having one of the oldest populations in Europe, with a significant portion of citizens aged 65 or older, a group that is highly vigilant about protective measures. According to the Italian National Institute of Statistics, households with elderly members purchase more masks than the national average, driven by the need to protect vulnerable family members. The second critical driver is the strong textile and manufacturing heritage of Italy, which enables local producers to quickly adapt and produce high-quality, fashionable, and specialized masks that cater to diverse needs. As per the Italian Textile Industry Association, Italian manufacturers have pioneered the integration of antiviral fabrics and stylish designs, capturing both domestic and export markets. Furthermore, the tourism industry, which brings millions of visitors to historic cities, necessitates robust mask availability in hospitality and transport sectors. According to the Ministry of Tourism, mask provisions are a standard requirement for hotels and tour operators, adding to the overall consumption volume. This convergence of demographic necessity, industrial capability, and tourism demands keeps Italy as a key player.

United Kingdom Masks Market Analysis

The United Kingdom is predicted to showcase a healthy CAGR in the European masks market over the forecast period due to a mature healthcare infrastructure and a strong emphasis on workplace safety regulations post-Brexit. The UK market is defined by a balanced mix of public sector procurement through the NHS and a dynamic private retail sector driven by consumer choice. A major driving factor is the rigorous enforcement of health and safety executive regulations across various industries, compelling employers to provide adequate respiratory protection to workers. According to the UK Health and Safety Executive, inspections and penalties for non-compliance have increased, driving up corporate spending on certified masks. The second significant driver is the high level of public awareness and the “better safe than sorry” attitude prevalent among British consumers, leading to consistent household stockpiling of masks. As per retail sales reports, UK households maintain an average reserve of masks per person, higher than the European average, reflecting a precautionary mindset. Additionally, the growth of the gig economy and delivery services has created a new segment of workers who rely on masks for daily protection, further boosting demand. According to labor market analyses, the courier and delivery sector has grown significantly, directly correlating with increased mask usage. This combination of regulatory pressure, consumer prudence, and evolving work patterns sustains the UK’s significant market position.

Spain Masks Market Analysis

Spain is expected to exhibit a notable CAGR in the European masks market over the forecast period due to its large tourism industry, dense urban centers, and a strong cultural emphasis on social interaction which necessitates protective measures. The Spanish market is influenced by the seasonal influx of millions of tourists, which requires the hospitality and transport sectors to maintain high levels of mask availability and usage. The primary driving factor is the vital role of the tourism and service sectors in the Spanish economy, where staffs in hotels, restaurants, and airports are required to wear masks to ensure guest safety and comply with health protocols. According to the Spanish Confederation of Hotels and Tourist Accommodations, the sector employs millions of people, a significant portion of who are regular mask users, creating a steady baseline demand. The second critical driver is the high population density in major cities like Madrid and Barcelona, which correlates with higher rates of respiratory virus transmission and consequently higher mask adoption. As per the Spanish Ministry of Health, urban areas account for the majority of mask sales, driven by crowded public transport and social venues. Furthermore, the warm climate of Spain has spurred innovation in breathable, lightweight masks suitable for summer use, expanding the usability of masks year-round. According to product development firms, sales of cooling and moisture-wicking masks have increased in Southern Europe. This unique blend of tourism dependency, urban density, and climatic adaptation ensures Spain remains a vital component of the European masks market.

COMPETITIVE LANDSCAPE

The competition in the Europe masks market is characterized by intense rivalry between established multinational corporations and agile local manufacturers vying for dominance through innovation and regulatory compliance. Major players leverage their extensive distribution networks and strong brand reputations to secure large government and institutional contracts while smaller firms focus on niche segments such as eco-friendly or fashion oriented masks. Competitive pressure is heightened by the strict enforcement of European safety standards which requires continuous investment in testing and certification processes to maintain market access. Companies are increasingly differentiating themselves through technological advancements like smart sensors and antimicrobial coatings that offer added value beyond basic filtration. The push towards sustainability has also become a critical battleground where firms compete to develop biodegradable materials and circular recycling programs. This dynamic environment forces participants to balance cost efficiency with high quality standards while adapting to shifting public health guidelines and consumer preferences to capture market share.

KEY MARKET PLAYERS

Some of the notable key players in the Europe masks market are

- 3M Company

- Honeywell International Inc.

- DuPont de Nemours Inc.

- Kimberly Clark Worldwide Inc.

- Uvex Group

- Ansell Limited

- Delta Plus Group

- Drägerwerk AG

- Avon Protection plc

- Moldex Metric Inc.

- Alpha Pro Tech Ltd.

- Cardinal Health Inc.

Top Players in the Market

- Moldex-Metric Inc stands as a preeminent manufacturer of respiratory protection with a significant footprint across the European industrial and medical sectors. The company contributes globally by setting high standards for filter efficiency and user comfort through its proprietary foam and filter technologies. Recently Moldex has strengthened its market position by expanding its production facilities in Germany to increase local supply chain resilience and reduce dependency on imports. They have also launched new lines of reusable respirators equipped with exhalation valves to address sustainability concerns while maintaining safety. These strategic initiatives demonstrate their commitment to innovation and reliability ensuring they remain a preferred partner for healthcare providers and industrial safety managers seeking premium quality protective equipment throughout the continent.

- Drägerwerk AG & Co KGaA is a leading German engineering firm renowned for its advanced safety and medical technology solutions including high performance masks and respirators. Their global contribution involves integrating cutting edge sensor technology and digital monitoring into personal protective equipment to enhance worker safety in hazardous environments. To fortify their standing in Europe Dräger has recently partnered with major hospital networks to supply integrated respiratory care systems that combine masks with ventilation support. They have also invested heavily in research and development to create lighter and more breathable materials that improve compliance among users during extended wear periods. These actions highlight their dedication to merging traditional manufacturing excellence with modern digital health solutions to meet the evolving needs of the European market.

- Uvex Safety Group operates as a key player in the European personal protective equipment landscape offering a comprehensive range of disposable and reusable masks for various industries. The company plays a vital role globally by emphasizing ergonomic design and sustainable production methods that align with strict European environmental regulations. Recent efforts to strengthen their market presence include the acquisition of specialized filter material suppliers to secure raw material access and control quality from source to finish. They have also introduced a circular economy program allowing customers to return used masks for recycling thereby reducing waste and appealing to eco conscious buyers. These proactive measures underscore their focus on sustainability and supply chain security positioning them as a forward thinking leader in the competitive European safety gear sector.

Top Strategies Used by Key Market Participants

Key players in the Europe masks market primarily employ strategies focused on vertical integration to control raw material sourcing and ensure consistent product quality. Companies are heavily investing in local manufacturing facilities to reduce reliance on global supply chains and mitigate logistical disruptions. Another major strategy involves the development of sustainable and biodegradable mask options to comply with stringent environmental regulations and appeal to eco conscious consumers. Brands are also leveraging digital platforms to enhance direct to customer sales and provide educational resources on proper mask usage and safety standards. Additionally, participants are forming strategic partnerships with healthcare institutions and industrial firms to secure long term supply contracts and foster brand loyalty. These approaches collectively aim to build resilience improve sustainability and maintain competitive advantage in a regulated environment.

MARKET SEGMENTATION

This research report on the European masks market has been segmented and sub-segmented based on categories.

By Type

- Surgical mask

- N95 respirators

- Dust mask

By Distribution Channel

By Usage

By End Use

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe