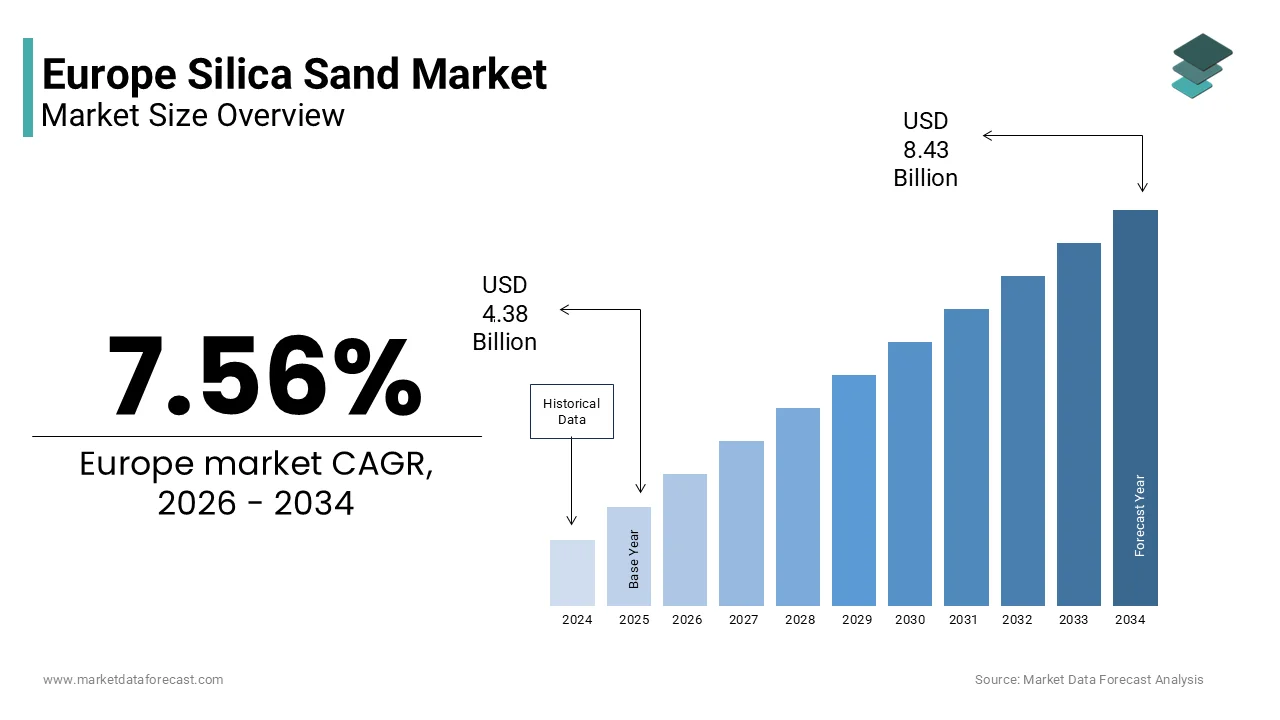

The Europe silica sand market was valued at USD 4.38 billion in 2025, is estimated to reach USD 4.71 billion in 2026, and is projected to reach USD 8.43 billion by 2034, growing at a CAGR of 7.56% during the forecast period. Market growth is driven by increasing demand from glass manufacturing, construction, and industrial applications. Silica sand is widely used due to its high purity, durability, and essential role in producing glass, foundry molds, and construction materials. The rising demand for flat glass, container glass, and specialty glass in automotive and construction sectors is further supporting market expansion. In addition, growing infrastructure development and industrial activities are contributing to strong market growth across Europe.

Key Market Trends

- Rising demand for glass products in construction and automotive industries is driving silica sand consumption.

- Increasing infrastructure development is supporting market expansion.

- Growing use of silica sand in industrial and foundry applications is boosting demand.

- Expansion of renewable energy applications such as solar glass is enhancing market growth.

- Technological advancements in processing and purification are improving product quality.

Segmental Insights

- Based on end use industry, the glass manufacturing segment was the largest and held 54.5% of the Europe silica sand market share in 2025. This dominance is attributed to the extensive use of silica sand in producing flat glass, container glass, and specialty glass for various industrial applications.

Regional Insights

- The Europe silica sand market is experiencing strong growth across key countries, supported by industrial demand and construction activities.

- Germany was the largest contributor, accounting for 23.2% of the Europe silica sand market share in 2025, driven by a strong manufacturing base, advanced glass industry, and increasing demand for high quality raw materials.

Competitive Landscape

The Europe silica sand market is moderately competitive, with key players focusing on resource optimization, product quality, and expansion of production capabilities to strengthen their market position. Companies are investing in advanced mining and processing technologies to meet growing demand. Prominent players in the Europe silica sand market include U S Silica Holdings Inc, Fairmount Santrol, Sibelco, Covia Holdings Corporation, Badger Mining Corporation, Emerge Energy Services LP, Quarzwerke GmbH, and Mitsubishi Corporation RtM Japan Ltd.

Europe Silica Sand Market Size

The Europe silica sand market size was valued at USD 4.38 billion in 2025 and is projected to reach USD 8.43 billion by 2034 from USD 4.71 billion in 2026, growing at a CAGR of 7.56%.

Silica sand constitutes a fundamental industrial mineral characterized by high purity silicon dioxide content essential for diverse manufacturing applications across the European continent. This material serves as the primary raw material for glass production foundry operations and hydraulic fracturing activities although the latter remains limited within Europe compared to other regions. The geological abundance of quartz deposits in nations such as Germany, France and the United Kingdom underpins the regional supply chain stability. Industrial consumption patterns reveal a steady reliance on this resource for producing flat glass container glass and specialty glass variants used in automotive and construction sectors. According to Eurostat, the European Union produced approximately 250 million tons of non-energy mineral extracts in recent years with silica sand representing a significant portion of this volume. The construction industry alone accounts for a substantial share of demand driven by urbanization trends and infrastructure renewal projects. As per the European Commission, the building sector consumes nearly 50% of all raw materials extracted in Europe which indirectly boosts silica sand requirements for mortar and concrete formulations. Environmental regulations strictly govern extraction processes ensuring sustainable mining practices while maintaining ecological balance. The strategic importance of silica sand extends beyond traditional uses into emerging technologies such as solar panel manufacturing where high purity quartz is indispensable. This dual role in conventional industries and advanced technological applications defines the current market landscape and underscores its critical position in the European industrial ecosystem.

MARKET DRIVERS Expansion of Solar Energy Infrastructure Drives High Purity Demand

The aggressive transition toward renewable energy sources across Europe significantly fuels the requirement for high purity silica sand, particularly in the photovoltaic sector, which is one of the major factors propelling the growth of the European silica sand market. Solar panels rely heavily on polysilicon, which is derived from quartzite or high purity silica sand through complex purification processes. According to the International Energy Agency, the European Union installed a record 55.9 gigawatts of solar photovoltaic capacity in 2023, which is representing a 40% increase from the previous year. This unprecedented growth trajectory requires a robust supply of raw materials capable of meeting stringent quality standards for semiconductor grade silicon. Germany, Spain, and the Netherlands lead this installation surge driven by national policies aimed at reducing carbon emissions and enhancing energy security. According to the European Solar Manufacturing Council, domestic production capabilities must expand substantially to meet the target of 30 gigawatts of annual manufacturing capacity by 2025. Each gigawatt of solar module production requires several thousand tons of high purity quartz feedstock. Consequently, mining companies are investing in upgrading processing facilities to produce silica sand with silicon dioxide content exceeding 99.9%. This shift from standard industrial grade to premium grade material creates a specialized market segment with higher value propositions. The regulatory framework supporting the Green Deal further accelerates this trend by mandating increased shares of renewable energy in the overall mix. Therefore, the direct correlation between solar capacity additions and silica sand consumption establishes a powerful demand driver that transcends traditional construction based cycles.

Revitalization of Glass Packaging Sector Supports Steady Consumption

The persistent demand for sustainable packaging solutions reinforces the consumption of silica sand in the glass manufacturing industry across Europe, which is further contributing to the expansion of the European silica sand market. Glass remains a preferred material for food and beverage packaging due to its infinite recyclability and inert properties, which preserve product quality. According to Feve, the European Container Glass Federation, the collection for recycling rate for glass packaging in the European Union reached an average of 80% in recent years. Despite high recycling rates, virgin silica sand remains essential to maintain the chemical composition and structural integrity of new glass products. The construction of new furnaces and the refurbishment of existing ones require consistent inputs of high quality sand to compensate for losses during the melting process. The beverage sector, particularly beer and wine producers, drives a significant portion of this demand given Europe’s status as a global leader in alcohol production. According to the Brewers of Europe, beer production in the European Union exceeded 34.3 billion liters in 2022, sustaining a steady need for glass bottles. Furthermore, consumer preference shifts away from single use plastics toward more environmentally friendly alternatives bolster glass usage. Regulatory measures such as the Single Use Plastics Directive encourage manufacturers to adopt reusable and recyclable packaging options. This regulatory tailwind, combined with brand commitments to sustainability, ensures that glass production volumes remain stable or grow moderately. Consequently, silica sand suppliers benefit from long term contracts with glassmakers who prioritize reliable and consistent raw material sources to ensure uninterrupted production lines.

MARKET RESTRAINTS Stringent Environmental Regulations Impose Operational Constraints

Rigorous environmental legislation across European nations imposes significant operational constraints on silica sand extraction and processing activities, which is significantly impeding the European silica sand market growth. The European Union’s Natura 2000 network protects numerous habitats that often overlap with potential mining sites, thereby restricting access to new deposits. According to the European Commission, the Natura 2000 network covers approximately 18% of the European Union’s land area and more than 8% of its marine territory. Companies must undergo extensive environmental impact assessments, which can delay project approvals by several years and increase initial capital expenditures. Additionally, the Industrial Emissions Directive mandates strict limits on dust, particulate matter, and noise pollution from mining sites, requiring advanced mitigation technologies. Compliance with these standards necessitates substantial investment in filtration systems, water treatment plants, and land rehabilitation programs. The Water Framework Directive further complicates operations by regulating water usage and discharge quality, affecting washing and classification processes essential for producing high grade silica sand. In countries like Germany and France, local communities frequently oppose new mining projects due to concerns over landscape alteration and biodiversity loss. This social license to operate becomes increasingly difficult to obtain, leading to the closure of older quarries without adequate replacements. The scarcity of permitted sites forces manufacturers to transport sand over longer distances, increasing logistics costs and carbon footprints. Moreover, the Carbon Border Adjustment Mechanism may indirectly affect the cost structure of energy intensive processing methods. These regulatory hurdles collectively restrict supply flexibility and elevate operational risks for market participants striving to balance profitability with compliance.

Volatility in Energy Costs Elevates Production Expenses

Fluctuating energy prices are further hampering the European silica sand market expansion. The extraction and refinement of silica sand involve energy intensive stages, including crushing, drying, and screening, which rely heavily on electricity and natural gas. According to Eurostat, medium sized industrial consumers in the European Union paid an average electricity price of 0.21 euros per kilowatt hour during the second half of 2023. For instance, average gas prices for industrial consumers doubled in certain periods compared to historical averages, severely impacting operational margins. Processing facilities require consistent thermal energy to remove moisture and achieve the desired grain size distribution, making them vulnerable to price shocks. Unlike some other regions, Europe lacks abundant low cost domestic energy resources, forcing reliance on imported fuels subject to global market dynamics. The transition toward renewable energy sources, while beneficial long term, involves upfront infrastructure costs that manufacturers must absorb. Small and medium sized enterprises face particular challenges in hedging against energy price fluctuations due to limited financial reserves. Higher production costs inevitably translate into increased prices for end users, potentially reducing competitiveness against imports from regions with cheaper energy profiles. Furthermore, the European Emissions Trading System imposes additional costs on carbon intensive operations, encouraging efficiency improvements but also adding financial burden. Manufacturers must continuously invest in energy efficient technologies to mitigate these costs, yet the pace of technological adoption often lags behind price increases. This persistent pressure on profit margins constrains the ability of producers to expand capacity or invest in research and development, thereby stifling market growth potential.

MARKET OPPORTUNITIES Development of Synthetic Silica Alternatives Presents New Avenues

The emergence of synthetic silica production technologies offers lucrative opportunities for the European silica sand market. Synthetic silica, produced through chemical processes, provides superior purity and controlled particle characteristics compared to natural silica sand, making it ideal for high end applications in electronics, pharmaceuticals, and cosmetics. For instance, the demand for synthetic silica is growing substantially throughout the world due to the rising demand in specialized industries. European chemical companies are well positioned to capitalize on this trend due to their advanced technical expertise and established infrastructure. The semiconductor industry in particular requires ultra-high purity silica for wafer manufacturing and encapsulation materials where natural sand cannot meet stringent contamination limits. Investments in research and development enable firms to create tailored silica products with specific surface areas and pore structures, enhancing performance in catalyst supports and battery components. The electric vehicle boom further stimulates demand for synthetic silica used in lithium ion battery anodes to improve charge capacity and cycle life. According to the European Commission, the European Battery Alliance aims to ensure that Europe can satisfy up to 90% of its battery demand with domestic production by 2030. By shifting focus from bulk commodity sales to specialized chemical products, manufacturers can achieve higher profit margins and reduce dependence on volatile construction markets. Collaborations between mining firms and chemical processors facilitate the integration of upstream raw material supply with downstream value addition. This strategic pivot allows companies to leverage existing silica resources while accessing faster growing and more resilient market segments aligned with technological innovation trends.

Recycling Initiatives Create Circular Economy Integration

Integrating silica sand into circular economy models through enhanced recycling initiatives opens significant opportunities for the European silica sand market growth. The glass industry already leads in recycling efforts, but expanding these practices to other sectors such as foundry sand reuse presents untapped potential. According to the European Commission, the European Union produces more than 2.2 billion tonnes of waste annually, which is prompting a shift toward circular management for industrial byproducts. Advanced sorting and cleaning technologies enable the recovery of high quality silica from industrial waste streams and reduce the need for virgin extraction. Regulatory incentives favoring waste reduction and resource efficiency encourage manufacturers to adopt closed loop systems. The European Circular Economy Action Plan sets ambitious targets for material reuse, prompting industries to innovate in waste management solutions. Construction companies increasingly incorporate recycled silica sand in concrete mixes and asphalt formulations, contributing to green building certifications. This shift not only lowers raw material costs but also enhances corporate sustainability profiles, appealing to environmentally conscious investors and customers. Partnerships between waste management firms and silica producers facilitate the establishment of efficient collection and processing networks. Digital platforms tracking material flows improve transparency and optimize logistics, ensuring consistent supply of recycled feedstock. By positioning recycled silica as a viable alternative to virgin material, companies can access new revenue streams and comply with tightening environmental regulations. This approach transforms waste liabilities into valuable assets, fostering resilience against resource scarcity and price volatility while aligning with broader societal goals for sustainability.

MARKET CHALLENGES Supply Chain Disruptions Threaten Raw Material Availability

Persistent supply chain disruptions are majorly challenging the expansion of the European silica sand market. Geopolitical instability and logistical bottlenecks frequently interrupt the transportation of raw materials from mining sites to processing facilities and end users. According to the European Central Bank, approximately 72% of firms in the euro area reported that supply chain constraints were a factor limiting their production during peak disruption periods. Dependence on specific transport corridors, such as rail networks and inland waterways, makes the industry vulnerable to strikes, infrastructure failures, and weather related delays. For instance, low water levels in major rivers like the Rhine have historically hindered barge traffic, causing shortages and price spikes for bulk commodities including sand. The concentration of high quality deposits in limited geographic locations exacerbates this risk as any local disruption can have widespread repercussions. Import reliance for certain grades of silica sand from outside Europe introduces additional vulnerabilities related to trade policies and customs procedures. Tariff fluctuations and non-tariff barriers can abruptly alter cost structures and availability timelines. Manufacturers operating with lean inventory systems face heightened exposure to these shocks, lacking buffer stocks to absorb delays. The just in time delivery model, while efficient under normal conditions, proves fragile during crises, leading to production stoppages in downstream industries like glass and foundries. Diversifying supply sources and investing in localized storage infrastructure offer partial mitigations but require significant capital outlay. Until supply chains become more resilient, the market will remain susceptible to unpredictable interruptions affecting reliability and customer satisfaction.

Labor Shortages Impede Operational Efficiency

Acute labor shortages in the mining and processing sectors impede operational efficiency and hinder expansion plans for silica sand producers in Europe, which is another significant challenge to the growth of the European silica sand market. Demographic trends indicate an aging workforce with insufficient young entrants replacing retiring skilled workers in technical and operational roles. According to Eurostat, the labor shortage rate in the European Union reached 2.4% across all sectors in 2024, with industrial and technical roles being particularly affected. The perception of mining as an environmentally damaging and physically demanding industry discourages younger generations from pursuing careers in this field. This skills gap affects every aspect of operations, from equipment maintenance to quality control and safety management. Companies struggle to find qualified engineers, geologists, and machine operators, leading to increased overtime costs and burnout among existing staff. The lack of specialized training programs further exacerbates the problem, leaving firms unable to upskill current employees effectively. Automation offers a potential solution but requires significant investment and technical expertise that many small operators lack. Moreover, the transition to automated systems demands a different skill set focusing on digital literacy and data analysis, which the current workforce may not possess. Labor unions also play a significant role in negotiating wages and working conditions, adding complexity to hiring decisions. High turnover rates disrupt continuity and increase recruitment costs, eroding profitability. Without addressing the human capital deficit, producers face constraints in optimizing productivity and implementing innovative practices. This structural challenge threatens the long term competitiveness of the European silica sand industry in a global context where labor availability may be more favorable.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

7.56%

Segments Covered

By End Use Industry, and Region

Various Analyses Covered

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

U.S. Silica Holdings Inc (US), Fairmount Santrol (US), Sibelco (BE), Covia Holdings Corporation (US), Badger Mining Corporation (US), Emerge Energy Services LP (US), Quarzwerke GmbH (DE), Mitsubishi Corporation RtM Japan Ltd (JP)

SEGMENTAL ANALYSIS By End Use Industry Insights

The glass manufacturing segment accounted for the leading share of 54.5% of the regional market in 2025. The growth of the glass manufacturing segment in the European market is attributed to the indispensable role of silica sand as the primary constituent in glass formulation, providing structural integrity and thermal stability. The industry relies on high purity quartz with silicon dioxide content typically exceeding 99.5% to ensure optical clarity and durability in final products. The production of container glass for food and beverage packaging serves as a primary catalyst for silica sand consumption within this segment. European consumers increasingly favor sustainable packaging solutions, driving manufacturers to prioritize glass over single use plastics. According to Feve, the European Container Glass Federation, the production of container glass in Europe reached 37.3 million tonnes in 2022, representing a 5.0% increase in tonnage compared to 2021. Each ton of glass requires approximately 1.2 tons of raw materials, with silica sand constituting nearly 70% of this batch composition. The beer, wine, and soft drink sectors are major contributors with Germany and France leading production volumes. Regulatory initiatives such as the European Union Single Use Plastics Directive mandate reductions in plastic waste, encouraging brands to switch to reusable and recyclable glass containers. This legislative push ensures consistent long term demand for high quality silica sand. Furthermore, the infinite recyclability of glass aligns with circular economy goals, although virgin sand remains necessary to maintain chemical balance during melting. As per industry data, new furnace constructions and refurbishments require substantial initial loads of premium grade sand, further bolstering market volumes. The resilience of the food and beverage sector against economic fluctuations provides a stable foundation for silica sand suppliers, ensuring predictable revenue streams despite broader market volatility.

However, the chemical production segment is anticipated to record the highest CAGR of 7.4% over the forecast period owing to the expanding application of silica based chemicals in high value industries such as electronics, pharmaceuticals, and advanced materials. Unlike bulk applications, chemical grade silica demands stringent purity levels and specialized processing, creating higher value opportunities for producers. The automotive industry’s shift toward fuel efficient and electric vehicles drives the demand for precipitated silica used in green tire manufacturing. Precipitated silica reduces rolling resistance, improving vehicle energy efficiency and extending battery range in electric models. According to the European Tyre and Rubber Manufacturers Association, consumer replacement demand for passenger car tires in Europe was approximately 213.7 million units in 2023. European regulations mandate label ratings for tire fuel efficiency, pushing manufacturers to replace carbon black with silica compounds. Each tire requires several kilograms of high purity silica to achieve optimal performance characteristics. The production of precipitated silica involves reacting sodium silicate derived from silica sand with acid, resulting in a fine white powder with controlled particle size. This process adds significant value to the raw material, transforming commodity sand into a specialized chemical ingredient. Major tire manufacturers in Germany, France, and Italy are expanding production capacities to meet evolving standards. According to industry reports, the European market for precipitated silica is expected to grow substantially as electric vehicle sales surpass traditional internal combustion engine vehicles. This transition creates a sustained upward trajectory for silica sand suppliers who can provide the necessary feedstock for sodium silicate production. The technical complexity and quality requirements create barriers to entry, allowing established players to capture premium margins while supporting the segment’s rapid expansion.

REGIONAL ANALYSIS Germany Silica Sand Market Analysis

Germany held the leading position in the Europe silica sand market by holding 23.2% of the regional market share in 2025. The dominance of Germany in the European market is attributed to the country’s robust industrial base, particularly in automotive glass and chemical manufacturing. Germany is home to some of the world’s largest glass producers and chemical companies that rely heavily on consistent supplies of high quality silica sand. The nation’s commitment to industrial innovation drives demand for specialized silica grades used in advanced applications. According to the Federal Statistical Office of Germany, the construction of new residential buildings in Germany involved 260,100 completed apartments in 2023. The automotive industry, a cornerstone of the German economy, is transitioning toward electric mobility, which requires specialized glass and silica based components. According to the German Association of the Automotive Industry, the production of electric cars in Germany grew by 59% in 2023 compared to the previous year. Furthermore, Germany’s strong environmental regulations encourage the use of recycled materials, but virgin silica sand remains critical for maintaining product quality in high end applications. The presence of major silica sand processors and distributors within the country ensures efficient logistics and reliable supply to downstream industries. Research and development initiatives in materials science further enhance the value proposition of silica based products. The country’s central location in Europe facilitates export opportunities to neighboring markets, reinforcing its status as the primary hub for silica sand consumption and processing in the region.

France Silica Sand Market Analysis

France also held a significant share of the European silica sand market in 2025. The country’s strong heritage in luxury goods, wine production, and construction drives consistent demand for glass packaging and building materials, which is propelling the French market expansion. France is one of the leading producers of wine and champagne globally, which necessitates substantial volumes of container glass. According to the International Organisation of Vine and Wine, France was the world’s largest wine producer in 2023 with an estimated production of 48 million hectoliters. The construction sector in France also contributes significantly, driven by government initiatives to renovate older buildings for energy efficiency. According to the French Ministry of Ecological Transition, approximately 373,000 new housing units were authorized for construction in France in 2023. This activity supports demand for flat glass and insulation materials containing silica sand. Additionally, France has a well developed chemical industry that utilizes silica derivatives in various applications, including cosmetics and pharmaceuticals. The country’s focus on sustainable development aligns with the circular economy principles, promoting glass recycling while maintaining the need for virgin raw materials. Strategic investments in renewable energy projects, particularly solar farms, further boost demand for high purity silica. The geographic diversity of silica deposits in France allows for localized sourcing, reducing transportation costs and environmental impact. These factors collectively establish France as a key player in the European silica sand landscape with balanced demand across multiple industrial sectors.

Italy Silica Sand Market Analysis

Italy is estimated to account for a prominent share of the European silica sand market during the forecast period due to the country’s vibrant ceramic and glass industries. Italy is renowned for its high quality ceramic tiles and sanitary ware, which require specific grades of silica for body formulation and glazing. According to Confindustria Ceramica, the Italian ceramic industry’s total sales reached 7.5 billion euros in 2023 despite a decrease in production volumes. This production volume necessitates a continuous supply of raw materials, including silica sand, feldspar, and clay. The glass sector in Italy is also prominent, particularly in the production of specialty glass for lighting and automotive applications. The country’s strong design and manufacturing capabilities support demand for premium materials that offer superior aesthetic and functional properties. Additionally, the construction and renovation sector in Italy benefits from government incentives such as the Superbonus scheme, which encouraged energy efficient upgrades. According to the Italian National Institute of Statistics, investments in the Italian construction sector increased by 4.0% in 2023. The presence of established mining operations in regions like Sardinia and Lombardy ensures reliable domestic supply. Italy’s strategic location in the Mediterranean also facilitates trade with North African and Middle Eastern markets. The combination of traditional craftsmanship and industrial innovation sustains Italy’s significant role in the European silica sand market.

Spain Silica Sand Market Analysis

Spain is estimated to hold a noteworthy share of the Europe silica sand market during the forecast period due to the country’s construction boom and tourism driven hospitality sector. Spain has experienced a resurgence in real estate development with significant investments in residential and commercial projects. According to the National Institute of Statistics of Spain, the number of mortgages constituted on dwellings increased to over 32,000 in early 2024. This growth translates into higher consumption of flat glass for windows and facades, as well as container glass for the food and beverage industry. The tourism sector, which is vital to the Spanish economy, requires extensive hospitality infrastructure, including hotels and restaurants that utilize large volumes of glassware and packaging. Additionally, Spain is emerging as a leader in renewable energy, particularly solar power. According to Red Eléctrica, solar photovoltaic energy became the main source of electricity generation capacity in Spain in 2024, exceeding 25 gigawatts. This expansion drives demand for high purity silica used in solar panel manufacturing. The country possesses abundant silica sand reserves, particularly in the Catalonia and Andalusia regions, enabling cost effective extraction and processing. Government policies supporting sustainable construction and energy transition further reinforce market growth. Spain’s competitive labor costs and strategic port facilities also enhance its export potential within Europe. These dynamics position Spain as a dynamic and growing market for silica sand with diverse application drivers.

United Kingdom Silica Sand Market Analysis

The United Kingdom is another notable regional segment in the Europe silica sand market. The country’s mature construction sector and strong glass manufacturing industry form the backbone of silica sand demand. Despite economic uncertainties, the UK continues to invest in infrastructure projects, including housing, transport, and energy networks. According to the Office for National Statistics, the annual construction output in the UK increased by 2.1% in 2023, driven largely by new work. The glass industry in the UK is well established, with major producers supplying container and flat glass to domestic and international markets. The beverage sector, particularly beer and spirits, drives consistent demand for container glass. According to the British Beer and Pub Association, the UK produced approximately 3.8 billion liters of beer in 2022. Additionally, the UK’s commitment to net zero emissions by 2050 drives investments in renewable energy and energy efficient buildings. This transition supports demand for specialized silica applications in solar panels and insulation materials. The country’s regulatory framework emphasizes sustainable sourcing and environmental protection, influencing mining practices and supply chain strategies. The presence of high quality silica deposits in regions such as Surrey and Norfolk provides a reliable domestic supply base. Post Brexit trade adjustments have prompted companies to optimize local supply chains, reducing dependence on imports. These factors collectively sustain the UK’s position as a key market for silica sand with a focus on quality and sustainability.

COMPETITIVE LANDSCAPE

The Europe silica sand market exhibits a moderately consolidated competitive landscape characterized by the presence of established multinational corporations and regional players. Leading companies compete based on product quality reliability of supply and adherence to environmental standards. The high capital intensity of mining and processing operations creates barriers to entry limiting the number of new participants. However local producers maintain relevance by offering cost effective solutions for specific regional needs. Competition intensifies in specialized segments where technical expertise and customization capabilities are critical differentiators. Companies increasingly focus on sustainability initiatives to align with regulatory frameworks and customer preferences. Strategic collaborations and mergers facilitate access to new technologies and markets enhancing competitive positioning. Price volatility in energy and logistics sectors influences competitive dynamics prompting firms to optimize cost structures. Innovation in recycling and circular economy models offers new avenues for differentiation. Overall the market remains dynamic with players continuously adapting strategies to address evolving industrial demands and regulatory pressures while striving for operational excellence and sustainable growth.

KEY MARKET PLAYERS

Some of the notable key players in the Europe silica sand market are

- U.S. Silica Holdings Inc

- Fairmount Santrol

- Sibelco

- Covia Holdings Corporation

- Badger Mining Corporation

- Emerge Energy Services LP

- Quarzwerke GmbH

- Mitsubishi Corporation RtM Japan Ltd

Top Players in the Market

- Sibelco stands as a global leader in material solutions with a significant footprint in the European silica sand sector. The company leverages its extensive network of quarries and processing facilities to supply high purity materials for glass foundry and chemical applications. Sibelco focuses on sustainable mining practices and circular economy initiatives to enhance its environmental profile. Recent investments in digitalization and automation have optimized operational efficiency across its European sites. The company actively collaborates with customers to develop tailored silica solutions that meet stringent industry standards. Its commitment to research and development ensures continuous innovation in product quality and application performance. Sibelco’s strategic partnerships with key industrial players strengthen its supply chain resilience. By prioritizing customer centric services and technical expertise the company maintains a competitive edge. These efforts solidify its reputation as a reliable partner for diverse industrial needs across the continent.

- Quarzwerke Group is a prominent player specializing in high quality quartz and silica sand products for various industrial sectors. The company operates several production sites in Europe ensuring consistent supply to glass ceramic and construction industries. Quarzwerke emphasizes vertical integration by controlling the entire value chain from extraction to final processing. This approach allows for strict quality control and customization capabilities. Recent expansions in processing capacity have enabled the company to meet growing demand for specialized silica grades. The group invests heavily in environmental protection measures including water recycling and land rehabilitation programs. Its focus on sustainability aligns with European regulatory requirements and customer expectations. Quarzwerke also engages in joint ventures to explore new market opportunities and technologies. By maintaining strong relationships with downstream manufacturers the company secures long term contracts. These strategic moves enhance its market presence and operational stability in the competitive European landscape.

- Euroquarz is a leading supplier of silica sand and quartz products serving the European market with a focus on quality and reliability. The company provides materials for foundry glassmaking and sports turf applications among others. Euroquarz operates modern processing facilities equipped with advanced technology to ensure product consistency. Recent initiatives include upgrading logistics infrastructure to improve delivery efficiency and reduce carbon emissions. The company prioritizes customer service by offering technical support and customized solutions for specific industrial needs. Euroquarz actively participates in industry associations to promote best practices and sustainable development. Its commitment to environmental stewardship is evident in its adherence to strict ecological standards. The company also explores innovative applications for silica sand in emerging sectors such as renewable energy. By fostering strong partnerships with clients and suppliers Euroquarz enhances its market position. These efforts demonstrate its dedication to meeting evolving industry demands while maintaining operational excellence.

Top Strategies Used by the Key Market Participants

Key players in the Europe silica sand market primarily employ vertical integration strategies to control supply chains and ensure quality consistency. Companies invest heavily in sustainable mining practices to comply with stringent environmental regulations and enhance corporate reputation. Strategic partnerships with downstream industries such as glass and automotive sectors help secure long term contracts and stabilize demand. Expansion into high value added segments like synthetic silica and specialized chemical grades allows firms to diversify revenue streams. Investment in digital technologies and automation improves operational efficiency and reduces production costs. Geographic diversification through acquisitions or joint ventures strengthens market presence and mitigates regional risks. Focus on research and development drives innovation in product applications particularly in renewable energy and electronics. These strategies collectively enable companies to maintain competitiveness and adapt to changing market dynamics effectively.

MARKET SEGMENTATION

This research report on the European silica sand market has been segmented and sub-segmented based on categories.

By End Use Industry

- Construction

- Glass Manufacturing

- Filtration

- Foundry

- Chemical Production

- Paints and Coatings

- Ceramics and Refractories

- Oil and Gas

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe