Has Changed Its Investment Story")

-

Cameco, the world’s second-largest uranium miner, has recently drawn attention as it expands beyond mining into enrichment and gains exposure to nuclear services through its stake in Westinghouse Electric, aligning its business more closely with the global nuclear build-out already underway.

-

An interesting angle is how this broader exposure to the nuclear fuel cycle may help lessen Cameco’s dependence on uranium spot prices, potentially smoothing earnings as governments pursue decarbonization and energy security policies.

-

We’ll now examine how Cameco’s push into enrichment and nuclear services could influence the company’s existing investment narrative built around uranium demand.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

To own Cameco, you have to believe the nuclear “renaissance” translates into sustained demand across the full fuel cycle, not just mined uranium. The latest move into enrichment and nuclear services via Westinghouse ties the story even more tightly to long term reactor build outs, while the key near term catalyst remains follow through on utility contracting. The biggest risk still lies in project delays and bottlenecks that could slow uranium and fuel services demand; this news does not remove that risk.

The recent long term agreement to supply nearly 22 million pounds of U3O8 to India over nine years is especially relevant here. It reinforces Cameco’s role as a core supplier to countries expanding nuclear capacity and helps underpin future volumes ahead of some of the proposed reactors reaching final investment decision. In the context of Cameco’s growing exposure to enrichment and Westinghouse services, this type of contract ties the traditional uranium narrative to the newer parts of the business.

Yet even with all this momentum, investors should be aware that Cameco’s heavy reliance on timely nuclear project approvals and contracting could…

Read the full narrative on Cameco (it’s free!)

Cameco’s narrative projects CA$4.3 billion revenue and CA$1.6 billion earnings by 2029. This requires 7.6% yearly revenue growth and an earnings increase of about CA$1.0 billion from CA$589.6 million today.

Uncover how Cameco’s forecasts yield a CA$174.76 fair value, a 9% upside to its current price.

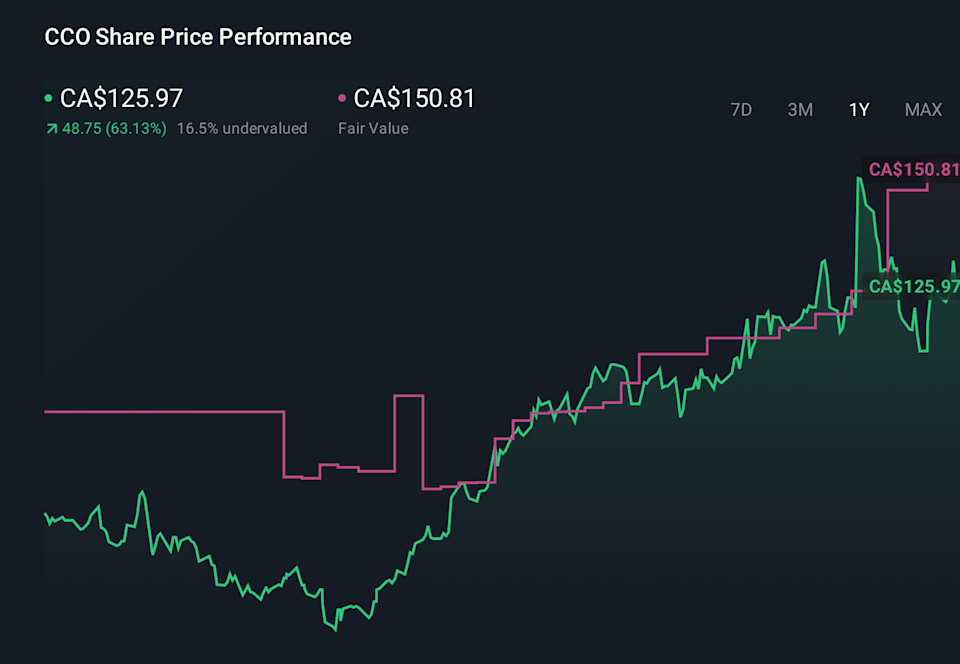

TSX:CCO 1-Year Stock Price Chart

Some of the lowest analysts were assuming roughly flat revenue around CA$3.4 billion and CA$1.3 billion in earnings by 2029, which is far more cautious than consensus and highlights how views on Westinghouse driven upside and contracting momentum can differ widely, especially now that this new fuel cycle news could reshape those expectations.