Valuation After Regulatory Push On Transmission Rules And Compliance Update")

Xcel Energy (XEL) is back in focus after helping lead a utility coalition pressing federal regulators to ease rules that slow new transmission projects, alongside a recent favorable ruling on a hydroelectric compliance issue.

For investors, the story here is less about short term headlines and more about how regulatory timing and oversight can shape the pace and economics of future grid and generation investments that underpin the business.

See our latest analysis for Xcel Energy.

At a share price of US$82.38, Xcel Energy has a 90 day share price return of 10.93%, while the 1 year total shareholder return of 22.18% and 5 year total shareholder return of 37.18% point to momentum that has been building around its regulated earnings profile, transmission build out plans, and steady flow of regulatory decisions.

If you are watching how grid investment stories are playing out, it can be useful to scan other power infrastructure names using our dedicated screener for 30 power grid technology and infrastructure stocks

With Xcel Energy trading at US$82.38, sitting on solid recent returns and only a modest 9% discount to the average analyst price target, the key question is whether there is still an opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 8% Undervalued

Compared with the last close of $82.38, the most followed narrative anchors on a fair value of about $89.53, built on a detailed earnings and capital investment roadmap.

Constructive regulatory outcomes and a strong history of allowed returns underpin Xcel’s predictable cash flow, while the company’s large pipeline of capital investments and increasing customer demand should drive consistent earnings growth, contrary to current market undervaluation.

Curious what underpins that conviction on future earnings and cash flows? The narrative leans on specific revenue growth, margin expansion, and a richer future earnings multiple.

Result: Fair Value of $89.53 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, that upside story can be tested quickly if wildfire liabilities escalate or if key renewable and transmission projects run into tougher or slower regulatory approvals.

Find out about the key risks to this Xcel Energy narrative.

Another View: What Earnings Multiples Are Signaling

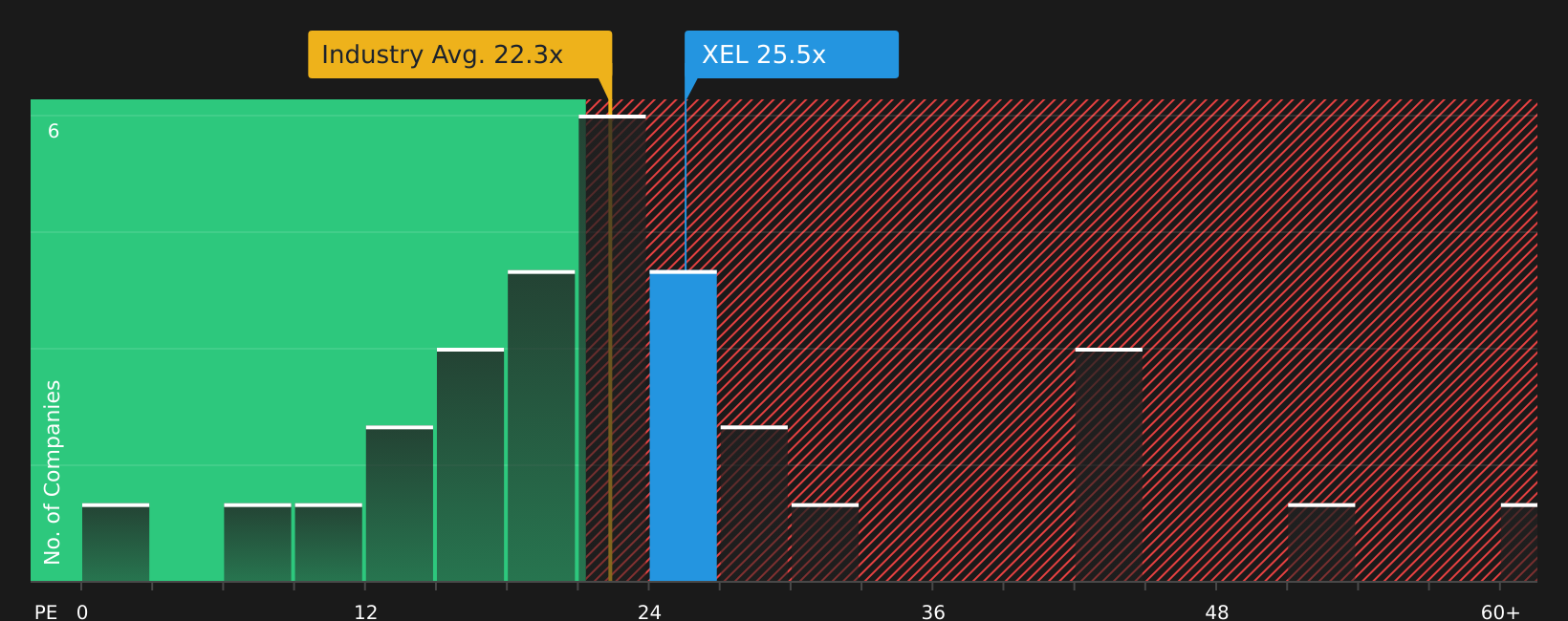

The analyst narrative leans on future earnings power to argue Xcel Energy is about 8% undervalued. However, the current P/E of 25.5x is higher than the US Electric Utilities industry at 22.4x and close to an estimated fair ratio of 26.7x. This raises the question of how much upside is really left in the multiple.

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:XEL P/E Ratio as at Apr 2026Next Steps

NasdaqGS:XEL P/E Ratio as at Apr 2026Next Steps

Opinions in this article pull in both directions, which is why it helps to act promptly and weigh the data for yourself, starting with the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Xcel Energy has your attention, do not stop here. Use focused stock lists to spot other opportunities that might suit your goals and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com