Amid the conflict in the Middle East, many investors are understandably confused about how to move forward. This is exacerbated by the current market environment. At 38, the Shiller P/E ratio is far above historical averages, and a massive decline could occur if market conditions deteriorate.

Nonetheless, investors should remember that the overall market has recovered from every past downturn. Additionally, while longtime CEO Warren Buffett raised a record amount of cash before retiring from Berkshire Hathaway, he retained considerable stock holdings.

That approach indicates that investors should stay the course even if they preserve optionality by holding considerable amounts of cash. Regardless of what happens in the near term, these three artificial intelligence (AI) stocks should hold investors in good stead as they navigate an uncertain environment.

Image source: Getty Images.

1. Nvidia

Nvidia (NVDA +2.59%) remains in a strong position to preserve capital as it maintains its dominance in the AI accelerator market. It has become an essential company in advancing AI, and rather than starving for business, it is instead struggling to keep up with the demand for its chips.

Admittedly, if one focuses on the stock chart over the last five years, they might assume it is due for a sell-off. Fortunately, its business conditions and financials appear to indicate otherwise.

Today’s Change

(2.59%) $4.76

Current Price

$188.67

Market Cap

$4.6T

Day’s Range

$184.32 – $190.00

52wk Range

$95.04 – $212.19

Volume

5.9M

Avg Vol

179M

Gross Margin

71.07%

Dividend Yield

0.02%

Despite a market cap of around $4.4 trillion, the company grew its revenue by 65% in fiscal 2026 (ended Jan. 25). Also, costs and expenses kept pace with revenue, and its $120 billion in net income also rose 65% yearly.

Still, since its stock rose by 85% over the last year, its valuation did not increase that much, and its 37 P/E ratio is arguably cheap given its rate of profit growth.

Also, amid its successes, it holds $63 billion in liquidity, giving it tremendous optionality should business conditions deteriorate. That positions Nvidia stock well to preserve one’s capital long term, making it a smart holding for value investors.

2. Amazon

Amazon (AMZN +2.02%) is also in a position of strength due to its two primary businesses: e-commerce and cloud computing. Since Amazon sells a wide variety of items, sales should remain steady even if an economic downturn prompts consumers to spend more carefully.

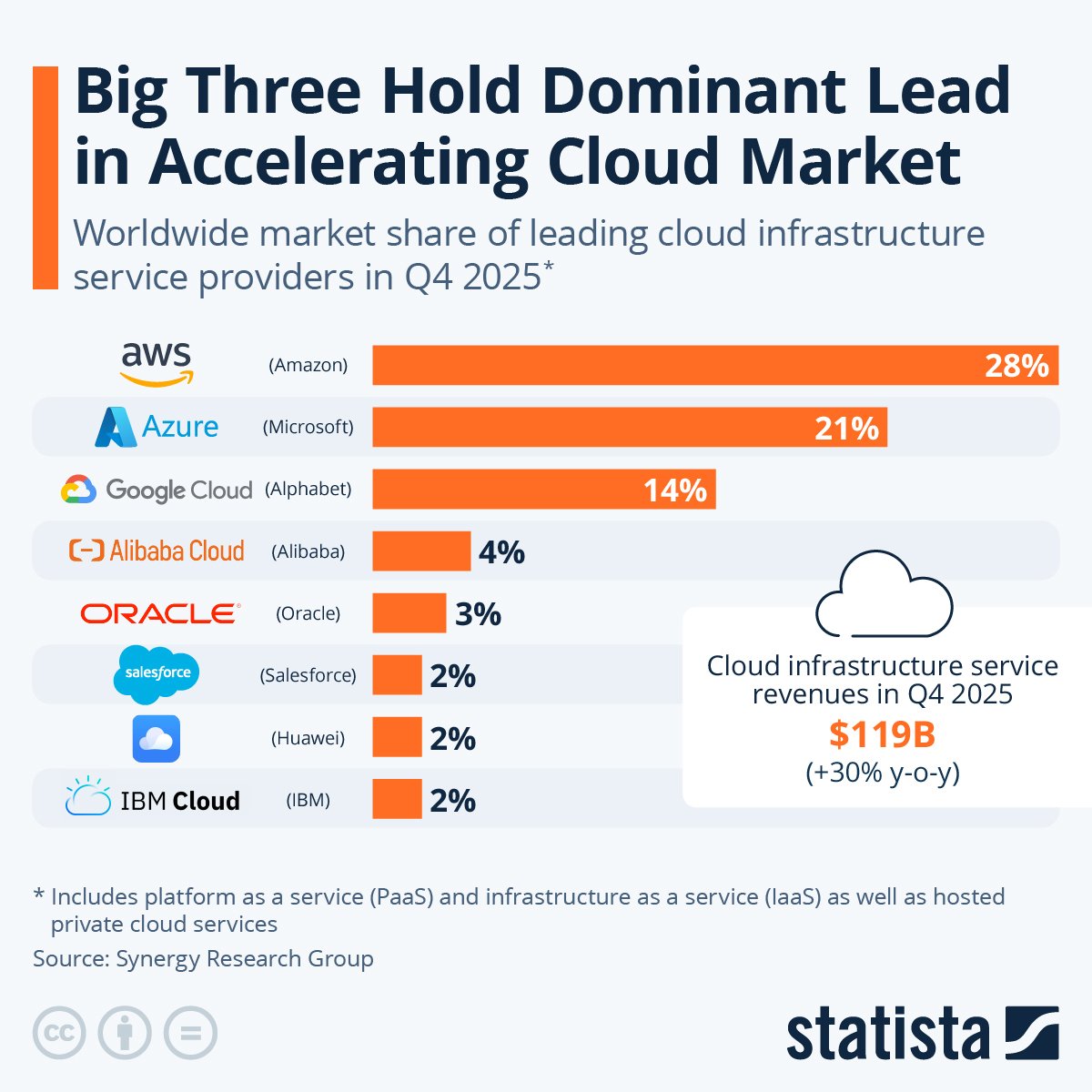

Data source: Statista.

Moreover, AWS remains the market leader in cloud computing. According to Grand View Research, the cloud industry is expected to grow at a compound annual growth rate (CAGR) of 16% through 2033, making it likely to continue growing even in a down economy.

Thus, despite a staggering $200 billion investment in property and equipment this year, Amazon holds $127 billion in liquidity. That enables it to afford this spending and, likely, whatever it needs to navigate the current environment.

Today’s Change

(2.02%) $4.73

Current Price

$238.38

Market Cap

$2.6T

Day’s Range

$235.21 – $240.43

52wk Range

$165.28 – $258.60

Volume

57M

Avg Vol

51M

Gross Margin

50.29%

Additionally, after increasing revenue by 12% in 2025, it reported almost $78 billion in net income for the year, a 31% rise over the same period. That indicates its massive investments may already be paying off for the tech giant.

Finally, its P/E ratio of 31 takes its valuation near multi-year lows. That earnings multiple makes it all the more likely Amazon will protect (and likely grow) one’s investments in these uncertain times.

3. Apple

Apple (AAPL 0.01%) is a longtime favorite of Buffett, who made it Berkshire’s largest holding. Even though he dramatically reduced this holding in recent quarters, he recently expressed some regret at selling.

Apple’s business likely remains the reason why. Its iPhone and iOS operating system are one of the leading smartphone ecosystems. Also, since it holds $132 billion in fair value liquidity, the company holds the resources necessary to maintain its place in the market without taking major risks.

Furthermore, revenue growth has recovered amid an iPhone upgrade cycle. In the first quarter of fiscal 2026 (ended Dec. 27, 2025), revenue rose by 16%, and this included a 23% increase in iPhone sales. That compares to the 6% overall revenue growth and the 4% rise in iPhone sales in fiscal 2025. Also, with fiscal Q1 profits up 16% yearly to $42 billion, the revenue growth has translated into higher profits.

Today’s Change

(-0.01%) $-0.02

Current Price

$260.47

Market Cap

$3.8T

Day’s Range

$259.03 – $262.17

52wk Range

$189.81 – $288.62

Volume

1.2M

Avg Vol

47M

Gross Margin

47.33%

Dividend Yield

0.40%

At about 32 times earnings, Apple stock is not as cheap as it used to be. Still, with these reemerging tailwinds, Buffett is likely right to wish that his company still held more Apple shares.