Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

-

Wondering if Align Technology at around US$190 per share still offers value or if the easy gains are gone? This article focuses squarely on what the current price might mean for you.

-

The stock has returned 9.8% over the last week and 30 days, 21.8% year to date and 10.9% over the past year, but those figures sit alongside a 46.5% decline over 3 years and a 69.3% decline over 5 years.

-

These mixed returns give important context for anyone assessing what the current valuation might be pricing in, especially for readers weighing shorter term momentum against longer term share price pressure. Together, they raise fair questions about how much optimism or caution may already be reflected in today’s market price.

-

Align Technology currently scores 1 out of 6 on Simply Wall St’s valuation checks. The next sections walk through traditional valuation approaches and then finish with a broader framework that can help you make better sense of that score.

Align Technology scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

A Discounted Cash Flow model takes expected future cash flows, then discounts them back to today to estimate what the business might be worth right now. It is essentially a cash flow based “what are you paying for” check.

For Align Technology, the latest twelve month Free Cash Flow is about $459 million. Analysts provide explicit forecasts only for the next few years, with Simply Wall St extending those projections further out. For example, projected Free Cash Flow for 2029 is $851.857 million, with intermediate years such as 2026 and 2027 also modeled in hundreds of millions of dollars.

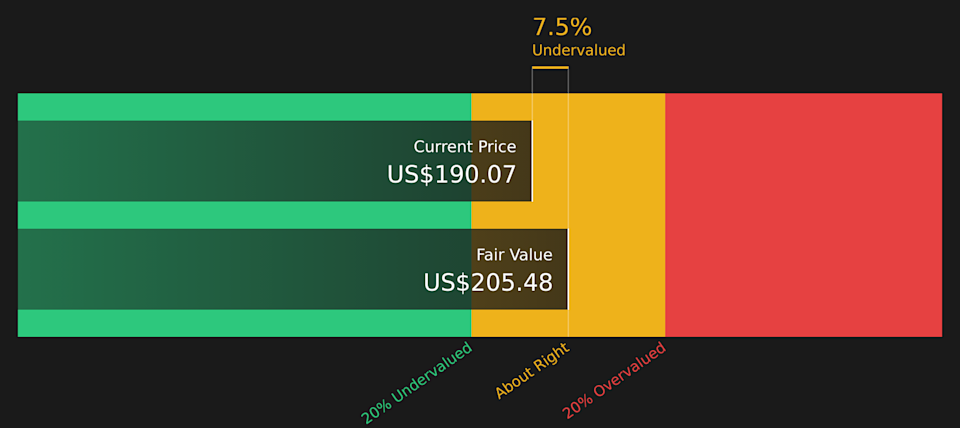

Using a 2 Stage Free Cash Flow to Equity approach, these cash flows are discounted back to today to arrive at an estimated intrinsic value of about $205.48 per share. Compared with a current share price around $190, the DCF suggests the stock is roughly 7.5% undervalued. This sits in the “close enough” zone rather than clearly cheap or expensive.

Result: ABOUT RIGHT

Align Technology is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment’s notice. Track the value in your watchlist or portfolio and be alerted on when to act.

ALGN Discounted Cash Flow as at Apr 2026

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Align Technology.

For profitable companies, the P/E ratio is a useful shorthand because it ties what you pay directly to the earnings the business is generating today. The higher the expected growth and the lower the perceived risk, the more investors are usually willing to pay in terms of a higher P/E multiple, and the reverse is also true.

Align Technology currently trades on a P/E of 33.17x. That sits above both the Medical Equipment industry average of 26.02x and the peer average of 24.54x, which might initially look rich if you only compare against those simple benchmarks.

Simply Wall St’s Fair Ratio for Align Technology is 26.41x. This is a proprietary estimate of what a P/E multiple could look like after considering factors such as earnings growth, profit margins, industry classification, company size and identified risks. Because it adjusts for these company specific drivers, the Fair Ratio can give a more tailored anchor than a broad industry or peer average alone.

Set against that Fair Ratio of 26.41x, the current P/E of 33.17x screens as higher than what those fundamentals might justify.

Result: OVERVALUED

NasdaqGS:ALGN P/E Ratio as at Apr 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story to the numbers by linking your view of Align Technology’s business, its forecast revenue, earnings and margins, to a Fair Value that you can compare with today’s price, update automatically as new news or earnings arrive, and tailor to your own outlook, whether that looks closer to a cautious Fair Value around US$154.62 or a more optimistic Fair Value near US$225, all available directly on the Align Technology Community page where you can see how different investors frame the same stock.

For Align Technology, however, we will make it really easy for you with previews of two leading Align Technology Narratives:

Together they frame the current share price from both a more optimistic and a more cautious angle so you can decide which story feels closer to your own view of the business.

🐂 Align Technology Bull Case

Fair value in this narrative: US$201.69 per share.

Current price vs this fair value: about 5.7% below the narrative fair value, using the latest close of US$190.07.

Revenue growth assumption: 4.94% a year.

-

Analysts in this case see Align extending into more clinical segments and geographies, with Invisalign adoption and digital dentistry tools widening the addressable market.

-

They build in higher future profit margins, supported by automation, regionalized production and deeper integration of scanners and AI supported treatment planning.

-

The narrative centers on a consensus price target of US$201.69, with a range from US$169.00 to US$225.00, and encourages you to test those assumptions against your own expectations for growth, margins and risk.

🐻 Align Technology Bear Case

Fair value in this narrative: US$154.62 per share.

Current price vs this fair value: about 22.9% above the narrative fair value, using the latest close of US$190.07.

Revenue growth assumption: 4.80% a year.

-

This view highlights that Align operates in a cost sensitive world where inflation, pressure on discretionary spending and cheaper clear aligner alternatives make premium pricing harder to sustain.

-

It leans on clinical quality and technology as the core advantages, but questions how far practitioners and patients will stretch on price when lower cost competitors and regional differences in affordability are taken into account.

-

The author focuses on execution risk around margins, global expansion and competition, and sees current market expectations as demanding clear proof that earnings quality and brand strength can hold up against these pressures.

If you find yourself agreeing more with one narrative than the other, that is a useful signal about how you personally weigh Align Technology’s growth potential, competitive threats and current price.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Align Technology on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Do you think there’s more to the story for Align Technology? Head over to our Community to see what others are saying!

NasdaqGS:ALGN 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ALGN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

After Recent Share Price Rebound?")