?")

- Curtiss-Wright recently reported its first-quarter 2026 results, with revenue of US$913.69 million and net income of US$128.19 million, alongside completing a multi-year US$1.38 billion share repurchase program covering 17.52% of its shares.

- The company also advanced its role in next-generation nuclear technology by moving into prototype manufacturing of key systems for X-energy’s Xe-100 reactor, underlining its exposure to the emerging advanced nuclear market.

- We’ll now examine how the upgraded full-year outlook, backed by broad-based Q1 momentum, may influence Curtiss-Wright’s investment narrative.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

Curtiss-Wright Investment Narrative Recap

To own Curtiss-Wright, you need to believe in sustained demand for its mission-critical defense and nuclear hardware, supported by a robust backlog and disciplined capital returns. The Q1 2026 beat and upgraded guidance reinforce that near term earnings momentum remains the key catalyst, while dependence on large defense and nuclear programs is still the biggest risk. The completion of the US$1.38 billion buyback does not materially change that risk profile, but it does tighten the share base.

The shift from design to prototype manufacturing for X-energy’s Xe-100 reactor systems looks especially relevant here, because it puts real engineering content behind the nuclear growth story that underpins many bullish theses. For investors focused on catalysts, this concrete progress in advanced nuclear complements the raised full year outlook and growing order book, while still leaving open questions about how policy or project delays could affect future nuclear-related revenues.

Yet alongside the positive guidance and nuclear momentum, investors should be aware of how sensitive Curtiss-Wright remains to shifts in large defense and nuclear spending programs…

Read the full narrative on Curtiss-Wright (it’s free!)

Curtiss-Wright’s narrative projects $4.0 billion revenue and $593.3 million earnings by 2028. This requires 6.8% yearly revenue growth and roughly a $141.9 million earnings increase from $451.4 million today.

Uncover how Curtiss-Wright’s forecasts yield a $711.43 fair value, in line with its current price.

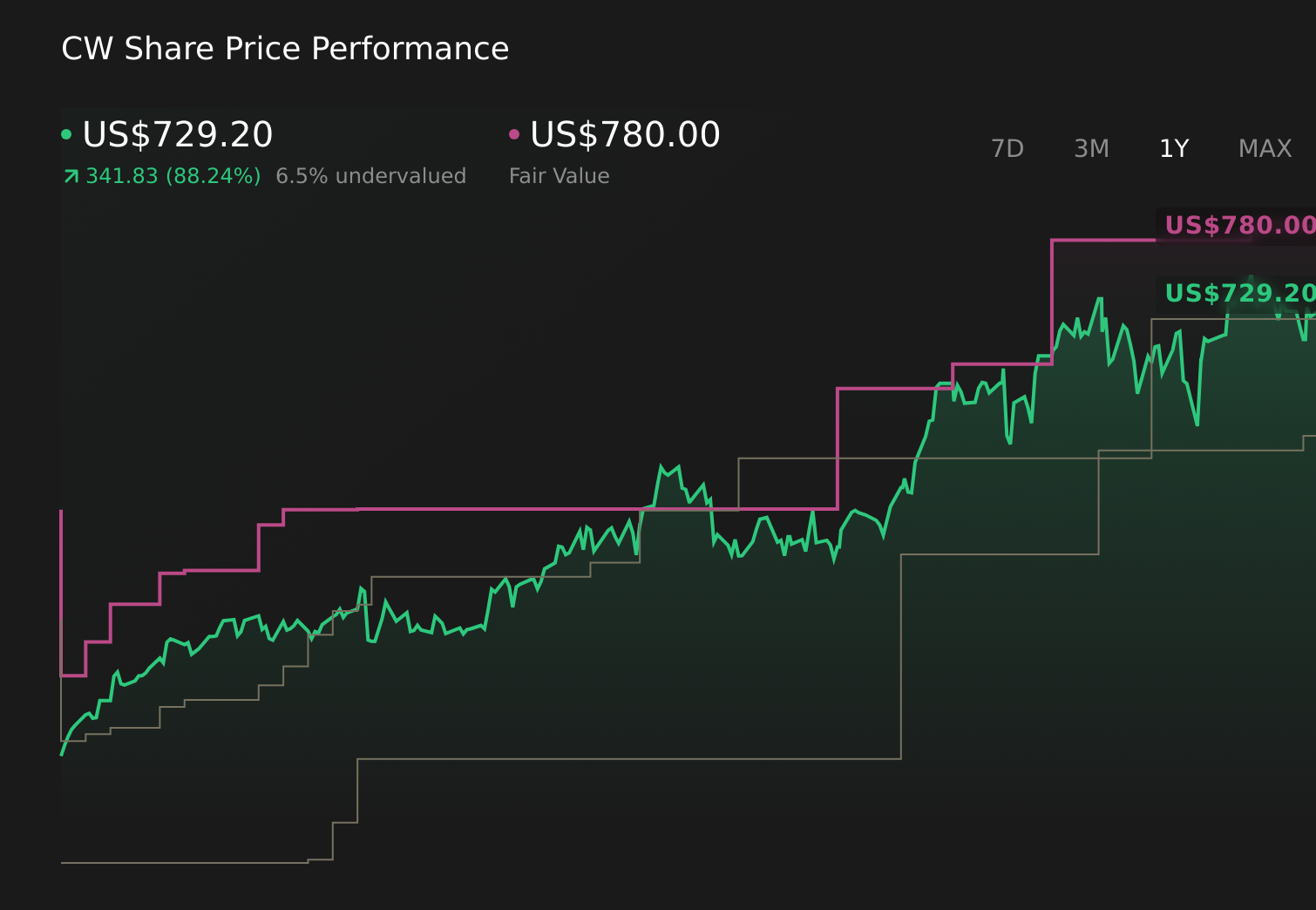

Exploring Other Perspectives CW 1-Year Stock Price Chart

CW 1-Year Stock Price Chart

Some of the most optimistic analysts were already assuming Curtiss-Wright could reach about US$4.5 billion in revenue and US$741.5 million in earnings by 2029, and this upbeat view leans heavily on the same defense and nuclear contract pipeline that recent Q1 results highlight. You may see this as far more optimistic than the baseline narrative, and the latest earnings surprise and Xe-100 progress could either support or challenge those assumptions once analysts update their models.

Explore 4 other fair value estimates on Curtiss-Wright – why the stock might be worth 44% less than the current price!

Decide For Yourself

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

- A great starting point for your Curtiss-Wright research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Curtiss-Wright research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Curtiss-Wright’s overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com