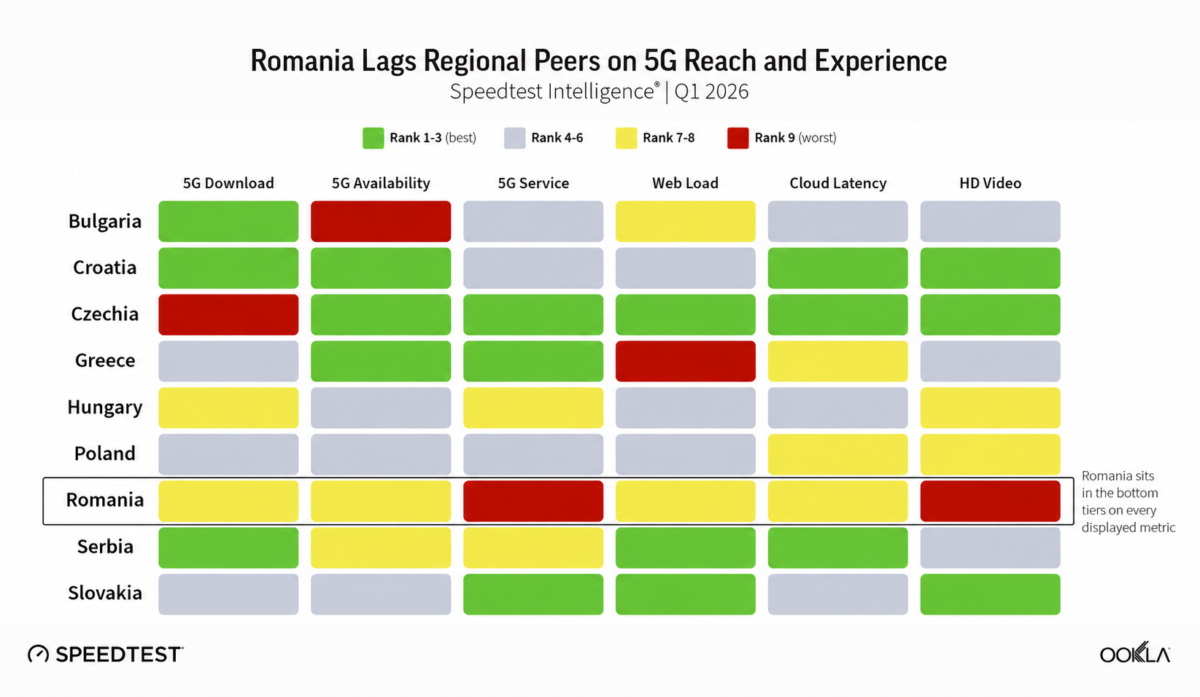

Romania ranks poorly in mobile performance compared to its Central and Eastern European peers.

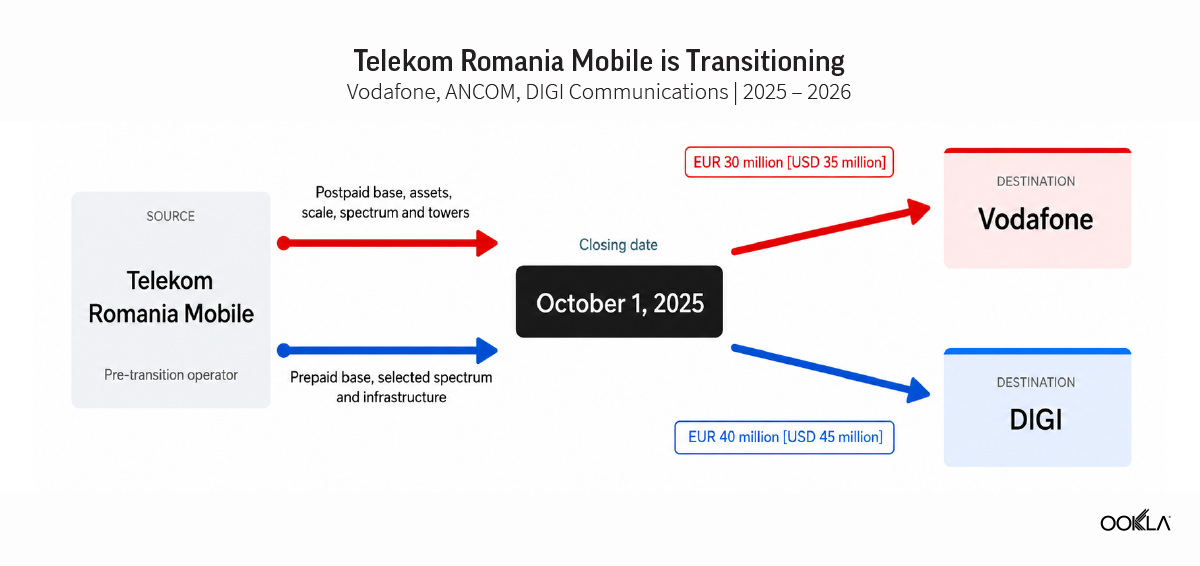

Romania’s mobile market has entered a more consequential phase of its 5G cycle. The country has moved beyond the initial spectrum allocation stage, 5G adoption is increasing, and the market structure changed after Vodafone and DIGI divided Telekom Romania Mobile between them in 2025. Vodafone took the postpaid and business customer base and much of the network infrastructure, while DIGI took the prepaid business and selected spectrum and tower assets.

Q1 2026 is the first full quarter of the three-mobile operator structure in Romania. Analysis of Speedtest Intelligence data reveals that the country still has a material gap to close, with Romania ranking near the bottom of Central and Eastern European (CEE) peers for overall mobile performance and 5G coverage, and with quality of experience (QoE) results weaker than its fixed broadband reputation might lead policymakers or enterprise users to expect.

It is still early post-consolidation, but the first signals are emerging on whether Orange, Vodafone, and DIGI can turn different spectrum portfolios, site grids, refarming strategies, and integration paths into better mobile service.

Key Takeaways:

- Romania’s mobile performance gap is driven as much by 5G reach as by headline speed. In Q1 2026, 5G Availability stood at 39%, placing Romania toward the lower end among Central and Eastern European peers. That limited 5G reach helps explain why Romania’s median mobile download speed was also the lowest in the group, at 78.43 Mbps.

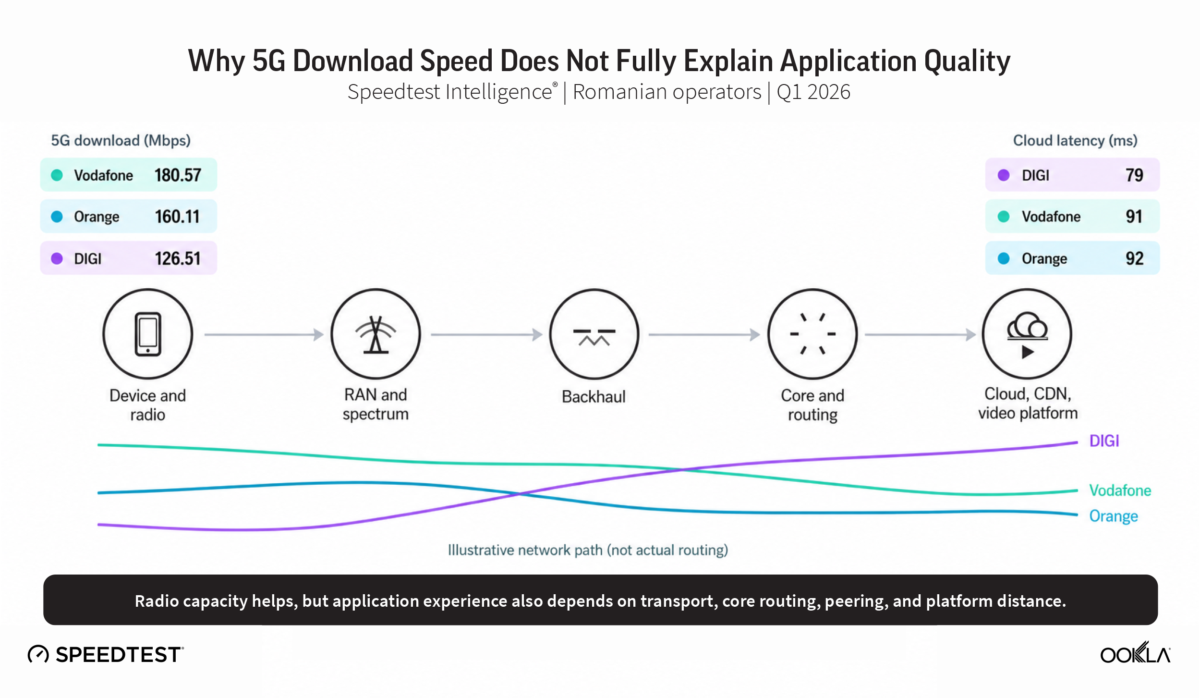

- Orange has the broadest 5G footprint among Romania’s operators, but this has not automatically translated into application latency leadership. Orange led on 5G Availability (57%) and overall median mobile download speed (97.70 Mbps) in Q1 2026, but it lagged on real-world latency outcomes measured to cloud infrastructure endpoints like AWS and Azure.

- Vodafone’s 5G footprint is narrower, but its 5G throughput result points to substantial capacity where 5G is deployed. Vodafone recorded median 5G download speeds of 180.57 Mbps in Q1 2026 (doubling year on year), with 36% 5G Availability, making network integration and spectrum refarming after the Telekom Romania Mobile deal central to further footprint expansion.

- DIGI’s results show why quality of experience does not always map neatly to download speed. DIGI recorded a lower 5G median download speed of 126.51 Mbps, but it had the highest Romanian operator 5G upload result at 33.03 Mbps and the lowest 5G cloud latency at 79 ms, potentially reflecting the merits of a dense fiber network, deeper peering or better optimized traffic routing and interconnection.

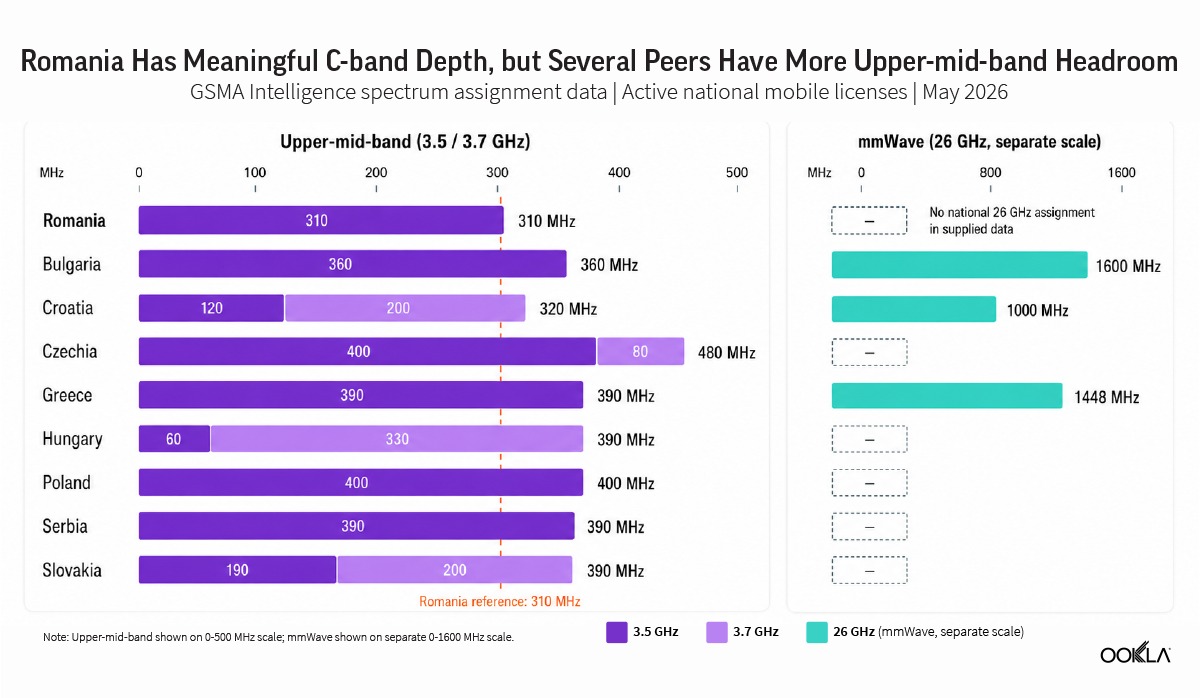

- Romania’s 5G gap is not only a question of rollout. It also reflects a thinner spectrum base in operators’ commercial portfolios. Only 30 MHz of national 700 MHz spectrum was assigned in the 2022 5G auction, around half the CEE norm of 60 MHz, after Telekom Romania Mobile chose not to apply. Romania also has the lowest assigned C-band depth below 3.7 GHz in the peer group, at 310 MHz.

Telekom Romania split creates a new market dynamic

Romania consolidated from four mobile operators to three on 1 October 2025, when Vodafone Romania completed a €30 million (US$34 million) purchase of Telekom Romania Mobile Communications from OTE and DIGI Romania paid €40 million (US$45 million) for a parallel carve-out from the same target. Vodafone took the legal entity, the postpaid base, and most of the spectrum.

DIGI took the prepaid book, residual towers, and spectrum blocks at 900, 1800, 2100, and 2600 MHz. The Romanian Competition Council cleared the deal on 28 July 2025, conditional on continued MVNO wholesale access, Orange co-location, DIGI road-coverage investment, and a four-year compliance trustee. ANCOM issued the modified licences on 8 October.

The deal closed three years of strategic re-orientation by parent OTE, which had retained the mobile arm after selling fixed-line Telekom Romania to Orange in 2021. That earlier sale produced a single convergent Orange footprint, legally merged on 1 June 2024. OTE ran Telekom Romania Mobile as a sub-scale fourth challenger with roughly 12% of active SIMs by end-2024, and its non-participation in the November 2022 5G auction left Romania with 30 MHz at 700 MHz, half the CEE norm.

The transaction did not come out of nowhere. Vodafone had already signaled that Romania was a market where consolidation could reshape the business. In its FY25 results, Vodafone Group disclosed a combined €4.5 billion goodwill impairment across Germany and Romania, with Romania specifically identified as a market offering “the opportunity to drive further consolidation.” The Telekom Romania Mobile transaction then became the mechanism for that consolidation, with Vodafone strengthening its mobile position and DIGI acquiring assets that helped address a long-standing weakness in its mobile spectrum base.

By Vodafone’s H1 FY26 results on 11 November 2025, 250,000 Telekom Romania customers had been migrated. The Telekom brand persists pending full legal merger into Vodafone after 1 July 2026. For our Q1 2026 analysis, Telekom Romania is treated as transitional rather than a continuing peer.

5G speeds are lagging but year-over-year results show promise

Romania’s overall median mobile download speed of 78.43 Mbps in Q1 2026 placed it last among the eight CEE countries examined in our analysis . The gap to the leader was large. Bulgaria delivered 196.35 Mbps (among the highest in Europe and across advanced liberal democracies), Serbia 134.92 Mbps, and Croatia 126.02 Mbps. Hungary, with its similar three-operator structure and rural geography, reached 83.24 Mbps. Romania’s 5G median of 144.55 Mbps ranked second-last, ahead only of Czechia at 113.67 Mbps, in a cohort where Serbia delivered 340.92 Mbps and Bulgaria 303.41 Mbps on 5G.

Analysis of median multi-server latency outcomes tells a similar story. Romania at 41 ms had the highest median latency in the CEE cohort, with the next-worst result (Poland, 39 ms) measurably ahead. On 5G, Romania at 39 ms also sat at the high-latency end of the cohort.

Our quality of experience (QoE) data reinforces this conclusion. Romania ranked last among the peer cohort for overall web page load times and second-last for 5G web page load times to popular websites. It also ranked near the bottom for 5G cloud latency (measuring to major hyperscaler endpoints like AWS, Azure, Google Cloud and Oracle) and for the share of mobile users who experience Full HD video resolution (1080p or higher) on 5G.

These results suggest that the country’s 5G gap is not just a radio access issue but also an application path issue shaped by deeper factors like transport, routing, peering, CDN placement, core architecture, and how much of the user journey actually stays on a well-performing 5G layer.

Vodafone’s 5G Speeds Doubled After Absorbing Telekom Romania’s Spectrum

Speedtest Intelligence® | Q1 2025–Q1 2026

Two contrasting patterns are, however, worth surfacing. The first is year-on-year improvement. Romanian median mobile download speeds rose 12% from 69.79 Mbps in Q1 2025 to 78.43 Mbps in Q1 2026, with 5G median speeds rising 9% over the same period from 132.91 Mbps to 144.55 Mbps. These improvements track the operator-level effects of consolidation, where Vodafone absorbed spectrum and density, and DIGI extended its coverage layer.

The second notable trend is observable in floor performance. Romania’s 10th percentile 5G download speed of 28.71 Mbps ranks third in the cohort, behind only Serbia and Bulgaria. In effect, this means that when users connect to 5G, the experience is competitive. The weakness is what happens between 5G sessions, where users still spend a large share of time on 4G layers that lack the dense mid-band overlay seen in CEE leaders like Bulgaria.

Spectrum access continues to trail regional peers

Romania’s total assigned mobile spectrum below 6 GHz amounts to 964 MHz, near the bottom of the CEE cohort. The structural gaps uniquely span both the coverage layer and the mid-band overlay. Sub-1 GHz holdings combined across 700, 800, and 900 MHz come to 160 MHz, second-last in the cohort and only ahead of Serbia.

The country’s 700 MHz allocation (ideal for broad 5G coverage), in particular, is uniquely thin. Romania assigned only 30 MHz at 700 MHz in the 2022 multi-band auction that closed on 15 November 2022, vs. the 60 MHz typical of CEE peers. The reason is documented in ANCOM’s pre-auction notice. Pre-consolidation Telekom Romania Mobile did not submit an application. Only Orange, RCS&RDS (DIGI), and Vodafone bid, and one of the three paired 2×10 MHz blocks went unsold.

C-band mid-band depth is similarly constrained. Romania’s total of 310 MHz across 3.4 to 3.8 GHz is the lowest in the CEE-8 cohort below 3.7 GHz. Czechia, Poland, Greece, Hungary, Serbia, and Slovakia all hold between 390 and 480 MHz at 3500 MHz. Orange Romania holds 160 MHz, Vodafone Romania 100 MHz, and DIGI 50 MHz of that 310 MHz total (exposing huge asymmetries among operators too). The 2022 auction itself raised €432.6 million (US$489 million) against an ANCOM-expected €692 million at reserve prices, a 37% shortfall that signalled operator caution about locking in long-duration spectrum at the offered prices given Romania’s comparatively weak monetization base (low ARPU) and potential pre-consolidation uncertainty.

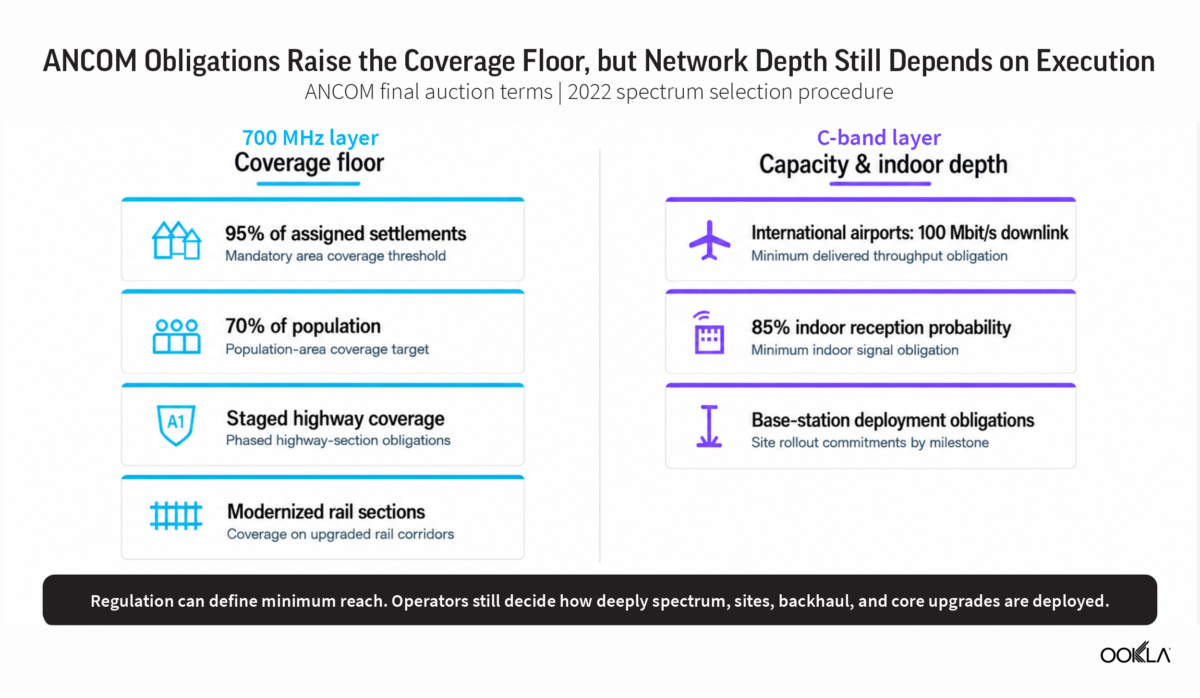

Coverage obligations require winners to cover at least 70% of the national population, all main highways, modernized railways, international airports, and 240 specifically named under-served settlements, with milestone deadlines through 2030. To that end, overall 5G Availability in Romania reached 39% in Q1 2026 in our data (up four percentage points year on year), below the CEE average but notably ahead of or comparable with mid-band centric 5G performance leaders Bulgaria (36%) and Hungary (41%).

The spectrum consolidation effects of the recent restructures in the market are likely to materially improve DIGI’s ability to compete on 5G coverage and Vodafone’s to compete on capacity. The October 2025 ANCOM license modifications reshaped DIGI’s spectrum portfolio. DIGI gained 2×5 MHz at 900 MHz, 2×15 MHz at 1800 MHz, 2×10 MHz at 2100 MHz, and 2×10 MHz FDD at 2600 MHz from the carve-out, expanding its sub-1 GHz position from 20 MHz to 30 MHz and adding 1800 MHz capacity it did not previously hold. Vodafone, meanwhile, consolidated the residual Telekom holdings, ending Q1 2026 as the operator with the deepest combined sub-1 GHz and 1800 MHz portfolio.

Low ARPU constrains ability to invest in Romania

Romania’s mobile market generates less revenue per connection than any other among the eight-country CEE cohort we examined, reflecting a legacy of fierce price-based competition. GSMA Intelligence reports ARPU per mobile connection at €6.45 (US$7.51) for Q1 2026. The next-lowest is Poland, which sits at €8.65 (US$10.08) per subscriber. Hungary leads at €13.84 (US$16.12), more than twice Romania’s level.

While capital intensity (share of revenues reinvested) appears healthy in relative terms at 18% of mobile revenue in GSMA data, above the CEE median and ahead of Czechia (11%) and Poland (10%), this masks the absolute revenue available to reinvest in the first instance. With per-connection ARPU under €7 (US$8.15), the capex envelope per population point is materially smaller than in CEE peers.

The country’s striking fixed-mobile divergence amplifies this picture. Romania ranks among EU (and global) leaders on fixed broadband, with one of the largest shares of high-speed household connections and third in the EU for gigabit connections based on the European Commission’s DESI data.

DIGI alone covers close to 100% of urban households with FTTH and holds about 70% of fixed connections. Orange reports more than 26,000 km of national fiber backbone and around 85,000 km of metro fiber, with 412,000 FTTH connections modernized during 2025.

In other words, fixed outcomes are excellent, but Romania’s mobile networks are held back by a combination of unfavorable factors coming together. These include the unusually compressed ARPU base noted here, the thin coverage-layer spectrum portfolio mentioned earlier, and a market structure that until October 2025 included a sub-scale fourth operator (Telekom) that could not absorb the investment required to keep pace.

Orange leads on network breadth and overall performance

Orange starts from the broadest Romanian operator position on 5G reach, likely helped by the largest 700 MHz allocation among the three operators (20 MHz, against Vodafone’s 10 MHz and zero at DIGI). In Q1 2026, Orange recorded 5G Availability of 57% (compared to 36% on Vodafone and 25% on DIGI). Its strong overall spectrum position also conferred an advantage in median download performance, leading with 97.70 Mbps across all technologies (as much as 39% and 45% higher than Vodafone and DIGI respectively).

These results are consistent with the operator’s public strategy. Orange Romania said in its 2025 results that 5G and 5G+ services were available in 88 cities, with consolidated turnover reaching €1.46 billion (US$ 1.7 billion), up 3%. Last year, it launched what it described as the country’s first public 5G standalone deployment in the Danube Delta, supported by a 5G core in Bucharest and a local edge node (an EU Connecting Europe Facility project covering 14 of 23 target localities).

Orange Leads on 5G Reach, DIGI Leads 4G Coverage

Speedtest Intelligence® | Q1 2026

The company said its 2026 investment budget would exceed €200 million (US$ 234 million). Its enviable spectrum position (including in mid-band depth and with a 1500 MHz supplemental downlink advantage) and its early 3G sunset therefore gives it several levers to use that capital to continue to compete. However, the caveat is latency and quality of experience, which is not simply shaped by spectrum alone but also other factors related to peering and interconnection.

Orange ranked behind DIGI but ahead of Vodafone on several responsiveness-related metrics, including on median multi-server latency, web page load times and latency to cloud infrastructure endpoints, with DIGI pulling further ahead on 5G.

Vodafone combines high 5G speeds with integration pressure

Vodafone Romania led on median 5G download speed at 180.57 Mbps, double its Q1 2025 result of 90.57 Mbps and surpassing Orange for the first time to become market leader. The doubling is consistent with absorbing Telekom Romania’s spectrum across 800, 900, 1800, 2100, and 2600 MHz, and with the operator’s various integration commitments.

Vodafone signed a six-year 5G RAN partnership with Ericsson on 12 February 2024 covering 5G RAN, Standalone transition, and Massive MIMO. A week later, Vodafone launched commercial Open RAN across 20 Romanian cities with Samsung vRAN, Wind River, and Dell PowerEdge, one of the larger commercial Open RAN footprints in Europe (supporting a more flexible vendor and radio strategy over time in theory, but also potentially introducing additional complexity). CEO Nedim Baytorun has committed €150 million (US$ 170 million) in incremental network investment tied to the integration.

Despite the newfound lead on 5G speed post-consolidation, the operator continues to lag its peers on overall QoE outcomes (although comparable with or ahead of Orange on a small number of measures), suggesting less mature or optimized peering, routing or interconnection depth in Romania to the most popular content and cloud infrastructure. In Q1 2026, for example, median web page load times on Vodafone’s network were as much as 7% slower than on peers.

DIGI’s challenger model and fiber depth produces favorable latency signals

DIGI’s Q1 2026 results reveal a different network thesis, aligning with its smaller mobile scale and narrower spectrum position. While it continues to trail peers on median 5G download speeds (principally due to more limited mid-band assets), it leads on 5G Consistency (the share of Speedtest samples with minimum performance of at least 25 Mbps down and 3 Mbps up) and 10th percentile 5G speeds, suggesting users on its network are less likely to end up with very weak tail outcomes on 5G.

Despite featuring a smaller 5G footprint (held back by the lack of 700 MHz), DIGI led on 4G Availability in Q1 2026 (with ~98% compared to a close ~96% on Orange and ~94% on Vodafone), and exhibited the lowest share of users spending most of their time stuck on legacy 2G networks (a likely merit of its broader 4G coverage layer observed in our data).

It is notable that the operator has pursued an aggressive spectrum refarming strategy, likely stimulated by its leaner portfolio requiring prudent management, being the first to sunset 3G and reuse its 2100 MHz (2×15 MHz) spectrum fully for 4G and 5G. On 5G coverage, DIGI is targeting a ramp from 30% population coverage at the end of last year to 70% by end-2028 and 99.8% by end-2030, underpinned by about 4,500 mobile sites.

The most interesting part of DIGI’s performance profile, however, is latency and QoE. DIGI recorded the lowest Romanian operator median multi-server latency (as much as 10% lower than peers) across all technologies and on 5G. In real-world testing of popular hyperscaler and website infrastructure endpoints, it also recorded the lowest cloud latency (as much as 14% faster) and shortest web page load times on 5G.

The QoE results suggest a relatively better experience for consumers in applications requiring responsiveness like video calling and gaming on DIGI’s network. That does not mean DIGI has the largest radio capacity position overall (evidenced by lower median and 90th percentile speeds), and highlights how application experience depends on more than download speed.

DIGI’s deep fixed network assets, backhaul economics, routing, and traffic management may be helping parts of the application experience even where its 5G download speed trails Orange and Vodafone.

Romania’s weaker mobile performance does not appear to be explained by a lack of local internet exchange, peering or content delivery infrastructure. Within Romania, Bucharest has a competitive peering and CDN ecosystem that, in theory, should not be a major bottleneck for operators.

The InterLAN internet exchange operates 125 peers across 5.4 Tbps of capacity, while RoNIX adds another 1.4 Tbps. Major content and cloud providers, including Google, Cloudflare, Meta, Microsoft, Akamai and Netflix, are also present in Bucharest. This points to operator-level differences in radio access, transport, core architecture, peering policy or traffic management as more likely drivers of QoE variation.

Coverage obligations set the baseline, but operator investment will determine performance

The next 12 to 18 months will test how far the new market structure can move performance in Romania. The Vodafone-Telekom legal merger is scheduled to complete after 1 July 2026, at which point the combined mid-band network should continue to extend the year-on-year 5G gains already visible in Q1 2026.

The timing of the first 5G SA launch and deployment at scale is the larger unknown. Orange’s Danube Delta cluster and Vodafone’s Politehnica private network are proofs of concept, not commercial services, and no Romanian operator has yet commercialized features like Voice over New Radio (VoNR), network slicing, or similar at national scale. Vodafone Group’s five-year programmable networks partnership with Ericsson, signed in October 2025 and naming Romania as a primary market, is the most concrete commitment to closing that gap.

Policy will set the floor moving forward, since ANCOM’s 2022 auction conditions tied spectrum rights to public coverage outcomes. Established 700 MHz winners must cover 95% of assigned under-served settlements, reach areas inhabited by 70% of the population, and meet staged transport-corridor milestones across highways and modernized rail. C-band winners, meanwhile, carry obligations at international airports, including at least 100 Mbps downlink and an 85% indoor reception probability, alongside base-station deployment targets.

Backed by ANCOM’s signal and service verification methodology, those terms should keep 5G from concentrating only in the most commercially attractive urban cores. DIGI’s aforementioned commitment to 99.8% population coverage by end-2030, on a base of about 4,500 antennas, runs in the same direction, reinforced by the road-coverage obligations the Competition Council attached to its Telekom Romania spectrum carve-out.

Economics will continue to shape how far operators go beyond minimum rollout obligations. Romania has some public support for connectivity, but not a broad national subsidy for mobile RAN expansion. The European Commission’s Romania connectivity profile cites €94 million of Recovery and Resilience Plan support for white and grey areas, plus CEF Digital funding for targeted projects such as 5G Connect Danube Delta.

In practice, the main performance lift will still come from operator capital allocation, spectrum deployment, site access, and core (i.e. with 5G SA) evolution. The open question for regulators is whether consolidation actually delivers the investment lift Vodafone’s commentary suggests, or whether the ARPU compression behind its €4.5 billion (US$5.09 billion) impairment continues to bite.