By Ana Milosavljević*, Serbia

Foreign investment shaped Serbia’s automotive industry. Now its risks are becoming visible

Often seen as the crown jewel of Serbian manufacturing, the country’s automotive industry has recently begun to wobble. Despite billions of euros in exports and major foreign investment, job cuts and factory closures since 2025 have raised concerns about the sector’s sustainability. “Germany cannot lay off 70,000 workers and everything here remain completely fine,” Serbian President Aleksandar Vučić commented, acknowledging a structural dependency that, according to critics, has left Serbian workers bearing the consequences of decisions made elsewhere. As foreign investors in this export-oriented sector begin to pull back, the fragility of Serbia’s automotive boom is becoming increasingly apparent.

The Serbian government has positioned the country as a key node in the global supply chain for multinational automotive companies, particularly from the EU and, increasingly, from China. Through a broad range of government incentives, the state has succeeded in attracting investments worth billions of euros.

Foreign companies are offered free-trade zones, tax incentives, discounted or free construction land, state-funded infrastructure, training subsidies and more. More than 50 foreign companies have benefited from such programmes, including Michelin, Bosch, Aptiv, Continental and Lear.

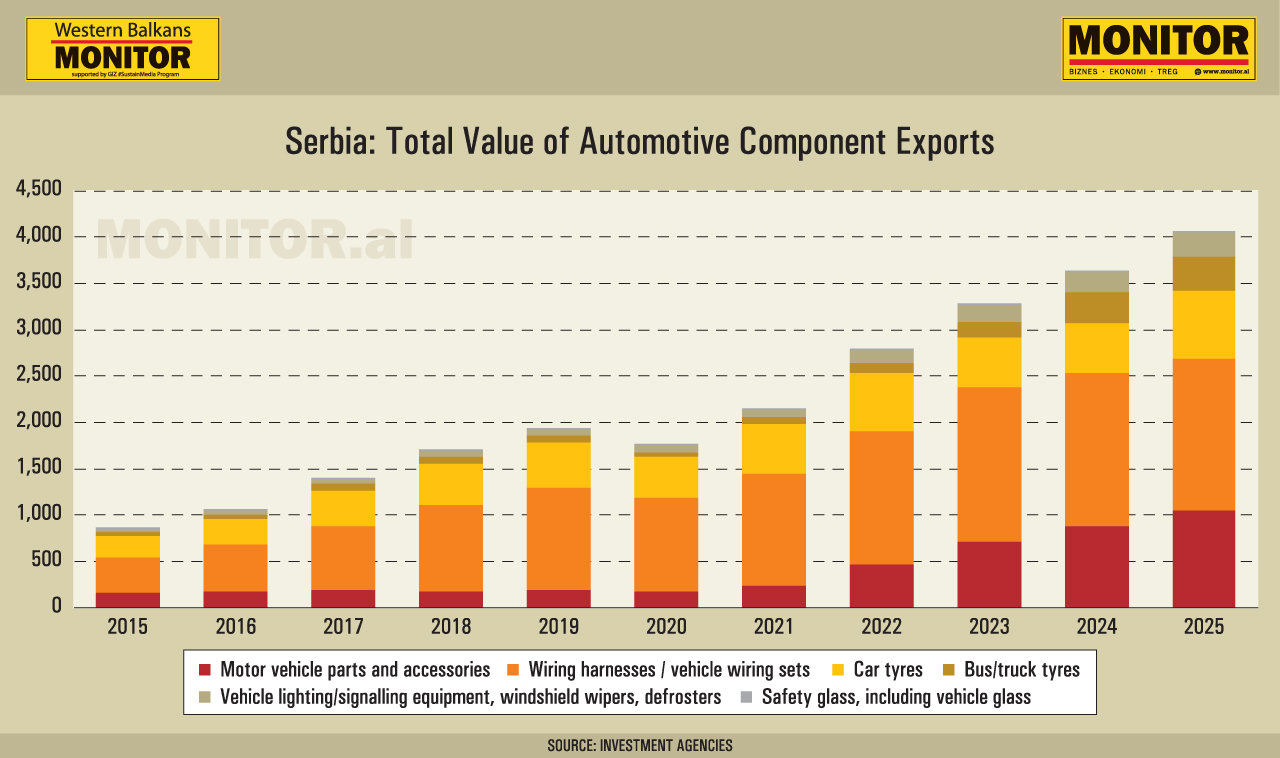

As a result, Serbia’s automotive exports exceeded €4 billion in 2025, accounting for 12.3% of total exports. Around 140 suppliers generated €8.8 billion in revenue in 2024, equivalent to 3% of Serbia’s GDP. However, this growth has been concentrated in labour-intensive automotive parts manufacturing, as foreign-owned companies were drawn to Serbia by low labour costs, generous state incentives and access to European markets.

Dr Dmitry Pozhidaev, member of the Scientific Association of Economists of Serbia and consultant to the United Nations Capital Development Fund, describes Serbia’s automotive industry as a sector in which “foreign-owned companies import the technology, machinery, designs, key components and often management systems, while Serbia mainly provides labour, industrial zones, infrastructure, subsidies and logistical access to European markets.”

Serbia’s automotive exports, including wiring systems, tyres, windscreen wipers, seat covers and other metal and plastic components, are directed mainly to Germany, Hungary and the Czech Republic. As demand weakened in these markets, the consequences began to emerge in Serbian factories during 2025 and have continued into 2026.

Around 16,000 jobs have been lost over the past year in Serbia’s manufacturing sector, which employs 475,000 workers. The automotive industry was no exception. In 2025, German automotive cable manufacturers Dräxlmaier and Leoni closed factories that together employed approximately 4,000 workers, while other plants placed employees on paid leave due to declining demand.

“All of this is the consequence of a decades-long strategy of attracting Foreign Direct Investment, which brought simple jobs in cable manufacturing, moulded components and tyres. Since the investments attracted were factories located at the lower end of the supply chains of major manufacturers and multinational corporations, any uncertainty affecting the ‘big players’ is inevitably accompanied by uncertainty here as well,” said Vladimir Simović, coordinator of the workers’ rights programme at the Centre for Emancipation Policies.

At the beginning of May, President Vučić blamed workers’ excessive use of sick leave as one reason foreign investors were leaving. However, according to labour-rights organisations, the current crisis has merely made existing exploitation within the sector more visible.

A 2024 study published by the Centre for Emancipation Policies found that automotive workers in Serbia have long faced harsh working conditions, some of which have even resulted in worker deaths. According to the study, 60-hour work weeks are not uncommon, while workers who take sick leave are often penalised. The study found that the average worker in the sector earned around €600 per month, including bonuses, overtime and night-shift work. “A prison camp would be better than this,” one interviewed worker said.

A notable example is Yura, the South Korean-owned automotive supplier whose Serbian workers went on strike in 2024 over what unions described as inhumane working conditions, punitive bonus policies, anti-union pressure and violations of the right to strike. Yura manufactures vehicle wiring systems used by the German company Mercedes-Benz, which conducted a Responsible Supply Chain Initiative audit in early 2025 following whistleblower reports concerning labour conditions. In January 2026, Mercedes-Benz marked the audit as “resolved”, while the Serbian Metal Workers’ Union insisted that conditions at Yura remained unchanged.

In 2026, Yura also laid off part of its workforce in Serbia and placed others on paid leave. Yet official production figures paint a more complicated picture of a sector in decline. In March 2026, Serbia’s industrial production increased by 6.4% year-on-year, while manufacturing output rose by 8.4%, with motor vehicle and trailer production among the main contributors to growth.

“These are not mutually exclusive trends,” said Dr Pozhidaev.

According to him, Serbia’s automotive sector is not moving uniformly. While component suppliers are cutting production and closing factories, final assembly at the Stellantis plant in Kragujevac is expanding. In 2025, Stellantis announced it would begin production of the petrol-powered Fiat Grande Panda. Around 800 workers in Kragujevac are now operating across three shifts, while reports suggest the plant is close to maximum capacity.

“Production can increase in certain segments without guaranteeing sustainable employment across the entire sector. From a trade union perspective, the primary concern is not overall production but the vulnerability of workers in export-oriented supplier firms exposed to external demand, European restructuring and decisions made by multinational corporations,” Dr Pozhidaev explained.

The crisis in Europe’s automotive industry is also creating new opportunities for Chinese investors. The Netherlands-based Stellantis Group is reportedly considering selling or sharing some of its European plants with Chinese partners.

China’s growing presence in Serbia’s automotive industry is already visible. In 2025, the Netherlands recorded the largest inflow of Foreign Direct Investment into Serbia, but China has been the fastest-growing foreign investor in the country over the past decade. However, like its EU competitors, Chinese investment has also been accompanied by allegations of labour and human-rights violations.

Since 2015, China has invested around €7 billion in Serbia. Chinese automotive companies such as Shandong Jindi, Ningbo Zhenyu and Shanghai Huizhong are investing in or planning to open automotive factories. One of the first major Chinese investments in the country was the Linglong tyre factory, the first Chinese tyre plant in Europe.

Announced in 2018 and designated by the Serbian government as an investment of national importance, the factory covers 97 hectares, represents nearly €1 billion in investment and is designed to produce 14 million tyres annually at full capacity. Many of its approximately 2,400 employees are migrant workers, some of whom have accused the company of human trafficking and forced labour. In 2025, as part of broader US efforts to limit China’s role in strategic supply chains, the United States banned imports of Linglong tyres.

While China’s growing presence in Serbia’s automotive sector may create new jobs and potentially more advanced production, Dr Pozhidaev warns that it will not alter the industry’s underlying external dependency.

“The entry of Chinese companies into the automotive market does not fundamentally change the industry model. The key issue is not whether investors come from Germany or China, but whether Serbia continues to occupy a position within global value chains where decisions regarding production, technological upgrading and employment sustainability are determined externally,” argues Dr Pozhidaev.

The current economic crisis represents a crossroads for Serbia, as the public increasingly questions the sustainability of an economy built around attracting foreign investment. With no visible end to job cuts, the crown jewel of Serbian manufacturing still shines in production and export statistics, but from the factory floor it appears far less secure. China’s rise in the sector may change the origin of investment, but not the model itself. Regardless of where the capital comes from, Serbia’s automotive industry remains defined by worker insecurity and dependence on decisions made elsewhere.

How the Western Balkans became Europe’s “factory”… what comes next?

*Ana Milosavljević is a Belgrade-based freelance journalist reporting on economic policy, labor issues, and regional politics in the Western Balkans

Ky është artikull ekskluziv i Revistës Monitor, që gëzon të drejtën e autorësisë sipas Ligjit Nr. 35/2016, “Për të drejtat e autorit dhe të drejtat e lidhura me to”.

Artikulli mund të ripublikohet nga mediat e tjera vetëm duke cituar “Revista Monitor” shoqëruar me linkun e artikullit origjinal.