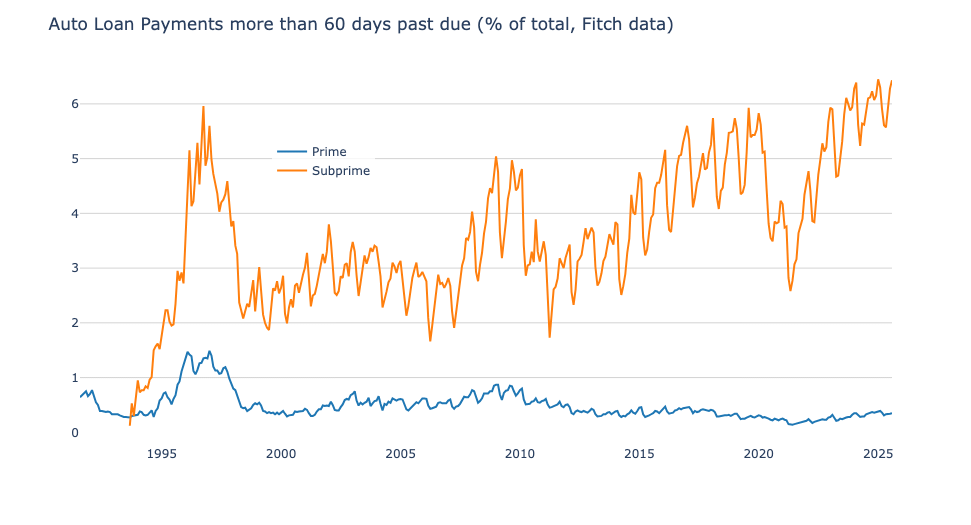

Interesting how prime loans are still at (fairly) low levels. To me this stands out as an illustration of the (US) inequality issue. Lower income households are feeling the crunch far more than upper income households.

KrisPBacon26 on

Isn’t this what they saw with subprime housing a year or two before the crash? Or do I have that wrong? I thought one of the warning signs was the large amount of homeowners not being able to keep up with their mortgages that they couldn’t afford in the first place? Not saying I think that’s happening, just genuinely curious.

Boring_Philosophy160 on

Would be cool to see another piece of data: mean loan payment in current/constant dollars.

unique_usemame on

Nice chart.

My instinctive read of the chart prior to 2020 and knowing the economic history is that there were a couple of spikes caused by issues in the economy. However there was also a general rise 2013-2019 that I didn’t think correlated to an issue in the economy… And what we see today is likely a continuation of that trend.

So what is that trend? Is that the growth in companies that make money by financing those with poor credit for cars that they repo every few months? Is this sparked by companies figuring out that this is profitable?

dterwiel on

why is the data periodic? there is a yearly high-default season with two peaks a year. Does it have anything to do with taxation frequency in the US or something? Or do the dips cooincide with common bonusses or alloance?

Melodic-Resource4392 on

Could this indicate a higher default opportunity leading to a potential surplus of houses on the market meaning possible lower house prices?

mdandy68 on

because incomes have lagged for decades. and once you’re poor it costs you more on every level to even make basic requirements.

You make less $ so you have less cushion.

Your job is probably lower tier work, you’re more likely to be fired or replaced.

You have to have reliable transport, but all truly reliable transport is out of reach or costs some crazy amount. They will only loan you so much, but at a shit rate.

auto companies and dealerships have started to really focus on bundling these debts and selling them. They have to sell cars and move loans and so they search out buyers, not really caring how realistic it is, or if the loan will be paid at all, because in a few months they won’t own the loan any longer.

Many similarities to the 2008 crash and bubble. Shady paperwork and inflated costs and really poor risk loans being spread out. You think a stripped out house with a bad roof is shitty collateral? Think about these automobiles. Scrap metal

AG3NTjoseph on

Add a line for the inflation-adjusted average car price. It just hit $50,000 in the US, and that’s straight up crazy.

RealMcGonzo on

Thank you for including plenty of history! So many of these charts on Reddit are like “Doh! This indicator hit a 2 year high! We’re going to crash!”

sarcasticorange on

Worth noting that subprime make up around 15% of loans.

janitorial-duties on

I worked in suprime auto loans. I beg of everyone to buy a used clunker until you can get your credit back up and have at least 20% cash down.

Otherwise you are paying your car TWICE over because of interest.

SortOfKnow on

So 1k a month car notes aren’t sustainable…wow

Capital_Coconut_2374 on

20% of new vehicles this year had a payment north of a thousand bucks a month

weas71 on

Are auto loans mostly from dealerships? Trying to find the angle here to make money off this and nothing is coming.

AWill33 on

Forgive my ignorance… What technically constitutes an auto loan as subprime?

ahipikr on

What is the y-axis scale? 1%, 2%, etc.?

AWill33 on

Interesting just from my own experience in finance. Lower wage/credit tend to be more “invested” in the car they drive. As a point of pride. Higher wage earners tend to see it as just another expense. Also why you tend to see higher net worth individuals buying collector cars even if they aren’t car people. They view it as an investment or at least an asset that’s full depreciated and/or possibly more likely to gain value.

5minArgument on

The answer to how one goes into poverty:

-very slowly at first, then all of a sudden-

Highschooleducation on

Would love to see the rates and profits even with this many behind, I’ll bet it’s outrageous. Preying on poor people, do payday loans next.

20 Comments

Source: Fitch, Tools: Python and Plotly

Interesting how prime loans are still at (fairly) low levels. To me this stands out as an illustration of the (US) inequality issue. Lower income households are feeling the crunch far more than upper income households.

Isn’t this what they saw with subprime housing a year or two before the crash? Or do I have that wrong? I thought one of the warning signs was the large amount of homeowners not being able to keep up with their mortgages that they couldn’t afford in the first place? Not saying I think that’s happening, just genuinely curious.

Would be cool to see another piece of data: mean loan payment in current/constant dollars.

Nice chart.

My instinctive read of the chart prior to 2020 and knowing the economic history is that there were a couple of spikes caused by issues in the economy. However there was also a general rise 2013-2019 that I didn’t think correlated to an issue in the economy… And what we see today is likely a continuation of that trend.

So what is that trend? Is that the growth in companies that make money by financing those with poor credit for cars that they repo every few months? Is this sparked by companies figuring out that this is profitable?

why is the data periodic? there is a yearly high-default season with two peaks a year. Does it have anything to do with taxation frequency in the US or something? Or do the dips cooincide with common bonusses or alloance?

Could this indicate a higher default opportunity leading to a potential surplus of houses on the market meaning possible lower house prices?

because incomes have lagged for decades. and once you’re poor it costs you more on every level to even make basic requirements.

You make less $ so you have less cushion.

Your job is probably lower tier work, you’re more likely to be fired or replaced.

You have to have reliable transport, but all truly reliable transport is out of reach or costs some crazy amount. They will only loan you so much, but at a shit rate.

auto companies and dealerships have started to really focus on bundling these debts and selling them. They have to sell cars and move loans and so they search out buyers, not really caring how realistic it is, or if the loan will be paid at all, because in a few months they won’t own the loan any longer.

Many similarities to the 2008 crash and bubble. Shady paperwork and inflated costs and really poor risk loans being spread out. You think a stripped out house with a bad roof is shitty collateral? Think about these automobiles. Scrap metal

Add a line for the inflation-adjusted average car price. It just hit $50,000 in the US, and that’s straight up crazy.

Thank you for including plenty of history! So many of these charts on Reddit are like “Doh! This indicator hit a 2 year high! We’re going to crash!”

Worth noting that subprime make up around 15% of loans.

I worked in suprime auto loans. I beg of everyone to buy a used clunker until you can get your credit back up and have at least 20% cash down.

Otherwise you are paying your car TWICE over because of interest.

So 1k a month car notes aren’t sustainable…wow

20% of new vehicles this year had a payment north of a thousand bucks a month

Are auto loans mostly from dealerships? Trying to find the angle here to make money off this and nothing is coming.

Forgive my ignorance… What technically constitutes an auto loan as subprime?

What is the y-axis scale? 1%, 2%, etc.?

Interesting just from my own experience in finance. Lower wage/credit tend to be more “invested” in the car they drive. As a point of pride. Higher wage earners tend to see it as just another expense. Also why you tend to see higher net worth individuals buying collector cars even if they aren’t car people. They view it as an investment or at least an asset that’s full depreciated and/or possibly more likely to gain value.

The answer to how one goes into poverty:

-very slowly at first, then all of a sudden-

Would love to see the rates and profits even with this many behind, I’ll bet it’s outrageous. Preying on poor people, do payday loans next.