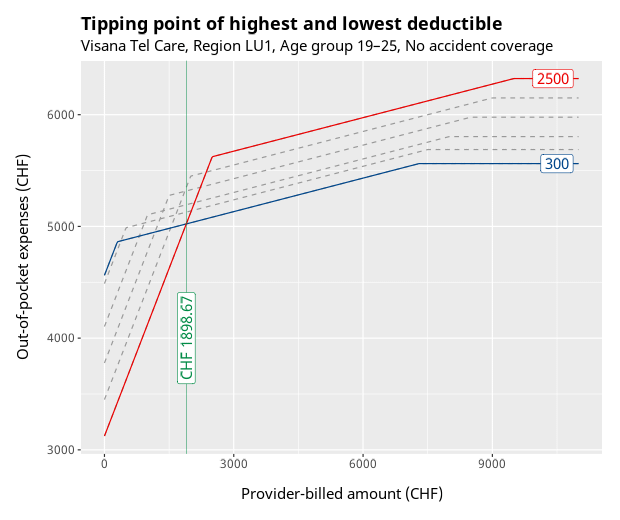

The specific insurance shown is just used as an example

Source: https://hertig.blog/posts/why-most-health-insurance-deductibles-make-no-sense/

https://i.redd.it/071kj9f29u0g1.png

Posted by CatsInYourArea

The specific insurance shown is just used as an example

Source: https://hertig.blog/posts/why-most-health-insurance-deductibles-make-no-sense/

https://i.redd.it/071kj9f29u0g1.png

Posted by CatsInYourArea

15 Comments

I did the calculations myself a couple of weeks ago and switched from 2500 to 300 for next year. Franchise levels in-between didn’t show any cost savings. It really was either-or for me.

I made the calculation and it actually is 114 x 12 + 300 =1’668 for me

114 is the monthly difference.

If you’re not sure, the 2500 savings potential is a lot higher than the 300 potential. So the worst-case scenario with 2500 isn’t that bad. You can see that in the chart.

Similar break even point with Concordia at around 1900.- (has crept up a bit over the years actually)

The article mentions this at the bottom: the government’s insurance comparer also has its [own calculator](https://www.priminfo.admin.ch/de/sparen/franchisenrechner?location_id=60033080653296&yob%5B0%5D=2000&insurer=1555&plan=TCA&coverage%5B0%5D=0&display=franchise-calc).

(I had to disable the browser ad & tracker blocking to get this page to load).

> if you expect your healthcare bills to be below CHF 2’000

I did expect that last year as I am seldom ill. Then on holiday in Switzerland I had to go for gal stone removal. CHF 1700 later and I was a bit screwed financially. I had to make payment arrangements.

This year I lowered my franchise to CHF 500 si I am not screwed by a single event.

To complement OP’s post, use this very useful tool by the consumer magazine Bon à Savoir. Allows to make the right decision.

[https://www.bonasavoir.ch/services/outils-calculateurs/assurances/la-meilleure-franchise-pour-lassurance-maladie](https://www.bonasavoir.ch/services/outils-calculateurs/assurances/la-meilleure-franchise-pour-lassurance-maladie)

My healthcare bills are usually between 15.- CHF and 280.- CHF.

So I should choose franchise 300?

Yes this is well known. Any franchise except 300 or 2500 is a scam. What I don’t understand is the why the in between premiums are allowed to be sold. Since the are mathematically provable to always be a worse deal.

Dis you just rounded 1900 to 2000?

The whole thing just sucks. It needs reforming.

Yaaaay I always wanted to gamble on my health

I concur that this is what it does indeed look like (having spent time doing it in excel to check)

2500, you reach that so quickly if you just have one minor issue. It’s all so expensive in Switzerland, simple 15min visit 200+, visit specialist 300/400, a test 500+, a scan close to a 1000, etc.

While I agree, I would still encourage people to do the math. For example swisscare (so international student insurance) is actually cheaper on the 500chf franchise simply because the monthly difference between the 300chf and 500chf franchise is more than 20chf per month