Source with navigable data: https://www.ambrosetti.eu/community-cashless-society/indici-cashless/

Article from the sun (I paste everything because it is behind a paywall): https://www.ilsole24ore.com/art/cashless-index-italia-21-posto-nell-ue-181-transazioni-digitali-pro-capite-AI2UhrqB

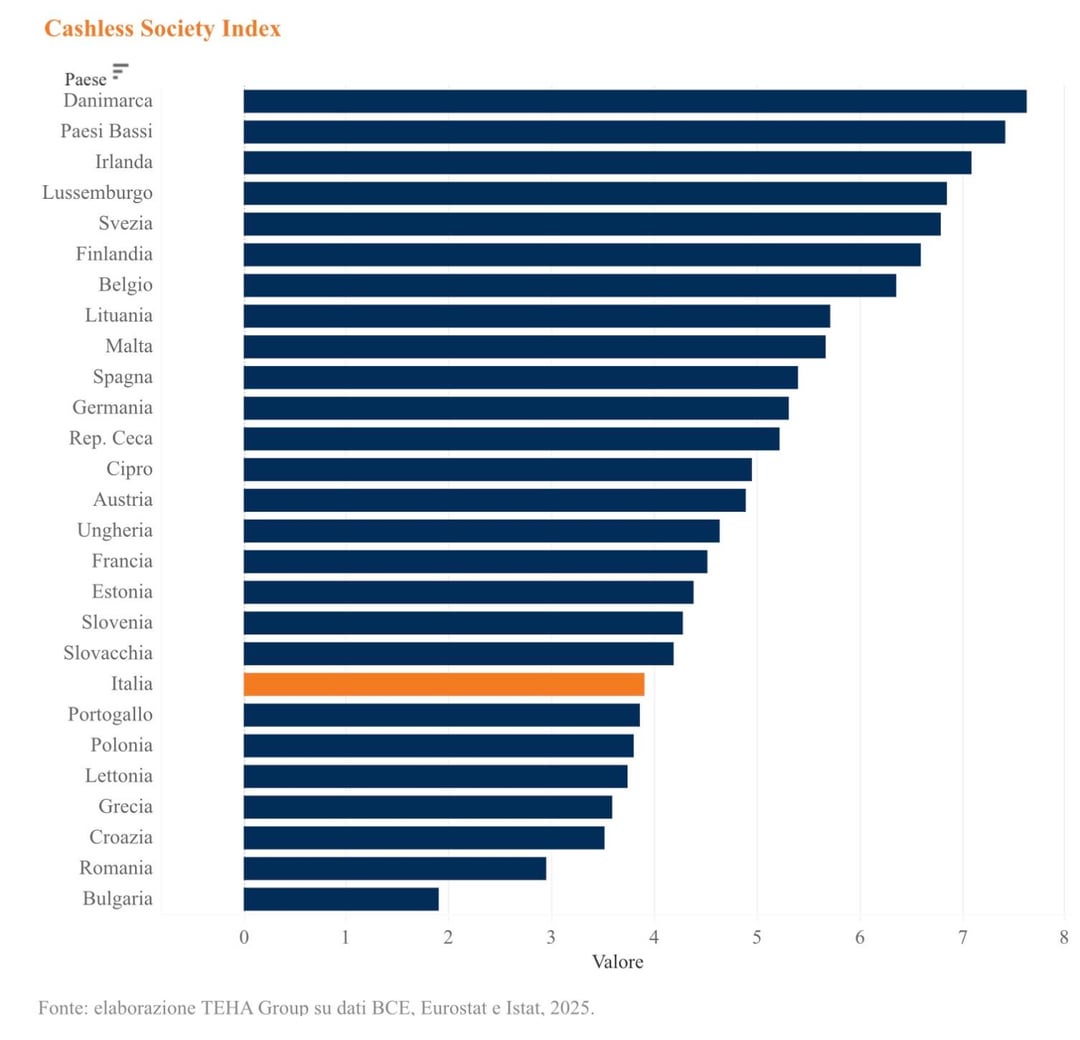

Despite transactions that will exceed 500 billion euros this year, Italy is still below the European average: it is 21st in the Cashless Society Index 2026 and 31st in the world for Cash Intensity, with a use of cash still higher than the European average. This is the ranking that emerges from the 2026 report of the Community Cashless Society by Teha Group.

In 2025, cashless transactions in Italy tripled their value compared to 2015 and stood at 26.6% of GDP, a result that consolidates the growth of digital payments in the country and confirms its role as an enabling economic infrastructure. However, the expansion of cashless, supported by an average annual growth rate of +9.5% in the last three years, is part of a framework that still shows significant room for growth: Italy is in 21st place in the Cashless Society Index 2026, with 181.4 transactions per capita, well below the average of the EU of 27 countries, equal to 246.8 transactions per capita.

The international report

The 11th report of Teha Group’s Community Cashless Society also conducted a survey on citizens, merchants and companies to analyze the main innovative trends in the world of cashless payments: the results will be presented during the Forum, which will be held on 26 March 2026 in Villa d’Este, Cernobbio. «Digital payments are now a stable component of the national economy and a strategic lever for competitiveness, legality and efficiency», declares Valerio De Molli, managing partner and CEO of The European House – Ambrosetti and Teha Group. «However – he adds – the distance from the main European countries remains significant: bridging this gap means strengthening Italy’s ability to attract investments, reduce the shadow economy and support more transparent, modern and inclusive growth».

At current growth rates, a further 27.5 billion euros could be activated by 2030, while in the case of alignment with the best European performers the overall potential could reach 123 billion euros. The cashless payments industrial chain today represents a structured and high-value sector for the national economic system: it has 2,844 companies with the integration of national and international operators, generates 17.7 billion euros in turnover and 9.4 billion in added value, with 34,600 employees distributed along the entire electronic transaction value chain. Over the last ten years, the sector has recorded a growth dynamic significantly higher than the average of the Italian economy: since 2015, turnover has increased by 85.3%, compared to a GDP growth of +32.2 percent.

The Index and the use of cash

Returning to the Cashless Society Index 2026, Italy (21st place in the EU-27) has lost one position compared to the previous year and remains distant from the main European benchmarks: Germany (10th), Spain (12th) and France (16th). The gap also emerges clearly in the main quantitative indicators. Cashless transactions represent 26.6% of GDP, remaining below the EU-27 average of 31.6%. If on the one hand the country has accelerated in the process of digitizing payments, on the other the comparison with Europe highlights how the recovery is still partial and insufficient to bridge a gap that appears to be of a structural nature. The dependence on cash fits into this context, which according to the Cash Intensity Index places Italy in 31st place out of 144 world economies for the incidence of cash in circulation on GDP (11.5%), a value higher than the European average (9.8%) and higher than the main geographical areas. The increased circulation of cash has a negative impact on the traceability of transactions and contributes to strengthening the dynamics of the underground economy, which for the third consecutive year has worsened (+7.5%), bringing the phenomenon back to levels higher than the pre-pandemic period.

https://www.reddit.com/gallery/1rp5140

Posted by sr_local

4 Comments

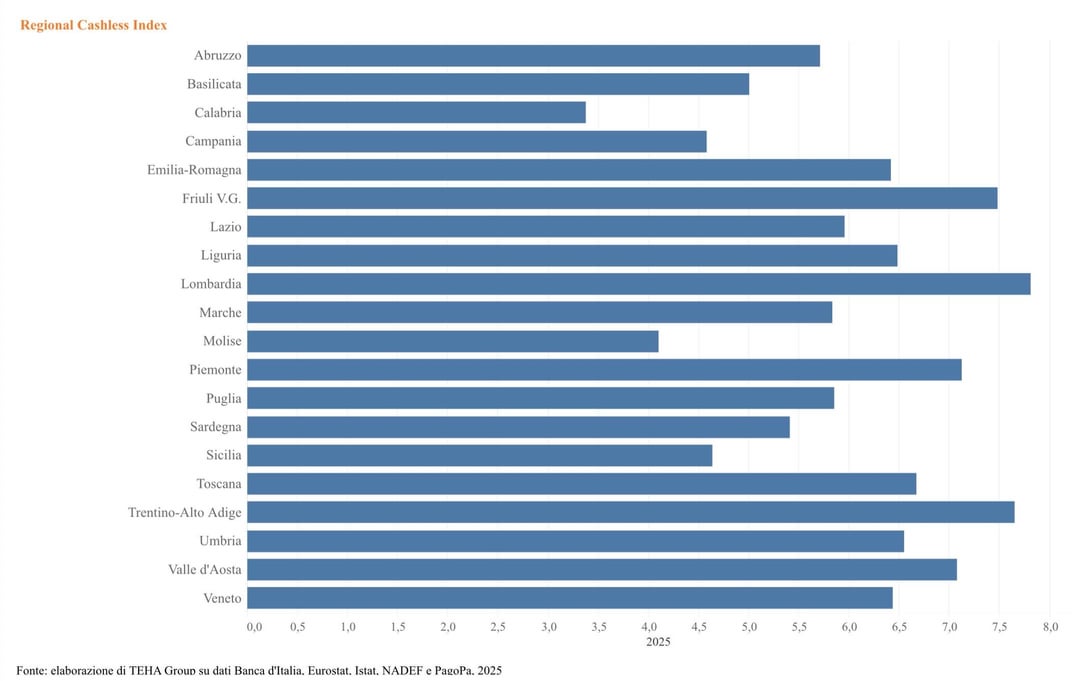

Non capisco come possa essere possibile che ci sia una sola regione con un punteggio inferiore a quello nazionale. La Lombardia ha un dato simile alla Danimarca e fa un sesto della popolazione italiana, com’è possibile che il dato nazionale sia sostanzialmente la metà?

Basito nel vedere l’Italia dietro la Germania onestamente

Semplice impressione personale. Io noto una differenza enorme tra i contesti dei grandi centri urbani (specialmente nelle zone centrali e semicentrali) e quelli di provincia. Da una parte il contante sta sparendo e dall’altra è ancora di largo utilizzo.

Io mi muovo molto per lavoro e noto che appena si esce fuori di città e si va in contesti provinciali la gente paga molto di più in contanti.

Parlo di semplici transazioni quotidiane, poi c’è un enorme sommerso di transazioni dove il pagamento avviene in contanti perché prestatore d’opera e cliente si accordano in tal senso..

Statistiche drogate dagli acquisti online.