![[OC] Consumers with mistakes on their credit report are getting less help from TransUnion and Experian under Trump’s Consumer Financial Protection Bureau](https://www.byteseu.com/wp-content/uploads/2026/03/bki688g0qkog1-1024x992.jpg "[OC] Consumers with mistakes on their credit report are getting less help from TransUnion and Experian under Trump’s Consumer Financial Protection Bureau")

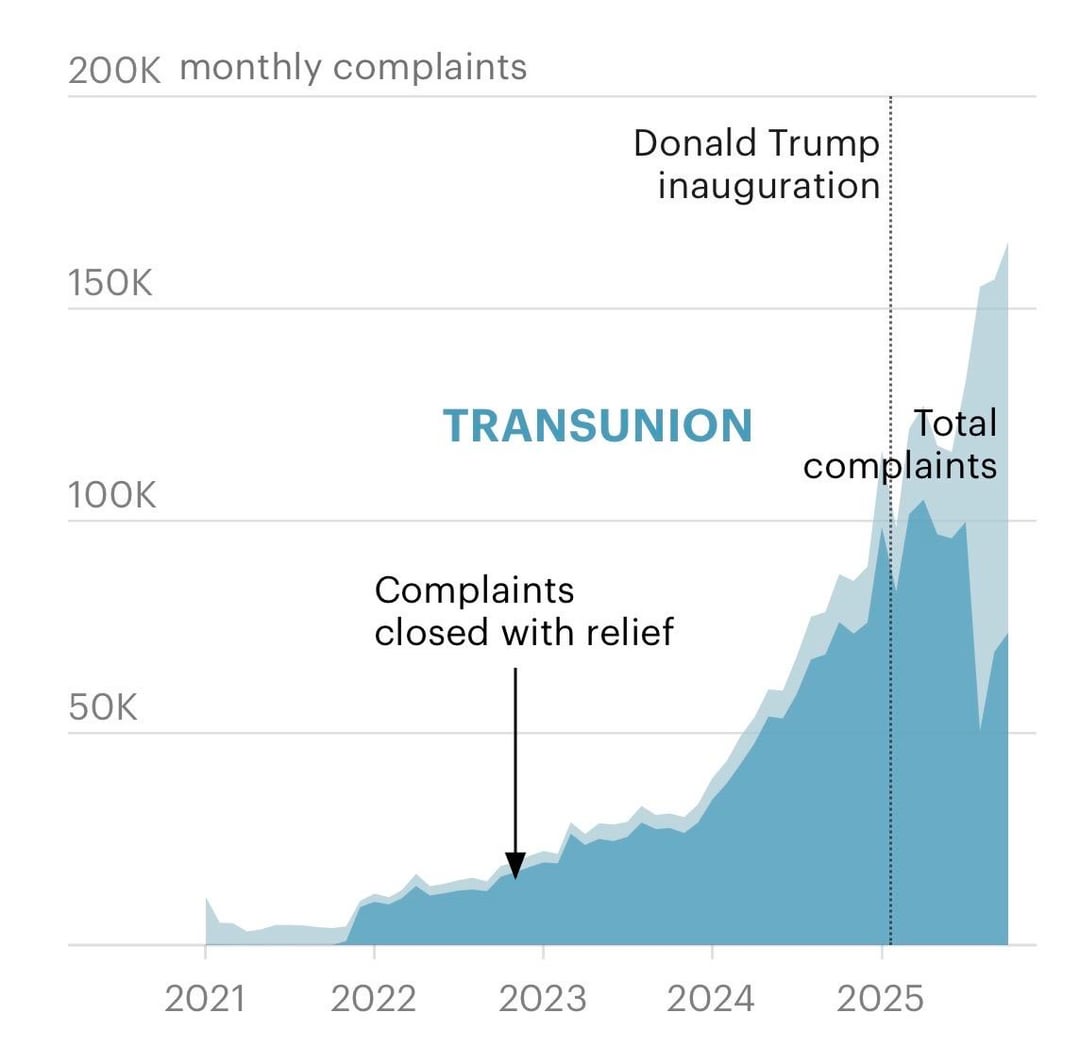

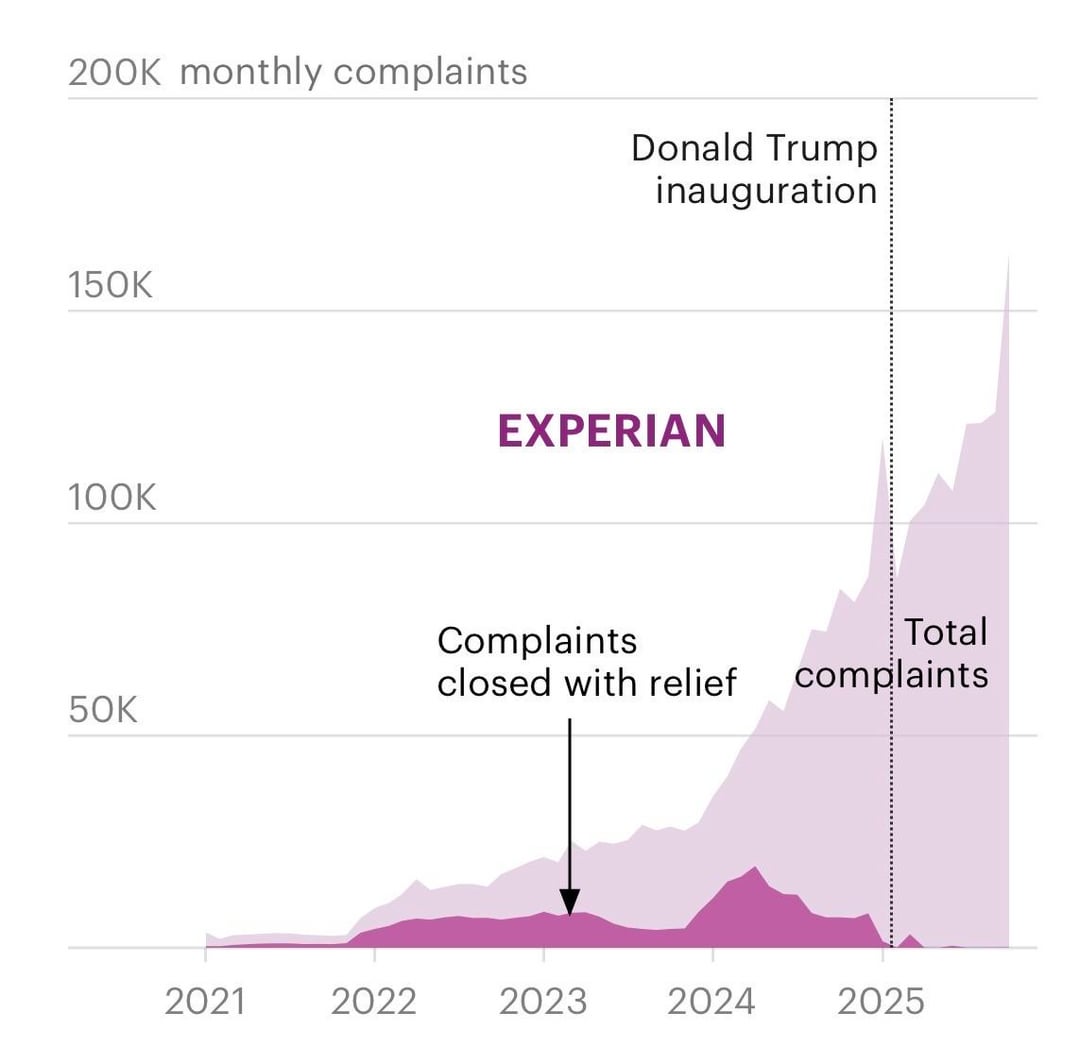

TransUnion and Experian have sharply reduced the share of consumer complaints they resolved in customers’ favor, according to our analysis of federal complaint data.

TransUnion’s relief rate, which had remained relatively steady for several years, began plunging in the summer of 2025. By October it was providing relief roughly half as often.

Experian’s drop was even more dramatic. The company resolved nearly 20% of complaints in consumers’ favor in 2024. Last year, that figure fell to less than 1%.

The timing of the drops at TransUnion and Experian coincides with the dismantling of the Consumer Financial Protection Bureau. Since Jan. 2025, a total of more than 2.7 million credit reporting complaints submitted to the CFPB have gone without relief, leaving some people at risk of being denied loans, housing or employment and subject to higher rates from insurers and lenders.

Here's our full investigation: https://www.propublica.org/article/credit-report-mistakes-cfpb-experian-transunion

Tool: Datawrapper. Source: Consumer Financial Protection Bureau.

—

*Chart note: Credit reporting agencies can close complaints in customers’ favor by providing financial or nonmonetary relief, such as changing information on a credit report. Otherwise, complaints are generally closed with an explanation. Complaints are shown in the month the CFPB received the complaint. Companies have up to 60 days to provide a final response. Data as of Feb. 23, 2026.

In statements to ProPublica, the credit bureaus said that many complaints are illegitimate, including a large volume filed by credit repair organizations that charge customers to challenge negative information on their reports. A CFPB spokesperson also said that the complaint system was inundated with submissions from bots and third-party credit repair firms, which the agency was working to address. CFPB did not respond to written questions about the decline in relief or enforcement.

Posted by propublica_

12 Comments

The Experian complaints data don’t fit the CFPB narrative. This could be the TikTok trend of falsely reporting any negative marks on your credit report to try and raise your score. It seemed to start ~2 years ago and now the bureaus have caught on.

It’s almost as if this was by design, or something.

They’re currently directing resources towards removing a plethora of bankruptcies from Trump’s credit report…

This is a very short time window of roughly four years. It would be useful to see this data going back 20 years.

As someone who runs credit reports on a daily basis for the past decade, average credit scores have increased considerably over that period without proportional improvements in underlaying negative factors such as late payments, collections, and charge-offs. Credit reports are far more favorable given the same set of circumstances as they were over the past 10 years I’ve been working with them regularly. Ironically the avereage underlying data I’ve looked at has gotten worse over that time period. So I’m skeptical that this chart is reflective of anything meaningful as from where I sit, people’s credit has gotten worse while their credit rating has improved.

>A CFPB spokesperson said the complaint system was inundated with submissions from bots and third-party credit repair firms, and the agency was working to address that so legitimate consumers can more effectively get help. The agency did not respond to written questions about the decline in relief or enforcement.

Seems like as credit score become a widely used tool they will be socially hacked to become less useful.

To me this is exactly like a good product that was found by lots of people leading to its enshitification. Bots now run most of the Internet traffic and bots run most of the credit score traffic so bots will soon run most of the credit score complaint traffic.

All I’m seeing is continuation of trends that began well before Trump’s inauguration

It’s wild how some people in the US don’t seem to get that regulations exist for the consumer’s benefit. They’re meant to force companies to operate responsibly. Without them, corporations would just focus on maximizing profits without giving a single thought to consumers.

Without knowing the actual validity of these claims, this data is meaningless.

Pffft, who needs Consumer Financial Protection anyway?

Why did the total number of complaints increase by 3x? Seems hard to blame that on the CFPB…

> In statements to ProPublica, the credit bureaus said that many complaints are illegitimate, including a large volume filed by credit repair organizations that charge customers to challenge negative information on their reports. A CFPB spokesperson also said that the complaint system was inundated with submissions from bots and third-party credit repair firms

Oh. Well… maybe they’re telling the truth? Note the absolute number of “complaints closed with relief” is still roughly double what it was in 2024, at least for TransUnion. Experian does seems like there’s definitely a problem, though the drop in “complaints closed with relief” seems to have started *before* Trump’s inauguration?

I thought doge pretty much killed the CFPD

Dude fuck these credit bureaus. You’re not the customer – companies who get sold your financial info are. And at this point I think 2/3 of them have lost my personal data to hackers.

Set up accounts with all 3 major credit bureaus online, then FREEZE YOUR CREDIT. This means people can’t open accounts in your name, and the credit bureaus can’t sell your data in the same way.

I forgot about it and applied for a new credit card. Immediately denied – working exactly as expected. You can just login and lift the freeze for a set number of hours.

Every single person should do this.