[OC] Social Security is projected to pay full benefits through 2034, then 81% under current law

Posted by Low_Ability4450

![[OC] Social Security is projected to pay full benefits through 2034, then 81% under current law](https://www.byteseu.com/wp-content/uploads/2026/06/pr4ukehrf25h1-1536x864.png "[OC] Social Security is projected to pay full benefits through 2034, then 81% under current law")

[OC] Social Security is projected to pay full benefits through 2034, then 81% under current law

Posted by Low_Ability4450

31 Comments

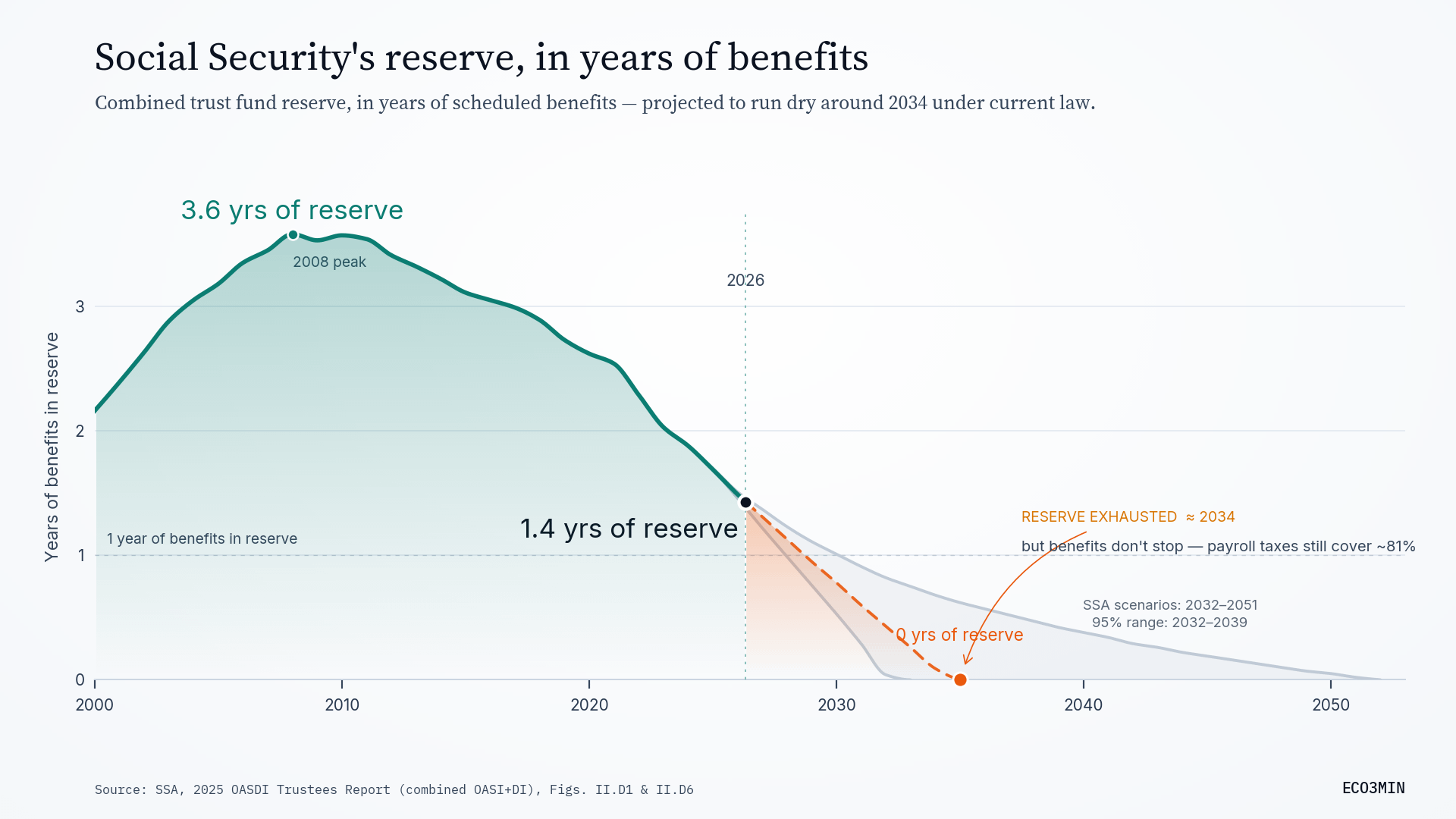

Three numbers do most of the work here, and the third is the one people usually miss.

Combined trust fund (retirement + disability), SSA 2025 Trustees Report, under current law:

• 2008: reserves peaked at 3.6 years of benefits (358% of one year’s cost)

• May 2026: 1.4 years left

• 2034: reserves reach zero — and benefits do NOT stop. Continuing payroll taxes still cover 81% of scheduled benefits, declining to 72% by 2099

So the event in 2034 isn’t “the checks stop.” It’s a 19% shortfall on a program that keeps paying 81% out of ongoing payroll tax unless current law changes first.

The fan after 2026 is the three official Trustees scenarios: depletion in 2032 (high-cost), 2034 (intermediate / best estimate), and 2051 (low-cost). The SSA’s stochastic model (5,000 simulations) puts 95% of outcomes between 2032 and 2039. The retirement fund on its own (OASI, excluding disability) reaches zero a year earlier, in 2033, at 77% payable.

I built an interactive version on eco3min where you can toggle between the reserve fan, the share of benefits payable over time (100% → 81% → 72%), and the two funds split (OASI 2033 vs DI vs combined) — useful if you want to see why the “combined” date is later than the retirement-only one.

https://eco3min.fr/en/social-security-trust-fund-depletion/

Tools: Python (matplotlib). Sources: SSA 2025 OASDI Trustees Report (Figs. II.D1, II.D6, II.D8), Congressional Research Service, SSA Monthly Statistical Snapshot. Full dataset (CSV/XLSX) on the page. Happy to answer methodology questions.

Honest open question for the sub: some read “81% payable” as proof the system is fundamentally fine and just needs a modest tax or benefit tweak; others read a 19% cut hitting in ~8 years as a serious near-term problem. The data is the same either way — curious how this sub reads it.

Guess what year I reach retirement age? Sorry, entire country, my epic personal bad luck is going to bring the whole system down!

Welp, we’re boned. Who’s up for a world ending orgy in 30 years?

This shows the reserve, extra money collected but not yet paid out. But there was $0 in the fund the day it started. What a data analysis should show is the consequences of reasonable course corrections: say, raising taxes by removing the cap on social security wage contributions. Or limiting payouts to those with significant assets.

*Me, born in 1968, doing some quick math in my head…*

It’s too bad maximizing shareholder value doesn’t include paying enough taxes to have a safety net for society.

Were gonna expand SS soon otherwise its gonna turn into the walking dead on the streets soon. 5% of america is probably aging seniors eating a can of dinty moore a day right now

I’ve always heard that the issue is demographic booms, with more people retiring than contributing. If that’s the case, and SSA payments reduce to make up for it, is there a point to predict it reverses and starts having more than it needs, once a younger generation is bigger than the retired one?

(I can imagine that length of retirement too, caused by longer lifespans, is an aggravating factor.)

Enough of these thieves in office. It’s time to TAKE OUR MONEY BACK. They have repeatedly robbed social security that WE have paid directly into. Vote for people who will do the same to the top 0.1%. Not tax them. TAKE it from them. The class wars have been going on for ever, and we have the numbers in our favor.

As someone closer to retirement age than I want to admit, these projections make me think about taking Social Security earlier than I would normally need to. If I think my checks are going to be down 20% in 15 years then I might as well take it at 62. I’m wondering if more people will do the same which will then deplete the reserves even faster.

Remove the Social Security tax cap.

Elon Musk pays the same amount into Social Security as your kid’s pediatrician.

That’s not sustainable.

We really should be able to opt out of all benefits and payment after we put our 10 years of contributions in.

Take my free money leave me alone while I boost my 401k savings by 13%, or 10% and I buy a term policy.

So the range of values is just the difficulty of predicting the future. It would be interesting to see what impact proposed changes to Social Security law would have on this graph. My understanding is that changes were made around 1980, which allowed the reserves to build up again.

Which country are we talking about?

IN WHICH COUNTRY?

Jesus, we all don’t live where you live

Funny, I’m expected to pay full social security till 2034, then also continue to pay full (if not more) social security after until 2060 when I turn 65, when I get nothing.

Yea the boomers orchestrated a wealth redistribution scheme where young people paying into the system now are funding their cushy retirements, and as soon as the boomer generation kicks the bucket the entire system runs out of funding and collapses in on itself. The “me” generation, the most selfish bunch of jerks to ever populate this planet. Beatniks and hippies bucking responsibility and “free love” fucking without consequence in the 60s when it suited them, turned Reaganites by the 80s once it was their time to get rich, then corporatists from the 90s onward to preserve the wealth they’d accrued and keep everyone below them from catching up. Now they’re going to coast into the sunset leaving the country drowning in debt with all the systems they’d benefited from too underfunded to be rescued.

They have been saying that my whole life. It’s why I’ve planned my retirement as if I will get nothing for social security and then it’s just a bonus if I do. I’m honestly more personally worried about Medicare, as I have no alternatives to that when I retire.

That’s what happens when the pyramid scheme depends on infinite population growth

It was always going to collapse. It was a matter of when, not if.

This is why in Canada they transitioned to a semi-private system with the CPP, the CPP in the funds after transition are now effectively self sustaining by having a growth rate faster than the drawdown rate

It’s kind of absurd the SSA is only allows to invest in bonds, even if they didn’t invest in stocks and private equity like the CPP, it could still invest in infrastructure that would bring long term returns like trains, bridges, and other infrastructure to double as an infrastructure fund

There’s a reason the CPP owns the Chicago skyway, or like half of Canada’s biggest toll highway

We could just give it 1.5 trillion like we give to the military. But that would require congress doing something to help the people who pay them.

Why am I forced to contribute to SS, when I may never get anything back?

Remove the salary cap limit to contributions, but cap salary-based distributions.

Yup, keep giving our money to various countries yet Fuk the one that pay for it. Gotcha!

If they can minimize the fraud that is rampant in the SS system, it should put it on the right path.

You forgot to mention the country. You should probably remove your post and upload it again with the proper context.

Remove the income cap on ss tax!

Quick question, did boomers have kids **specifically** to scam them? Or are they just slimy people incapable of foresight beyond 48 hours?

People think the Social Security reserve is a pile of cash, but it’s not. The surplus was, by law, invested in US treasuries and then spent by the government. So the surplus is basically a bunch of IOUs.

So it’s not like the pile of cash runs out in 2034 or some other date. The government as a whole is still spending more than it makes and borrowing to pay the bills. That will continue.

And also — Social Security is a payroll tax on wages, and wages as a % of national income is at historic lows and headed lower, with more and more money flowing to holders of capital. It’s not just the cap, it’s the wage theft at the bottom of the wage distribution by rich owners who do not need Social Security.

Maybe increase immigration?