I envy those who were able to refinance in the low 2%. That’s life changing.

mariogamer9 on

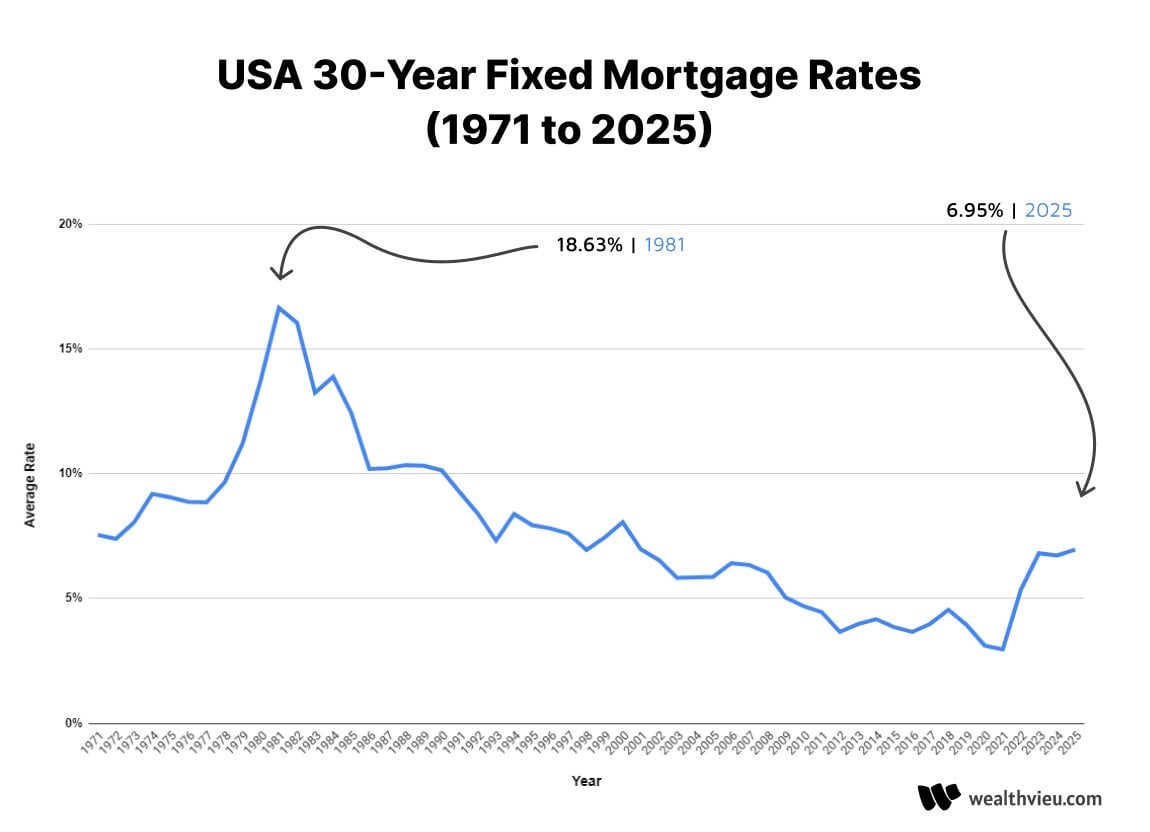

And I thought rates were high now. Looks like we’re just returning to the historical norm

Clemario on

Shout out to my fellow mortgage refinancers of 2020-21. We will never move.

Common_Senze on

One of the main problems the fact the housing market is way over bloated and simply not worth it. In TX, a $450k home, with 2.5% property tax (it ranges 1.5 to 4 ish%), plus insurance would cost 4500 to $5k per month.

BatmanOnMars on

Who makes these websites with a few random data series and nothing else but ads? You could find this on FRED and it would be way more useful.

Seriously, “wealthvieu”!?

iGrimFate on

Don’t forget the most important part. Homes in 1980 were $50,000 – 60,000.

17% on $60,000 vs 7% on a current $500,000 home

plausden on

born at the high, bought at the low.

slewfootedhoopajew on

Rates are actually normalized…house prices? No.

talljoe999 on

We refied like most in ‘21. We went from a 30yr to a 20 yr. And I think we went from 4.125 to 3. The new mortgage will save us nearly $100k in interest over the previous mortgage.

Saxonite13 on

My fiance and I bought our first home at 9.0% in 3023. We just refinanced at the beginning for 2025 at 5.1% and we couldn’t be any happier. Interest is such a scam

sickofwords on

Got at 2.95 in 2021. Seller said he wanted to self finance me for 10 years and renegotiate after 10 and I said no thanks. I knew rates would never be as low as they were then.

joegrizzly02 on

I bought my house at the end of 2020 at 3.12%. Best decision I ever made.

tart_reform on

I was going through estate stuff for my dad and realized his mortgage rate was 17% originally. He also had six kids and a stay at home wife. The cost of life has just been rearranged.

WYO1016 on

Got mine at 3.5% in 2016. Just missed the window to cut a point off of that, but I’m certainly not angry about what I have.

Utterlybored on

I bought my first house on the tip of the spike in 1981. House was cheap, though.

reality_aholes on

Only thing that could bring better clarity is the average new home price or average monthly income required.

HornStar1974 on

Keep in mind those who bought during this time way overpaid for the property. Probably still saving money, but not as much as you think. If you re-financed it was the deal of a lifetime.

bjb13 on

I bought my first home in 1980. As I recall my interest rate was 12.5%. Yuck

EchoCyanide on

Bought a house near the bottom, 3.5%. I won’t move until this house is paid off and I can use the equity to buy something smaller in cash. I got lucky.

iggnac1ous on

30 year at 3.2 started 2011

ScarletNerd on

Just a reminder to those that missed out on low rates and are stuck with the high rates: IF you can afford it, just make an inflated principal payment and the ridiculous interest on your 30 year will melt away much faster. Every 30 year mortgage I’ve had I’ve tried to pay it at the 15-20 year payment plan. That way I save $100K+ in interest and if things go south you can fall back to paying the minimum if needed.

For example: If your starting payment is $1000/m (leaving off taxes and insurance) just auto pay an extra $500 onto the principal every month and forget about it. If you start this early the loan will melt away much faster by a decade or more.

I completely understand this is not always possible, but if you’re just paying the minimum you’re hurting yourself long term over only $500. I’ve had this conversation with so many friends and family that can afford to pay above minimum and they’re shocked when thet see the amortization and how much money they’re wasting. You should never pay minimum if you don’t have to. The more you pay towards the principal the better.

Counter argument: stock market returns on that $500/m compounded is typically greater than your interest rate, so just invest it and pay the mortgage off that way when they reach parity. BIG BUT: this assumes a stable market of long term growth, that investment could also go south whereas your mortgage isn’t going anywhere. Also with rates at 7% it’s kind of a wash now.

ShadowFox2020 on

Overlay that with the median prices of homes during the same period

hazmatt24 on

The missing component is what the average cost of a home was. In 1981, it was $83k ($275k adjusted for inflation). You can’t find a decent house in a desirable area for under $400k now. Everyone talks about how high the interest rates are, but they are average. The cost of homes is grossly over inflated. If housing costs had stayed even with inflation, you’re looking at around $1500 a month, which wouldn’t be outlandish in today’s dollars. The issue is that current owners don’t want to lose value (I know I don’t), but the only way to fix the housing crisis is to increase inventory and drive the prices back down. Construction can’t keep up with demand, especially with the current administration getting rid of all the workforce and the potential for material logjams depending on how tariffs play out. What needs to happen is a limit on property ownership. Ban corporations from owning single family property and limit the number of homes that an individual can have. Free up all the rentals and AirBnBs for people wanting home ownership. That ain’t happening in at least the next four years, though, and highly unlikely after that due to the Blackstones of the world padding congressional pockets.

24 Comments

Now do wages:price over the same period

I envy those who were able to refinance in the low 2%. That’s life changing.

And I thought rates were high now. Looks like we’re just returning to the historical norm

Shout out to my fellow mortgage refinancers of 2020-21. We will never move.

One of the main problems the fact the housing market is way over bloated and simply not worth it. In TX, a $450k home, with 2.5% property tax (it ranges 1.5 to 4 ish%), plus insurance would cost 4500 to $5k per month.

Who makes these websites with a few random data series and nothing else but ads? You could find this on FRED and it would be way more useful.

Seriously, “wealthvieu”!?

Don’t forget the most important part. Homes in 1980 were $50,000 – 60,000.

17% on $60,000 vs 7% on a current $500,000 home

born at the high, bought at the low.

Rates are actually normalized…house prices? No.

We refied like most in ‘21. We went from a 30yr to a 20 yr. And I think we went from 4.125 to 3. The new mortgage will save us nearly $100k in interest over the previous mortgage.

My fiance and I bought our first home at 9.0% in 3023. We just refinanced at the beginning for 2025 at 5.1% and we couldn’t be any happier. Interest is such a scam

Got at 2.95 in 2021. Seller said he wanted to self finance me for 10 years and renegotiate after 10 and I said no thanks. I knew rates would never be as low as they were then.

I bought my house at the end of 2020 at 3.12%. Best decision I ever made.

I was going through estate stuff for my dad and realized his mortgage rate was 17% originally. He also had six kids and a stay at home wife. The cost of life has just been rearranged.

Got mine at 3.5% in 2016. Just missed the window to cut a point off of that, but I’m certainly not angry about what I have.

I bought my first house on the tip of the spike in 1981. House was cheap, though.

Only thing that could bring better clarity is the average new home price or average monthly income required.

Keep in mind those who bought during this time way overpaid for the property. Probably still saving money, but not as much as you think. If you re-financed it was the deal of a lifetime.

I bought my first home in 1980. As I recall my interest rate was 12.5%. Yuck

Bought a house near the bottom, 3.5%. I won’t move until this house is paid off and I can use the equity to buy something smaller in cash. I got lucky.

30 year at 3.2 started 2011

Just a reminder to those that missed out on low rates and are stuck with the high rates: IF you can afford it, just make an inflated principal payment and the ridiculous interest on your 30 year will melt away much faster. Every 30 year mortgage I’ve had I’ve tried to pay it at the 15-20 year payment plan. That way I save $100K+ in interest and if things go south you can fall back to paying the minimum if needed.

For example: If your starting payment is $1000/m (leaving off taxes and insurance) just auto pay an extra $500 onto the principal every month and forget about it. If you start this early the loan will melt away much faster by a decade or more.

I completely understand this is not always possible, but if you’re just paying the minimum you’re hurting yourself long term over only $500. I’ve had this conversation with so many friends and family that can afford to pay above minimum and they’re shocked when thet see the amortization and how much money they’re wasting. You should never pay minimum if you don’t have to. The more you pay towards the principal the better.

Counter argument: stock market returns on that $500/m compounded is typically greater than your interest rate, so just invest it and pay the mortgage off that way when they reach parity. BIG BUT: this assumes a stable market of long term growth, that investment could also go south whereas your mortgage isn’t going anywhere. Also with rates at 7% it’s kind of a wash now.

Overlay that with the median prices of homes during the same period

The missing component is what the average cost of a home was. In 1981, it was $83k ($275k adjusted for inflation). You can’t find a decent house in a desirable area for under $400k now. Everyone talks about how high the interest rates are, but they are average. The cost of homes is grossly over inflated. If housing costs had stayed even with inflation, you’re looking at around $1500 a month, which wouldn’t be outlandish in today’s dollars. The issue is that current owners don’t want to lose value (I know I don’t), but the only way to fix the housing crisis is to increase inventory and drive the prices back down. Construction can’t keep up with demand, especially with the current administration getting rid of all the workforce and the potential for material logjams depending on how tariffs play out. What needs to happen is a limit on property ownership. Ban corporations from owning single family property and limit the number of homes that an individual can have. Free up all the rentals and AirBnBs for people wanting home ownership. That ain’t happening in at least the next four years, though, and highly unlikely after that due to the Blackstones of the world padding congressional pockets.